You sell on Amazon, see sales tax collected at checkout, and assume the platform has it handled. Then a state auditor asks why you stopped filing returns, and the tax you thought was someone else’s problem turns into back taxes and penalties. That gap, between what the marketplace covers and what you still owe, is where multi-channel sellers lose real money.

Marketplace facilitator laws decide who collects sales tax on a sale and who is left holding the rest. They affect anyone on a third-party platform, anyone running a store alongside a marketplace, and anyone keeping books across both. This article covers how the laws work, where responsibility still falls on the seller, what changed in 2025 and 2026, and how to set up accounting so the same dollar of tax never gets remitted twice.

TL;DR

- Facilitator laws shift tax collection to platforms: Amazon, Etsy, and similar marketplaces collect and remit sales tax, but only on transactions that happen on their platforms.

- Sellers are still responsible for more than they think: Direct sales, registrations, filings, and nexus tracking remain the seller’s job even when marketplaces handle the tax.

- Rules vary by state and keep evolving: Thresholds are converging toward revenue-based limits, but definitions and edge cases still differ across states.

- Multi-channel selling creates accounting risk: If marketplace-collected tax isn’t recorded separately, liabilities get overstated, or the same tax gets paid twice.

- The safest approach is separation: Treat marketplace tax and seller-owed tax as different ledger events, track them separately, and review each channel regularly.

What is a marketplace facilitator?

A marketplace facilitator is a platform that lists products from third-party sellers, processes the payment, and sends the proceeds back to the seller. The Streamlined Sales Tax Governing Board defines it as a business that owns or operates a marketplace and facilitates third-party sales, collecting payment from the buyer and passing it to the seller.

| Amazon, Etsy, eBay, Walmart Marketplace, TikTok Shop, and Airbnb are the familiar examples. |

Why did states move collection onto these platforms? The math is simple. Chasing a million individual sellers, many with no nexus and some ignoring the rule anyway, costs states more than it collects. Collecting from one Amazon was far cheaper, and by 2026 every sales-tax state has a facilitator law.

Read our article about sales tax nexus.

How marketplace facilitator laws work, and what changed after Wayfair

The current rules trace back to the 2018 Supreme Court decision in South Dakota v. Wayfair, Inc., which let states require sales tax collection from sellers with no physical presence in the state. All 45 states with a statewide sales tax now enforce economic nexus laws, so sales volume alone can trigger an obligation. Each has two laws: economic nexus for direct sellers, and a facilitator law for the platforms.

Thresholds are converging on a single number

How much do you have to sell before a state cares? The most common standard is $100,000 in sales or 200 transactions, but several states are dropping the transaction count, and only 18 still impose one. The trend is toward a flat revenue benchmark, which removes the per-transaction trigger that punished low-priced-item sellers hardest. For the marketplaces themselves, thresholds are a formality: Amazon and eBay clear them everywhere on day one, so facilitator collection is universal across all 45 sales-tax states.

Which platforms are marketplace facilitators and which are not

There’s one misconception that costs sellers the most: assuming every selling platform is a marketplace facilitator. Some only provide the software to build a store, but they don’t facilitate the transaction between seller and buyer. They may calculate tax, but calculation and remittance differ, and only one keeps a seller off an audit list.

So which platforms collect for you, and which leave the duty to you? Start with the five marketplaces sellers use most.

Does Amazon collect sales tax for sellers?

Yes. Through its Marketplace Tax Collection program, Amazon calculates, collects, and remits sales tax on third-party seller transactions in all 45 states with a statewide sales tax, plus the District of Columbia. Collection happens automatically at checkout, and Seller Central reports show the tax broken out by order.

What Amazon doesn’t handle is the rest of your tax picture. If Amazon stores your inventory in a fulfillment center in another state, that can create physical nexus there, so you may owe tax on direct, non-Amazon sales into that state. Amazon also won’t file returns in your name where a state requires one. For the full split, see the quick-reference table and the state matrix below.

Does Etsy collect sales tax for sellers?

Yes. Etsy collects and remits sales tax on seller transactions in all 45 sales-tax states, plus the District of Columbia and Puerto Rico. The collected amounts appear in your Etsy shop dashboard, and Etsy handles remittance for the orders without any action on your part.

Reporting requirements still vary by state. Some want Etsy sellers to keep an active permit and report marketplace sales on their own returns, even though Etsy already remitted the tax; others don’t. Etsy collecting on your behalf does not automatically clear your registration or filing obligations. Check the state matrix below for where a separate seller return applies.

Does eBay collect sales tax for sellers?

Yes. eBay collects and remits sales tax on transactions in every state with a marketplace facilitator law. The collected tax is included in your eBay payout detail, so you can reconcile it against what reached your bank.

eBay doesn’t handle your direct-sales obligation. If you sell the same products through your own website, at events, or wholesale, those sales are yours to track, and they may count toward economic nexus where eBay’s marketplace sales pushed you over the threshold. Treat eBay’s collection as covering eBay orders only.

Does Walmart Marketplace collect sales tax for sellers?

Yes. Walmart Marketplace collects and remits sales tax on seller transactions in every state with a marketplace facilitator law, reported per order in Walmart Seller Center.

As with the other large marketplaces, Walmart’s collection covers only sales made through Walmart. You still owe sales tax on direct sales wherever you have nexus, and Walmart won’t file a return in your name. If a state requires a separate seller return alongside Walmart’s remittance, that filing is on you.

Does TikTok Shop collect sales tax for sellers?

Yes. TikTok Shop collects and remits sales tax where marketplace facilitator laws apply, which now covers every state with a statewide sales tax. It’s a newer program than Amazon or eBay, so watch how it reports as it matures. Collected tax shows up in the TikTok Shop Seller Center.

TikTok Shop follows the same pattern as the others: it covers TikTok Shop orders, not your direct sales, and not your registration or filing obligations, where states still require them. For the full picture, see the quick-reference table and the state matrix below.

What doesn’t count as a marketplace facilitator?

Plenty of services touch an online sale without meeting the facilitator definition. Payment processors are the clearest example: Stripe, Square, and PayPal, in their processor role, move money between buyer and seller, but they don’t own the listing relationship, so they aren’t facilitators and don’t collect sales tax for you. Advertising platforms like Google Ads and Facebook Ads direct buyers toward your store, but don’t host the transaction.

The same goes for pure store software: your own Shopify storefront, WooCommerce, Wix, BigCommerce, and Squarespace give you tools to build a shop, but the shop is yours, and so is the tax duty. Delivery network companies are the edge case; they usually aren’t facilitators, though some states now let them elect that status, as Ohio’s HB 315 does. If your platform doesn’t meet the facilitator definition, the collection duty stays with you, no matter how the buyer found you.

Here’s an overview:

| Platform | Marketplace facilitator? | What it means for you |

| Amazon | Yes | Collects and remits in every state with an MPF law |

| eBay, Etsy, Walmart Marketplace, TikTok Shop | Yes | Same coverage as Amazon |

| Shopify’s Shop channel | Yes, since Jan 1, 2025 | Shopify collects and remits on Shop channel orders only |

| Your own Shopify storefront | No | You are the merchant of record; you collect, remit, and file |

| WooCommerce, BigCommerce, Wix, Squarespace | No | Store software, not a marketplace; the duty stays with you |

| Meta (Facebook & Instagram) | No, since Aug 26, 2025 | Meta stopped acting as an MPF; the duty came back to you |

The line shifts more often than sellers expect, and 2025 moved it both ways. On January 1, 2025, Shopify’s Shop channel began collecting and remitting sales tax in every state with a statewide sales tax, plus DC and local taxes in Alaska, but only on Shop channel orders. The storefront still works the old way, with the seller as merchant of record.

Going the other way, Meta stopped acting as a facilitator for all new orders created on or after August 26, 2025, so Facebook and Instagram Shops sellers got that responsibility back partway through the year.

| The takeaway for anyone running more than one channel: classify each channel separately, and revisit the list every quarter. A platform that handled your tax in January may not handle it in December. |

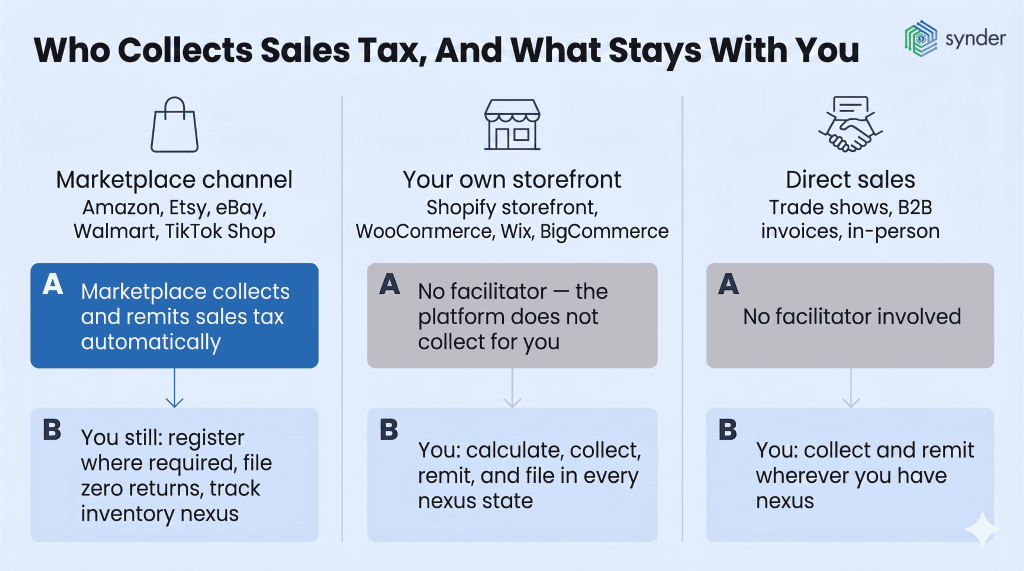

What sellers still have to do, even when the marketplace collects

Marketplace facilitator laws relieve one duty, collecting and remitting tax on platform sales, and leave the rest in place. Treat the law as a blanket exemption, and you’re the seller who gets the audit letter. So what’s still on the seller’s plate?

- Sales outside the marketplace. Amazon collects on Amazon. Your own Shopify store, trade show table, direct B2B invoices, and in-person sales are your responsibility wherever you have nexus.

- Sales tax registration in many states. Plenty of states still require a valid permit and your own returns, even when a platform handles collection. New Jersey requires remote sellers over the threshold to register, even if they sell only through a marketplace. Alabama is different: in-state marketplace-only sellers apply for an exemption certificate, not a sales tax account. Confirm your status in each state before deregistering anything.

- Filing zero or informational returns. Some states want you to file in your own name even when the marketplace remitted everything. Texas has in-state sellers keep their permit and file on time, with marketplace revenue in Total Sales but not Taxable Sales. Washington won’t let marketplace-only sellers cancel their permit at all, since it ties Business & Occupation tax to the same return.

Separate returns and written-agreement waivers

A few states go further than a zero return, requiring a marketplace seller to file a separate return alongside the marketplace’s own remittance so the state can match the two. Georgia, Indiana, and North Dakota are verified examples.

A smaller group of states let the seller and the marketplace shift collection responsibility by written agreement. Nevada, New Jersey, and Tennessee have provisions along these lines, though it’s rarely used in practice, because large marketplaces don’t sign individual collection agreements with small sellers. Either way, the marketplace collecting tax does not always mean it has discharged every filing obligation tied to those sales. Check the state’s Department of Revenue guidance before assuming otherwise.

- Counting marketplace sales toward economic nexus. Most states roll marketplace sales into your nexus calculation, which can push you over the threshold for direct-sales obligations even when a marketplace drove all the volume. In New York, marketplace sales count toward the threshold even though the marketplace already collected the tax.

- FBA inventory triggering physical nexus. If Amazon stores your inventory in a warehouse in another state, you may have physical nexus there for non-marketplace sales. Amazon handles tax on your Amazon orders, but the direct-sales obligation is yours.

Quick reference: what’s collected, what’s yours

| Channel | Who collects sales tax (US) | Your remaining obligations |

| Amazon (third-party seller) | Amazon, in every sales tax state | Register where required; file zero returns; track FBA-inventory nexus |

| Etsy | Etsy, in all 45 sales tax states + DC + Puerto Rico | Register where required; report sales on direct returns in some states |

| eBay | eBay, in every sales tax state | Same as Etsy; registration and reporting can still apply |

| Walmart Marketplace | Walmart, in every sales tax state | Same as Etsy and eBay |

| TikTok Shop | TikTok, where MPF laws apply | Same standard MPF rules |

| Shopify’s Shop channel (since Jan 1, 2025) | Shopify, on all U.S. orders through the Shop channel | Track separately from your storefront; different tax treatment |

| Your Shopify storefront | You are the merchant of record | Calculate, collect, remit, file in every nexus state |

| WooCommerce, Wix, BigCommerce | You are the merchant of record | Same as Shopify storefront |

| Facebook & Instagram Shops (post-Aug 26, 2025) | You are the merchant of record | Meta no longer files for you on new orders |

| Airbnb / Vrbo (Colorado, since Jan 1, 2025) | Platform, under SB24-024 lodging rules | Local lodging-tax compliance still applies |

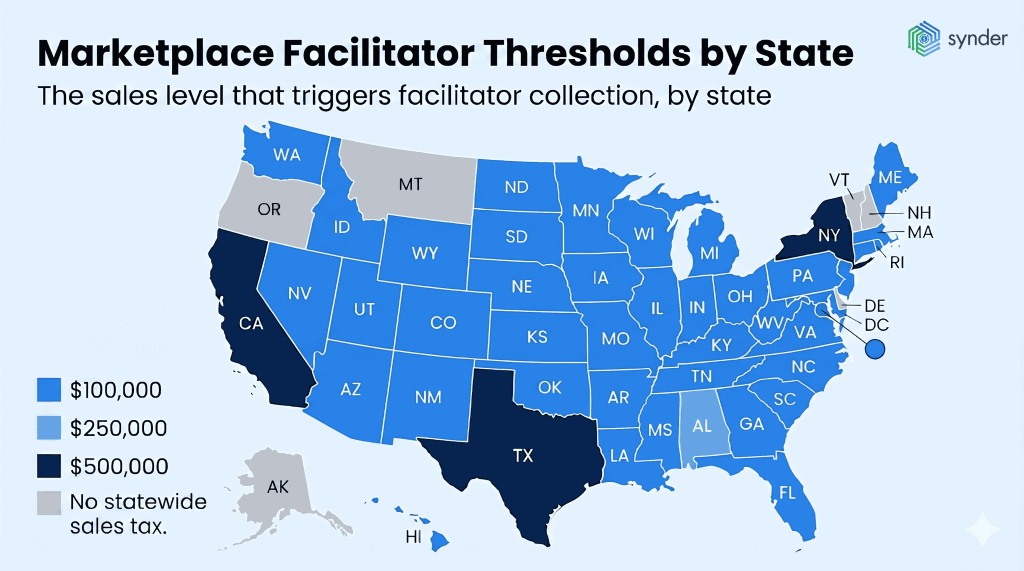

Marketplace facilitator thresholds by state

Every sales-tax state has a marketplace facilitator law, but the trigger threshold and whether you still file your own return vary. The 25 states with the highest ecommerce sales volume are below; the same general rules apply in the remaining 20 sales-tax states, with state-specific variations.

| State | Threshold | Effective date | Separate seller return required? | Notes |

| Alabama | $250,000 | Oct 1, 2018 | Sometimes | In-state marketplace-only sellers apply for an exemption certificate |

| Arizona | $100,000 | Oct 1, 2019 | Sometimes | Marketplace sales excluded from the seller’s threshold |

| California | $500,000 | Oct 1, 2019 | Sometimes | Marketplace sales count toward the seller’s threshold |

| Colorado | $100,000 | Oct 1, 2019 | Sometimes | SB24-024 extended facilitator rules to lodging platforms |

| Florida | $100,000 | Jul 1, 2021 | Sometimes | Revenue-only threshold |

| Georgia | $100,000 or 200 transactions | Apr 1, 2020 | Yes | Separate seller return can apply |

| Illinois | $100,000 | Jan 1, 2020 | Sometimes | 200-transaction threshold removed Jan 1, 2026 |

| Indiana | $100,000 | Jul 1, 2019 | Yes | Separate seller return can apply |

| Louisiana | $100,000 | Jul 1, 2020 | Sometimes | 200-transaction threshold removed Aug 2023 |

| Maryland | $100,000 or 200 transactions | Oct 1, 2019 | Sometimes | Revenue or transaction trigger |

| Massachusetts | $100,000 | Oct 1, 2019 | Sometimes | Revenue-only threshold |

| Michigan | $100,000 or 200 transactions | Jan 1, 2020 | Sometimes | Revenue or transaction trigger |

| Minnesota | $100,000 or 200 transactions | Oct 1, 2019 | Sometimes | Revenue or transaction trigger |

| Missouri | $100,000 | Jan 1, 2023 | Sometimes | Last state to adopt economic nexus |

| New Jersey | $100,000 or 200 transactions | Nov 1, 2018 | Sometimes | Collection can shift by written agreement; non-reporting status available |

| New York | $500,000 + 100 transactions | Jun 1, 2019 | Sometimes | Marketplace sales count toward the seller’s threshold |

| North Carolina | $100,000 | Feb 1, 2020 | Sometimes | 200-transaction threshold removed Jul 1, 2024 |

| Ohio | $100,000 or 200 transactions | Sep 1, 2019 | Sometimes | HB 315 lets delivery network companies elect facilitator status |

| Pennsylvania | $100,000 | Jul 1, 2019 | Sometimes | Revenue-only threshold |

| South Carolina | $100,000 | Nov 1, 2018 | Sometimes | Revenue-only threshold |

| Tennessee | $100,000 | Oct 1, 2020 | Sometimes | Collection can shift by written agreement |

| Texas | $500,000 | Oct 1, 2019 | Yes | In-state sellers keep their permit; marketplace revenue in Total Sales, not Taxable Sales |

| Virginia | $100,000 or 200 transactions | Jul 1, 2019 | Sometimes | Revenue or transaction trigger |

| Washington | $100,000 | Oct 1, 2018 | Yes | Marketplace-only sellers can’t cancel the permit; B&O tax ties to it |

| Wisconsin | $100,000 | Jan 1, 2020 | Sometimes | 200-transaction threshold removed in 2021 |

“Sometimes” in the separate-return column means the answer depends on whether you have physical presence, direct sales, or another in-state obligation. When marketplace sales are your only activity, many of these states let you file a zero return or skip filing entirely. Always confirm with the state’s Department of Revenue.

State-specific quirks worth knowing in 2026

The 2025–2026 update wave touched economic nexus thresholds, lodging rules, delivery taxation, and audit programs across more than a dozen states. The changes most likely to affect a marketplace seller, by effective date:

- Alaska, January 1, 2025. Repealed the 200-transaction threshold; economic nexus now rests solely on $100,000 in gross sales.

- Colorado, January 1, 2025. SB24-024 extends facilitator-style lodging-tax reporting to short-term rental platforms like Airbnb and Vrbo, a sign “marketplace” is expanding into lodging, delivery, and rideshare.

- California SB 1144, into 2025. Added information-collection duties for high-volume third-party sellers; marketplaces now verify tax documents, location, and banking info.

- Ohio, April 3, 2025. HB 315 makes all delivery-network charges taxable, even on otherwise non-taxable items like groceries, and lets those companies elect facilitator status.

- Utah, July 1, 2025. Eliminated the 200-transaction threshold; $100,000 in sales is the only trigger.

- Illinois, January 1, 2026. Removed the 200-transaction threshold for remote retailers and facilitators; only $100,000 in gross receipts triggers nexus, per the Illinois Department of Revenue.

- Washington, February 1 to May 31, 2026. A pilot Voluntary Disclosure Agreement program for international remote sellers and facilitators, with up to 39% in penalty waivers.

Beyond these, several states broadened what’s taxable in 2026: Maine added streaming and digital audio, Rhode Island raised lodging taxes, and Texas ended its R&D equipment exemption. If you sell into any of these states, check whether the change affects a channel you treated as settled.

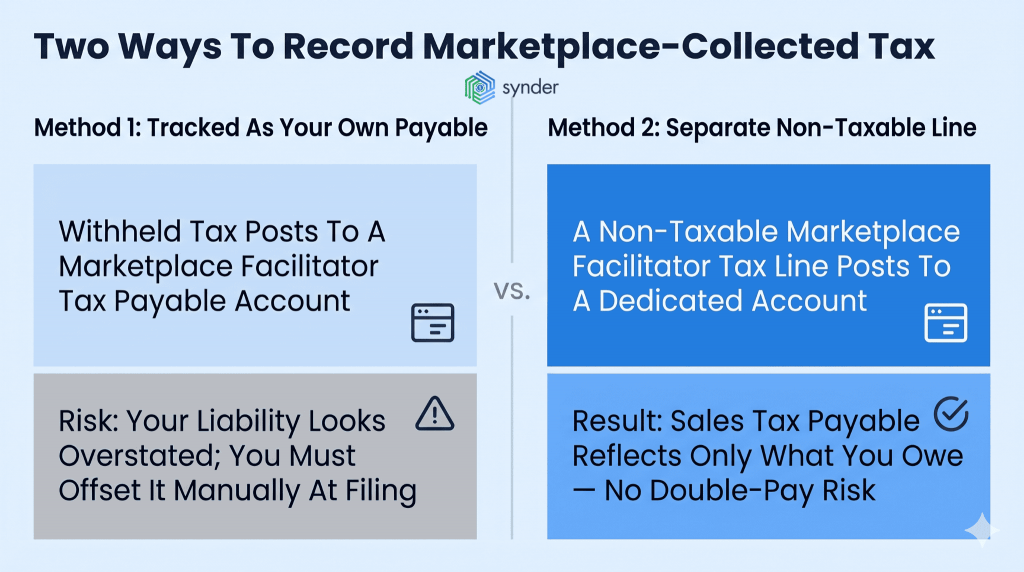

How should marketplace-collected tax appear in your books?

This is where the cleanest legal framework still costs sellers money. The marketplace remitted the tax, but it still has to be recorded correctly, or you’ll overstate your liability or pay the same tax twice at filing. So how should it appear in your books? There are two clean methods, and the second is the one most accountants recommend.

| Method | How it works | Consideration |

| Track it as your own payable | Withheld tax posts to a Marketplace Facilitator Tax Payable account and shows up in taxable sales reports | Your balance-sheet liability still reflects tax the marketplace already paid; you offset it manually at filing |

| Record it as a separate non-taxable line | A non-taxable Marketplace Facilitator Tax line posts to a dedicated account that never touches Sales Tax Payable | Cleaner; tracks marketplace tax fully without inflating your liability or creating a double-pay risk |

The second method keeps reports comparable: the Sales Tax Payable balance reflects only what the seller owes. Across hundreds of multi-channel sellers, one pattern dominates: tax that a platform already remitted appears in the wrong account, then gets paid again at filing. The fix is to segregate marketplace-collected tax by platform from the start. Set up the dedicated MPF accounts now, not at audit time, while you have a handful of transactions to backfill rather than a year’s worth.

A real warning from a practicing CPA

Megan Durst, CPA/ABV, CVA, principal at Dark Horse CPAs, warned Shopify sellers on LinkedIn after the Shop channel change took effect:

Shopify Sellers: Don’t Pay Sales Tax Twice! As of January 1, 2025, Shopify automatically collects and remits sales tax on orders placed through the Shop App in the U.S. While this simplifies compliance, it also creates a risk – double paying sales tax on your returns! When filing, be sure to: Separate Shopify’s remitted sales tax from what you owe. Report it correctly (some states require marking it as exempt). Review your reports carefully to avoid overpaying.

Megan Durst, CPA/ABV, CVA

Three implications follow for any multi-channel seller:

- First, “the platform paid it” isn’t the same as “the books reflect it”; the accounting still has to record the transaction so it can be backed out at filing time.

- Second, the exempt-flagging requirement is state-specific, so the same Shop channel order may be coded one way for New York and another for California.

- Third, the risk grows with every channel added, since each platform collects under different rules.

Where automation pays for itself

Synder is an accounting automation tool that helps businesses sync their ecommerce and financial data across 30+ platforms. It records marketplace facilitator tax as a separate line item by default for Shopify integrations, and on Amazon, eBay, Etsy, TikTok Shop, and Walmart – you pick between the two methods above per platform. Synder fetches each transaction, applies the tax treatment you set, and posts it to the right account in QuickBooks or Xero, so the separation happens at sync time, not audit time.

Consider a real example. TJAYZ, a retailer of handcrafted goods from Mexico, sells across Shopify, Amazon, eBay, Walmart, and Etsy with QuickBooks Desktop on the back end, so its team had every category of marketplace facilitator situation in one set of books. After connecting all five channels through Synder, every transaction flowed into QuickBooks with the tax tracked correctly per platform.

I don’t have to come back and babysit Synder; there’s nothing I need to worry about. Reflecting on it now, with our business expanding, I estimate that the time saved amounts to over 40 hours per month.

Tony Jamal, CEO of TJAYZ

That 40 hours a month wasn’t only about taxes. It was about making sure every transaction was categorized the way the IRS, the state, and an auditor would all recognize.

| To see how this maps to your channel mix, book a Synder demo. |

Audit-readiness: what to keep and what to expect

When an auditor shows up, “Amazon collects for me” is the start of an answer, not the whole answer. Most state revenue departments want documentation that the marketplace actually remitted the tax, especially where the seller is registered and filing returns.

As the Sales Tax Institute has flagged, a growing audit challenge is double taxation, when the facilitator and the retailer both tax the same transaction. So what should a seller produce on demand?

- Tax collection certificate from each marketplace. Amazon, eBay, Etsy, Walmart, TikTok Shop, and Shopify’s Shop channel each confirm they collected and remitted on your behalf. Save it per platform, per year.

- Payout reports showing tax withheld. Pull these from each seller dashboard at month-end. They bridge platform-collected tax and the deposit that reaches your bank.

- Sales tax in a separate ledger account. Marketplace facilitator tax should never share an account with your own sales tax payable. A dedicated account per platform beats one shared account.

- Reconciled returns showing the split. Every return should trace to a channel: one column direct, one column marketplace-collected and excluded from taxable sales, with totals tying back to your books.

- Nexus documentation by state. Record where you crossed economic nexus, when, and which sales pushed you over. Several states count marketplace sales toward the threshold even when the platform handled the tax.

- FBA inventory location reports. The FBA inventory location report shows which states hold your stock, which is where you may have physical nexus for non-Amazon sales.

If your accounting system can’t separate marketplace transactions from direct sales by tax treatment automatically, that work falls on you by hand at audit time.

Learn about top accounting software for multi-channel businesses.

Conclusions on marketplace facilitator laws and what they mean for your books

Marketplace facilitator laws have done what they were designed to do: shift the headache of state-by-state collection onto the platforms with the scale to handle it. The law is a relief on Amazon, Etsy, eBay, Walmart, and most major channels, and a trap on every channel where you assume the same rules apply.

Read it as a permanent split in your books. Keep marketplace-collected and seller-owed tax in separate accounts with separate reporting and documentation, and the system works as it should. Blur them together, and you’ll overstate your liability or pay the tax twice. States that wrote these laws are getting more active with audits, not less, and multi-channel sellers feel it first when their books don’t match the rules.

FAQ

How do I record marketplace facilitator tax so I don’t pay it twice?

Post it to a dedicated account that never touches your Sales Tax Payable balance, separated by platform. That keeps the tax fully tracked, keeps your liability accurate, and gives you a clean number to exclude at filing time.

What happens if a marketplace under-collects sales tax on my orders?

In most states, the marketplace, as the legal collector, carries the liability for tax on facilitated sales, including under-collection. Still, keep your own records: if the state questions a transaction, you’ll want payout reports and the marketplace’s documentation to show what was charged.

How do I reconcile a marketplace 1099-K with sales tax the platform already remitted?

A 1099-K usually reports gross transaction volume, which can include sales tax the marketplace collected and remitted. Pull the platform’s tax report alongside the 1099-K, separate the remitted tax from your taxable revenue, and document the difference so your income isn’t overstated.

What happens to marketplace-collected sales tax when a customer returns an order?

When the marketplace processes a refund, it generally reverses the sales tax it collected and adjusts its own remittance. Your books should mirror that reversal in the same dedicated marketplace-tax account, so a refund doesn’t leave stranded tax on your ledger.