Most ecommerce sellers find out about sales tax nexus the wrong way: a letter from a state revenue department about an inventory location they didn’t know they had, or a pre-audit questionnaire asking them to account for three years of unregistered sales. By that point, the question is no longer whether money is owed. It becomes how much is owed and to how many states.

The reason it plays out that way is that nexus rules have changed faster than most sellers track them, and the gap between knowing the rules and actually crossing a threshold is where the back taxes pile up. Below is what counts as nexus, what triggers it, how marketplace platforms fit in, and what to do once you’ve crossed a threshold.

TL;DR

- Nexus = tax obligation trigger: A business creates sales tax nexus through physical presence or economic activity (usually $100K in sales), and most states now enforce it.

- Rules are shifting toward sales-only thresholds: The 200-transaction rule is being phased out, making revenue the main trigger across states.

- It is more than just physical vs economic: Marketplace, click-through, affiliate, and trailing nexus can still create obligations even when sellers think they are covered.

- Compliance gets complex fast: Once nexus is triggered, sellers must register, configure tax collection, file regularly, and reconcile across channels.

- Ignoring nexus is expensive: States actively identify sellers, and missed registration can lead to years of back taxes, penalties, and interest, often avoidable through voluntary disclosure.

- Clean data and automation matter: Multichannel sellers stay compliant by keeping structured transaction data, monitoring thresholds, and using tools to handle syncing, reconciliation, and reporting.

What is sales tax nexus?

The cleanest definition comes from the Sales Tax Institute given on LinkedIn, which has been tracking how states define and enforce nexus since well before Wayfair:

Nexus is the connection between a business and a state that creates a sales tax obligation. Before 2018, that connection was almost always physical. A store. A warehouse. An employee. Then Wayfair happened. The Supreme Court ruled that economic activity alone – selling enough into a state, even with zero physical presence – can create nexus. Most states now have economic nexus thresholds, usually $100,000 in sales or 200 transactions. The biggest misconception we hear? ‘We don’t have a location there, so we don’t have nexus.’ That has not been true for years. And states are catching up fast.

Sales Tax Institute

The phrase nexus state just means a state where you’ve established that connection. You don’t pick which states; the facts of how and where you sell pick them for you. And because every state with a sales tax now enforces some form of economic nexus, sellers who built their business assuming “I’m only registered in my home state” are usually behind the actual rules.

Read more about ecommerce sales tax.

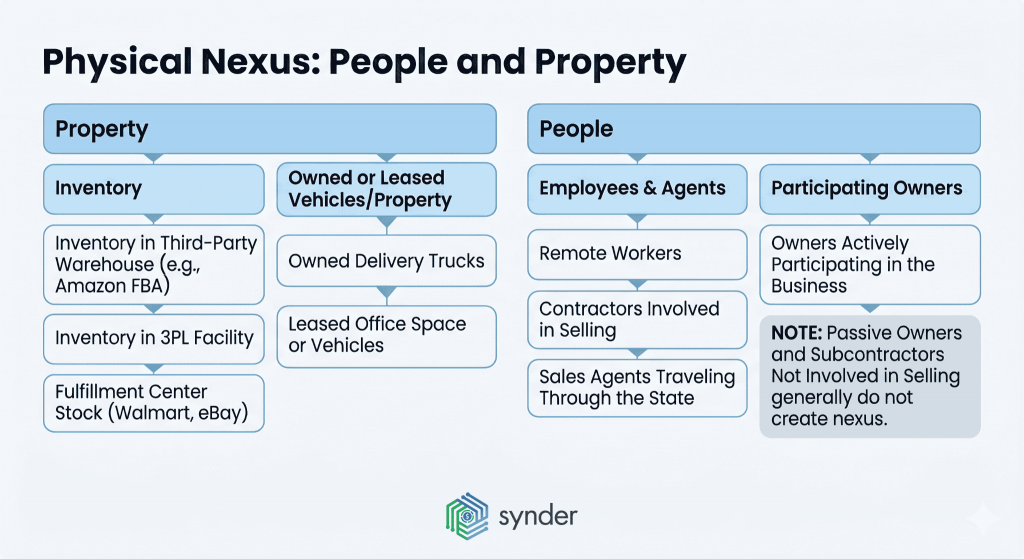

Physical nexus: people and property

Physical nexus is the older and simpler form. If your business has people or property in a state, you have nexus there from day one – no sales threshold to cross, no waiting period.

The two categories cover most situations. Property includes any inventory you store in a state, even if you don’t own the warehouse: products held in an Amazon FBA facility, goods at a third-party logistics provider, or stock at a fulfillment center for Walmart, eBay, or another platform. Owned or leased vehicles count too, as do leased properties. People means employees, contractors involved in selling, sales agents traveling through the state, and remote workers – even if your headquarters is somewhere else entirely. Owners who participate in the business count; passive owners and subcontractors not involved in selling generally don’t.

What this looks like: a Brooklyn-based meal-prep company with one office in New York that ships to customers in California has physical nexus in New York the day it opens. The day Amazon FBA stores its inventory at a California fulfillment center, it has physical nexus in California too. That’s why multichannel sellers using FBA have to be careful, as a single inventory transfer can create a registration obligation in a state you’ve never sold a single direct-to-consumer order from.

| A useful mental shortcut: physical nexus follows people and property, not where the customer is. If neither you nor your stuff is in the state, physical nexus is off the table, but economic nexus is getting started. |

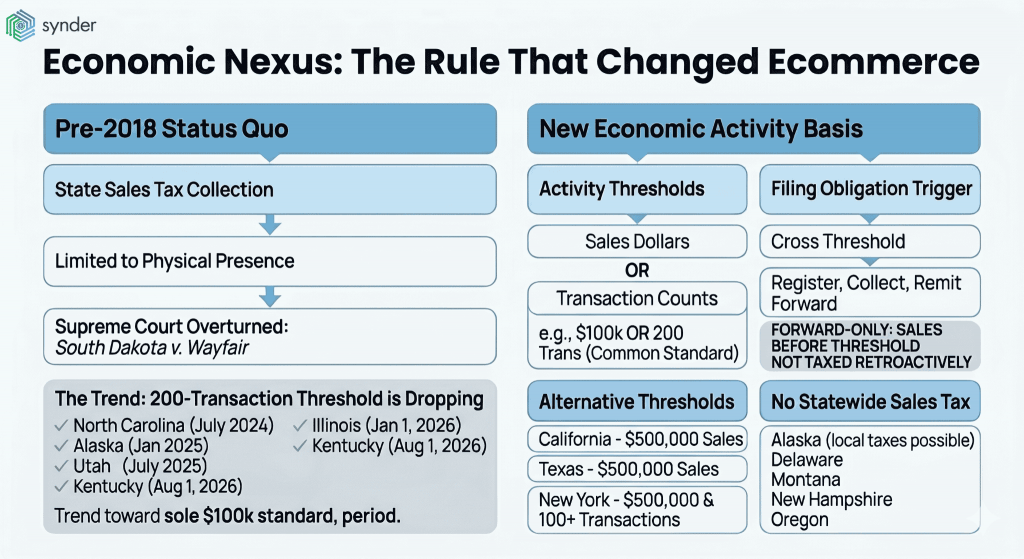

Economic nexus: the rule that changed ecommerce

Before June 2018, a state could only require you to collect sales tax if you had physical presence there. The Supreme Court’s South Dakota v. Wayfair decision overturned that. States can now impose collection on remote sellers based purely on economic activity in the state: sales dollars, transaction counts, or both.

Within months, every state with a sales tax adopted some version of an economic nexus rule. The most common standard, modeled on South Dakota’s law, has been $100,000 in gross sales OR 200 separate transactions in the current or previous calendar year. If you cross either threshold, you’re required to register, collect, and remit going forward (though you don’t owe back tax on the sales that got you there).

The 200-transaction threshold is on its way out

That standard is changing fast. According to the Sales Tax Institute’s Economic Nexus State Chart, every state with a sales tax now enforces economic nexus, but the 200-transaction trigger is being removed across the country.

| North Carolina dropped it in July 2024, Alaska followed in January 2025, Utah did the same in July 2025, Illinois removed its transaction count on January 1, 2026, and Kentucky is scheduled to follow on August 1, 2026. The trend points toward $100,000 in sales as the dominant (and in many cases sole) economic nexus standard. |

For high-volume, low-ticket sellers (for instance, a pet-treat brand selling $8 items), this is good news in states that have dropped the transaction threshold: 1,000 small sales adding up to $40,000 no longer trigger a filing obligation. For everyone else, the change is mostly clarifying. The bar is now sales dollars, period.

States that don’t follow the $100,000 rule

A few states fall outside the standard $100,000 framework:

- California – $500,000 sales threshold (sales only)

- Texas – $500,000 sales threshold (sales only)

- New York – $500,000 in sales and more than 100 transactions

States with no statewide sales tax:

- Alaska – no statewide tax (local jurisdictions may impose their own)

- Delaware

- Montana

- New Hampshire

- Oregon

Economic nexus thresholds by state (2026)

The table below covers all 45 states with a sales tax, plus Washington, D.C. The five states with no statewide sales tax (Alaska, Delaware, Montana, New Hampshire, and Oregon) are excluded.

Note: Local jurisdictions in Alaska can still impose their own taxes, so high-volume sellers shipping to Alaskan cities should check local rules separately.

| State | Sales threshold | Transaction threshold | Logic / notes |

| Alabama | $250,000 | None | Sales-only |

| Arizona | $100,000 | None | Sales-only since 2021 (TPT) |

| Arkansas | $100,000 | 200 | OR – either threshold triggers |

| California | $500,000 | None | Sales-only |

| Colorado | $100,000 | None | Sales-only (transaction threshold removed 2019) |

| Connecticut | $100,000 | AND 200 | AND – both must be met |

| Florida | $100,000 | None | Sales-only (prior calendar year only) |

| Georgia | $100,000 | 200 | OR – either threshold triggers |

| Hawaii | $100,000 | 200 | OR (general excise tax) |

| Idaho | $100,000 | None | Sales-only |

| Illinois | $100,000 | None | Transaction threshold removed Jan 1, 2026 |

| Indiana | $100,000 | None | Sales-only (200-transaction repealed 2024) |

| Iowa | $100,000 | None | Sales-only |

| Kansas | $100,000 | None | Sales-only |

| Kentucky | $100,000 | 200 (until Aug 1, 2026) | OR until Aug 1, 2026, then $100K-only |

| Louisiana | $100,000 | None | Sales-only (transaction threshold removed 2023) |

| Maine | $100,000 | None | Sales-only |

| Maryland | $100,000 | 200 | OR – either threshold triggers |

| Massachusetts | $100,000 | None | Sales-only |

| Michigan | $100,000 | 200 | OR – either threshold triggers |

| Minnesota | $100,000 | 200 | OR – either threshold triggers |

| Mississippi | $250,000 | None | Sales-only |

| Missouri | $100,000 | None | Sales-only |

| Nebraska | $100,000 | 200 | OR – either threshold triggers |

| Nevada | $100,000 | 200 | OR – either threshold triggers |

| New Jersey | $100,000 | 200 | OR – either threshold triggers |

| New Mexico | $100,000 | None | Sales-only (gross receipts tax) |

| New York | $500,000 | More than 100 | AND – both must be met |

| North Carolina | $100,000 | None | Transaction threshold removed July 2024 |

| North Dakota | $100,000 | None | Sales-only |

| Ohio | $100,000 | 200 | OR – either threshold triggers |

| Oklahoma | $100,000 | None | Sales-only |

| Pennsylvania | $100,000 | None | Sales-only (rolling 12 months) |

| Rhode Island | $100,000 | 200 | OR – either threshold triggers |

| South Carolina | $100,000 | None | Sales-only |

| South Dakota | $100,000 | None | Sales-only (transaction threshold removed 2023) |

| Tennessee | $100,000 | None | Sales-only |

| Texas | $500,000 | None | Sales-only |

| Utah | $100,000 | None | Transaction threshold removed July 2025 |

| Vermont | $100,000 | 200 | OR – either threshold triggers |

| Virginia | $100,000 | 200 | OR – either threshold triggers |

| Washington | $100,000 | None | Sales-only |

| West Virginia | $100,000 | 200 | OR – either threshold triggers |

| Wisconsin | $100,000 | None | Sales-only (transaction threshold removed 2021) |

| Wyoming | $100,000 | None | Sales-only (transaction threshold removed 2024) |

| Washington, D.C. | $100,000 | 200 | OR – either threshold triggers |

| Use this as a reference, not a registration roadmap. Thresholds, measurement periods, and what counts toward gross sales (taxable only? exempt sales too? marketplace sales?) vary, and several states have changed rules in the last 12 months. Always confirm with the state department of revenue or a licensed sales tax advisor before deregistering or skipping a registration. |

Other ways nexus can catch you off guard

Beyond physical and economic nexus, there are a handful of less-discussed nexus types as well:

- Marketplace nexus: If you sell through Amazon, Walmart, eBay, Etsy, or TikTok Shop, these platforms are usually classified as marketplace facilitators and required to collect and remit sales tax on your behalf. That doesn’t always mean you’re fully relieved of responsibility because many states still count marketplace sales toward your own economic nexus threshold, which can require you to register even if the marketplace is collecting the actual tax.

- Click-through nexus: Some states say you have nexus if in-state affiliates send you customers through referral links. Roughly 15 states have click-through nexus laws on the books, including New York, California, Pennsylvania, Connecticut, Maine, Rhode Island, Vermont, Louisiana, Arkansas, and Kansas – with thresholds typically set at $10,000 in referral-driven sales over 12 months.

- Affiliate nexus: Distinct from click-through, this applies when a related entity (a parent, sister company, or affiliated brand) operates in the state and meaningfully supports your sales, for example, by handling returns or providing customer service.

- Trailing nexus: Even after you stop the activity that created nexus, some states require you to keep collecting for a defined period. California is one example: if you cross its $500,000 threshold during a calendar year, you remain responsible for the rest of that year and the next, even if your sales drop below the threshold.

| Trailing nexus is the one most sellers miss when they try to “deregister” too early. Check the rule in each state before stopping collection. |

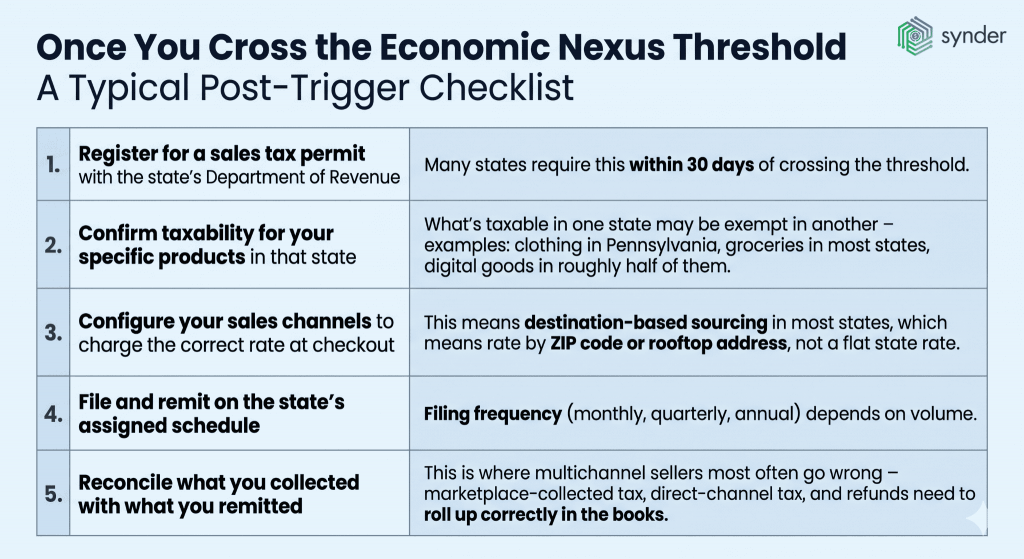

Once you cross the threshold

Triggering nexus is only the beginning, and what follows is where the real operational complexity lies.

The U.S. isn’t a single tax system but a network of 12,414 jurisdictions, with 681 rate changes and 335 new taxing authorities added in 2025 alone, including 108 new cities and 219 district taxes – the highest level since 2017, according to Vertex Inc.

This is the environment sellers step into once nexus is triggered. A typical post-trigger checklist looks like this:

- Register for a sales tax permit with the state’s Department of Revenue. Many states require this within 30 days of crossing the threshold.

- Confirm taxability for your specific products in that state. What’s taxable in one state may be exempt in another – clothing in Pennsylvania, groceries in most states, digital goods in roughly half of them.

- Configure your sales channels to charge the correct rate at checkout. This means destination-based sourcing in most states, which means rate by ZIP code or rooftop address, not a flat state rate.

- File and remit on the state’s assigned schedule. Filing frequency (monthly, quarterly, annual) depends on volume.

- Reconcile what you collected with what you remitted. This is where multichannel sellers most often go wrong – marketplace-collected tax, direct-channel tax, and refunds need to roll up correctly in the books.

How much getting sales tax wrong can cost

How much it costs to be wrong depends on the state. According to the Tax Foundation’s State and Local Sales Tax Rates, 2026, Louisiana has the highest combined state-and-local sales tax rate at 10.11%, followed by Tennessee at 9.61%, Washington at 9.51%, and Arkansas and Alabama tied at 9.46%. The population-weighted national average is 7.53%. So a seller who triggered nexus in Louisiana three years ago and never registered is looking at a back-tax exposure of roughly 10% of every Louisiana sale, plus penalties and interest.

What happens if you ignore nexus

States aren’t waiting for sellers to figure this out on their own. Pre-audit questionnaires, marketplace data sharing, and inventory tracking from FBA reports give state revenue departments a much clearer picture of who should be registered than they had even five years ago. States like Illinois and Missouri are actively sending these questionnaires now, and ignoring one is what tips an early-stage inquiry into a full audit with penalties and back taxes attached.

| If a state thinks you may have nexus, the first contact is often a questionnaire asking about your inventory locations, sales volume, and platforms. How you respond determines whether it escalates into a full audit. Sellers who don’t respond, or respond inaccurately, face back taxes for the entire lookback period (typically three to four years, sometimes more), penalties layered on top, and interest accruing daily. |

The math on back taxes

A seller who should have registered in Tennessee three years ago, doing $400,000 a year there, is looking at roughly $115,000 in back tax at the state’s 9.61% combined rate, before penalties and interest stack on. Voluntary disclosure agreements (VDAs), where a seller approaches the state first and offers to settle, are usually a far better path than waiting for a questionnaire. Most states will limit the look-back to three or four years and waive penalties in exchange.

How multichannel sellers stay compliant

For sellers under $1M in revenue selling on one or two platforms, manual tracking with a quarterly review can work: pull a sales-by-state report each quarter, compare against the threshold for each state, and register where you’ve crossed it.

That breaks down quickly once a seller is on three or more platforms. Shopify direct sales, Amazon, eBay, Walmart Marketplace, and TikTok Shop don’t share a unified view of a customer’s sales by state. Marketplace facilitators handle their own tax, but these sales still count toward economic nexus thresholds in most states. And the actual tax collected (whether by you, by the marketplace, or by both) has to be reconciled in the accounting system if you want clean books at month-end.

Read our article about multichannel ecommerce accounting.

A workable multistate compliance stack usually involves three layers:

- Source data: clean, well-organized transaction data flowing from each sales channel into your general ledger, with sales tax separated by state and jurisdiction. This is the layer handled by automation tools like Synder, which syncs ecommerce and financial data across 30+ platforms into systems like QuickBooks, Xero, NetSuite, Sage Intacct, and Intuit Enterprise Suite. It applies tax codes at sync time, groups by state for journal entries, and handles marketplace facilitator tax separately so it doesn’t double-count against your Sales Tax Payable.

- Nexus monitoring: a system or process that flags when sales by state are approaching a threshold, so registration happens before exposure piles up. Some sellers do this in a spreadsheet; larger ones use dedicated nexus-tracking tools.

- Filing and remittance: either in-house, through a sales tax compliance provider (TaxJar, Avalara, Numeral, TaxCloud), or via a CPA who specializes in multistate sales tax.

Check out top 10 sales tax automation software.

How automation helps real businesses handle sales tax

A Montreal-based bean-to-bar chocolate company selling into the U.S. through Stripe kept running into tax issues because Canadian provincial taxes and U.S. customer exemptions were not being applied consistently. After setting up Synder’s customizable rules with conditional tax logic, they are now able to apply Quebec or Ontario rates for Canadian buyers while automatically exempting U.S. transactions. The correct tax is applied to each transaction as it comes in, and four different tax types are handled without any manual work.

| The broader takeaway: applying tax rules at the moment data is synced is far more reliable than going back later and trying to fix tax codes in QuickBooks. |

If you want to see how this kind of automation handles your sales tax, book a demo with Synder.

Final thoughts on managing sales tax nexus

The truth about sales tax nexus in 2026 is that it’s no longer a question of whether a multichannel ecommerce seller has nexus in multiple states, but how many, and which. Wayfair settled the legal question almost eight years ago. The follow-on questions about marketplaces, transaction thresholds, digital goods, and how states enforce against unregistered sellers have moved in the same direction since: more states involved, more rules, faster enforcement.

The sellers and finance teams who handle this well share two habits. They review their sales by state on a quarterly basis, not annually, so a threshold crossing doesn’t go unnoticed for nine months. And they invest in clean source data: transactions categorized by state, jurisdiction, and tax code at the point of sync, so that registration, filing, and reconciliation run off the same numbers.

FAQ

Do I have to register in every state where I have customers?

No. You only need to register in states where you have nexus – physical presence, economic activity above the state’s threshold, or another qualifying connection. Selling a few orders into a state without crossing its sales or transaction threshold doesn’t create an obligation, though some sellers register voluntarily in states they expect to grow into.

Does the marketplace facilitator collect sales tax for all my marketplace sales?

In most states, yes. Amazon, Walmart Marketplace, Etsy, eBay, and similar platforms are required to collect and remit sales tax on transactions they facilitate. But sellers should still confirm the platform is registered in the relevant state, count marketplace sales toward their own economic nexus threshold where the state requires it, and record marketplace-withheld tax correctly in their books to avoid double-reporting.

How long do I have to register after I trigger economic nexus?

It depends on the state. Many require registration within 30 to 60 days of crossing the threshold; some require it by the first day of the following calendar month. Once registered, you must begin collecting tax on the next applicable sale. Voluntary disclosure agreements are available in most states for sellers who realize they’ve crossed thresholds in prior periods and want to settle before being audited.

Can I deregister if my sales drop below a state’s threshold?

In some states, yes, but trailing nexus rules in others (e.g., California) require continued collection for a defined period after the activity stops. Always check the specific state’s deregistration rules before stopping collection, and consider getting confirmation from a licensed sales tax advisor.

Does sales tax nexus apply to SaaS or digital products?

Increasingly, yes. About half of U.S. states tax SaaS and digital products explicitly; others apply existing sales tax rules to digital goods through agency guidance. Kentucky began taxing AI-enabled software and SaaS in January 2026 under expanded definitions of prewritten computer software, and several other states have added or clarified digital-goods rules in the last 18 months. SaaS sellers should treat nexus and taxability as two separate questions: nexus tells you whether you’re in the system, and taxability tells you whether your specific product is subject to tax in that state.