In the realm of accounting, GAAP, or Generally Accepted Accounting Principles, represents a collection of commonly-followed accounting rules and standards for financial reporting that dictate how financial transactions and events should be recorded, reported, and interpreted. GAAP provides a framework that ensures consistency, comparability, transparency, and accuracy in financial reporting across different organizations and industries.

Throughout this article, we’ll speak about the world of GAAP, exploring its origins and evolution, core principles, key components, and its significance in the accounting landscape. We’ll also touch upon the challenges and criticisms GAAP faces, and look ahead to recent developments and its future implications. This article is aimed at giving you a comprehensive understanding of how GAAP shapes the foundation of modern accounting practices.

Importance of GAAP in the accounting field

GAAP plays a pivotal role in accounting as it encompasses various rules and concepts that guide how financial transactions should be recorded, reported, and presented. It’s a set of detailed accounting guidelines and standards meant to ensure uniformity, transparency, and accuracy in financial reporting. By providing a standardized framework, GAAP enables accountants, businesses, investors, regulators, and other stakeholders to comprehend and compare financial information effectively. It instills trust and credibility in financial statements, facilitating informed decision-making.

Origins and evolution of GAAP

Historical development of accounting standards

The roots of GAAP can be traced back centuries to the earliest forms of commerce and trade. As economies grew more complex, the need arose for standardized methods of recording financial transactions. Over time, various civilizations developed their own accounting practices, laying the groundwork for the principles we recognize today. The double-entry accounting system, pioneered during the Renaissance, marked a significant milestone in formalizing accounting procedures.

Role of regulatory bodies in shaping GAAP

The refinement and consolidation of accounting principles gained momentum with the establishment of regulatory bodies. These organizations, such as the Financial Accounting Standards Board (FASB) in the United States, assumed the responsibility of setting and updating accounting standards. FASB’s primary objective is to ensure that financial reporting remains consistent, relevant, and reflective of changing economic conditions. These bodies collaborate with experts, industry stakeholders, and international counterparts to refine and harmonize standards.

Transition from principles-based to rules-based standards

The evolution of GAAP witnessed a shift from principles-based standards to rules-based standards and back again. Early accounting guidelines were rooted in overarching principles, providing a framework within which professionals exercised judgment. However, concerns arose over the potential for inconsistent interpretations and applications. This led to the adoption of rules-based standards, characterized by detailed, specific regulations. Yet, such an approach risked becoming overly complex and inflexible. As a response, there has been a recent trend towards principles-based standards that offer guidance while allowing for professional judgment and adaptation to unique circumstances. This ongoing evolution showcases the dynamic nature of GAAP and its responsiveness to the changing needs of the accounting landscape.

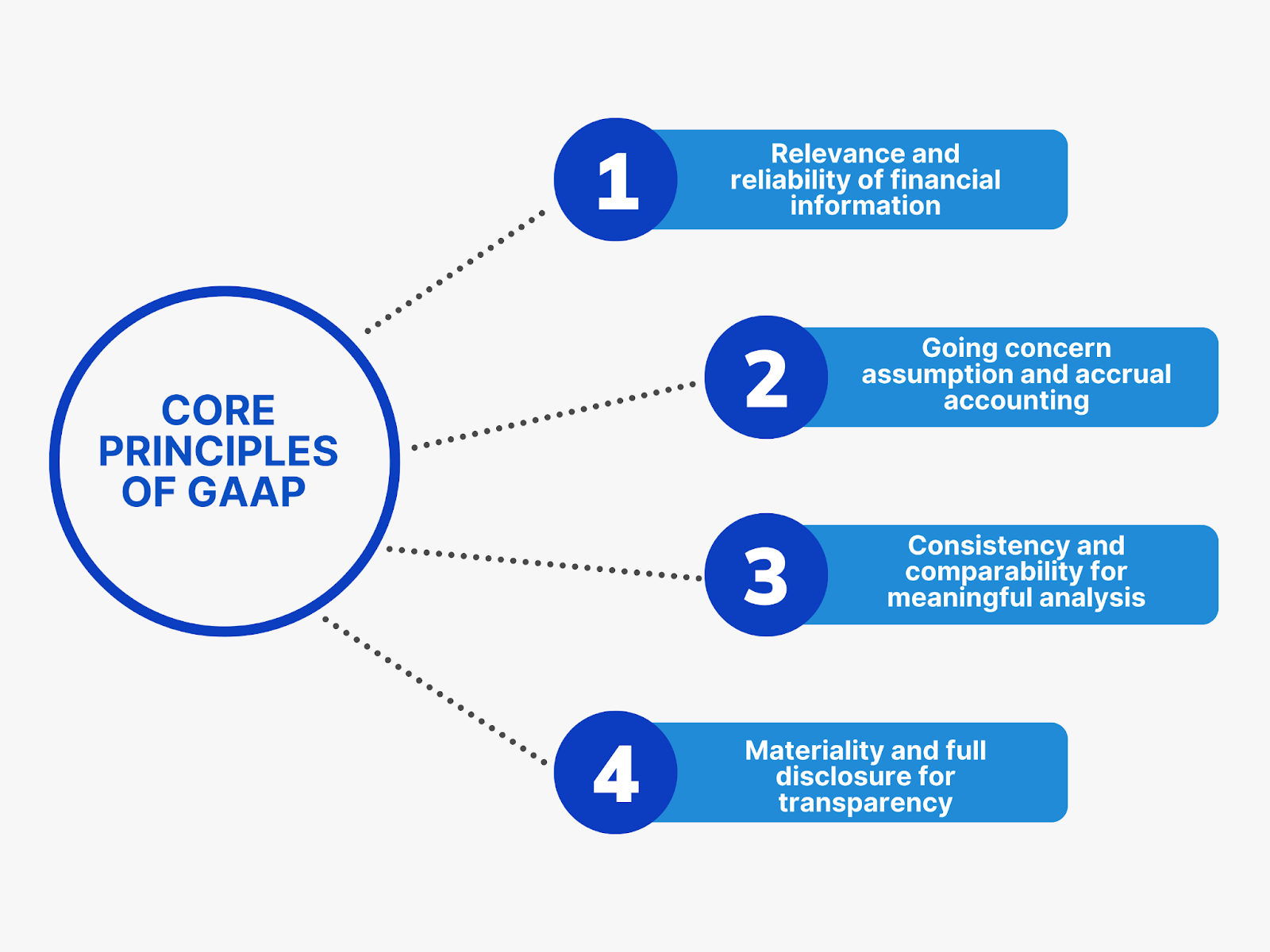

Core principles of GAAP

1. Relevance and reliability of financial information

In the realm of finance and accounting, the terms “relevance” and “reliability” hold immense significance. These two principles serve as the foundation upon which financial information is not only presented but also interpreted and utilized for decision-making. In this article, we delve into the crucial concepts of relevance and reliability, exploring how they shape the accuracy and effectiveness of financial reporting.

Relevance in financial information refers to its ability to influence the decisions made by users of that information. For financial data to be deemed relevant, it must possess predictive or confirmatory value. In other words, it should aid users in making future predictions about a company’s financial performance or confirm their existing expectations.

Relevant financial information is timely and capable of making a difference in the decisions users intend to make. For instance, if an investor is considering purchasing shares in a company, timely and relevant information about the company’s recent financial performance, growth prospects, and industry trends would be crucial in making an informed investment decision.

Reliability, on the other hand, pertains to the faithfulness of financial information. Reliable information is free from bias, faithfully representing the actual economic events and transactions it aims to portray. To be reliable, financial data should be verifiable, ensuring that different knowledgeable observers would reach a consensus about its accuracy.

Reliable financial information is also consistent across different periods, meaning that similar transactions or events are accounted for and reported consistently over time. This consistency ensures that financial statements reflect a true picture of an organization’s financial health and performance.

Balancing relevance and reliability can sometimes present a challenge. For instance, certain estimates and judgments made in financial reporting might enhance relevance but could potentially compromise reliability. Striking the right balance between these two principles is crucial. Decision-makers require information that is not only relevant to their choices but also trustworthy and accurate.

Relevance and reliability work hand in hand to provide decision-makers with the information they need to evaluate opportunities, assess risks, and allocate resources. Relevant information guides decisions toward outcomes that align with organizational goals. Reliable information, on the other hand, ensures that these decisions are based on accurate representations of the company’s financial position and performance.

A tool to ensure relevance and reliability of your financial data

As businesses grow and transactions multiply, the need for effective accounting solutions becomes paramount. This is where Synder Sync steps in, offering a comprehensive solution to simplify and streamline business accounting processes.

Synder Sync is a cutting-edge accounting solution designed to seamlessly integrate with various e-commerce platforms and payment gateways, facilitating the smooth flow of financial data into accounting software. With its user-friendly interface and powerful features, Synder Sync caters to businesses of all sizes, from startups to established enterprises.

Key features and benefits

- Multi-platform integration: Synder Sync integrates with a wide range of ecommerce platforms, marketplaces, and payment gateways, including Shopify, Amazon, eBay, PayPal, Stripe, and more. This versatility ensures that businesses can centralize their financial data regardless of the platforms they utilize.

- Automated data sync: Synder Sync eliminates the manual entry of financial data by automating the synchronization of transactions from ecommerce channels and payment gateways into the books. This not only saves time but also reduces the risk of errors associated with manual data input.

- Transaction categorization: The solution intelligently categorizes transactions based on predefined rules, enhancing accuracy and providing a clear overview of income and expenses.

- Multicurrency support: For businesses operating globally, Synder Sync’s multi-currency support is invaluable. It accurately converts and records transactions in different currencies, offering a comprehensive view of financial performance.

- Tax compliance made easy: Synder Sync simplifies tax compliance by accurately tracking taxes.

- Real-time reporting: With up-to-date reporting capabilities, businesses can access financial insights in real time. This enables informed decision-making and helps identify trends and opportunities.

How Synder Sync works

- Integration: Businesses connect their e-commerce platforms and payment gateways to Synder Sync, allowing the solution to access and sync financial data.

- Automated Sync: Synder Sync automatically retrieves and syncs transaction details, including sales, refunds, fees, and expenses.

- Categorization and Recording: The solution categorizes transactions based on predefined rules and records them in accounting software, such as QuickBooks or Xero.

- Real-Time Updates: Businesses can access real-time financial reports and dashboards, gaining insights into their financial health.

By eliminating manual processes, reducing errors, and enhancing accuracy, Synder empowers businesses to focus on growth and strategic decision-making.

Sign up for a free trial or book a seat at our weekly webinar where Synder specialists will answer all your questions.

2. Going concern assumption and accrual accounting

In accounting, two fundamental principles — going concern assumption and accrual accounting — play a pivotal role in capturing the essence of an organization’s financial reality. In this article, we delve into these essential concepts, understanding how they shape financial statements, provide insights into a company’s health, and enable informed decision-making.

The going concern assumption is a fundamental concept that underlies the preparation of financial statements. It posits that a business will continue its operations in the foreseeable future, allowing for the application of accrual accounting principles. In simpler terms, this assumption implies that unless there’s clear evidence to the contrary, companies are viewed as ongoing concerns with the capacity to meet their obligations and carry out their operations.

The going concern assumption has significant implications for financial reporting. It permits the valuation of assets at historical cost, the recognition of future cash flows from long-term assets, and the amortization of expenses over their useful lives. By assuming continuity, financial statements reflect a more accurate representation of a company’s financial position and performance.

Accrual accounting is a cornerstone of modern financial reporting. Unlike cash accounting, which records transactions when cash changes hands, accrual accounting records transactions when they occur—regardless of when the associated cash is received or disbursed. This method allows for a more accurate reflection of a company’s financial reality by recognizing revenues and expenses when they’re earned or incurred, respectively.

Accrual accounting aligns with the going concern assumption. It enables a more precise depiction of the timing and matching of revenues and expenses, portraying a holistic view of an organization’s financial activities. By doing so, it provides valuable insights into short-term and long-term financial trends and enables stakeholders to assess the company’s financial health and future prospects.

The going concern assumption and accrual accounting share a symbiotic relationship. The former permits the latter to function effectively, as the recognition of revenues and expenses over time assumes a continuous business operation. Together, these concepts enhance the accuracy, transparency, and comparability of financial statements, fostering informed decision-making by stakeholders.

The going concern assumption and accrual accounting are not mere technicalities; they have far-reaching implications for decision-makers. Lenders, investors, and management rely on these principles to make informed choices. Accurate financial statements, underpinned by these concepts, aid in assessing a company’s creditworthiness, growth potential, and risk exposure.

3. Consistency and comparability for meaningful analysis

In financial reporting, the principles of consistency and comparability serve as guiding stars, illuminating the path toward meaningful analysis. These two fundamental concepts ensure that financial information is not only accurate but also intelligible and relevant. In this article, we explore how consistency and comparability weave into the fabric of financial reporting, enabling stakeholders to decipher the story behind the numbers.

Consistency in financial reporting demands that an organization applies the same accounting methods and principles across different reporting periods. It’s about maintaining uniformity in how transactions are recorded, measured, and presented. This approach allows for meaningful year-to-year and period-to-period comparisons, providing insights into trends, changes, and shifts in a company’s financial performance.

Consistency is essential not only for external stakeholders like investors and regulators but also for internal decision-makers. It facilitates the identification of patterns and helps uncover the underlying drivers of financial fluctuations. This principle provides a reliable backdrop against which financial information can be analyzed, ultimately aiding in strategic decision-making.

Comparability takes the notion of consistency a step further. While consistency ensures uniformity within a single entity’s financial reporting, comparability extends this uniformity across multiple entities within the same industry. Comparability allows stakeholders to evaluate a company’s performance against its peers and industry benchmarks, shedding light on its competitive position.

Comparable financial information transcends company boundaries and geographical borders. For investors considering investment opportunities, comparability enables them to gauge the relative attractiveness of different entities. For regulators, it promotes a standardized framework for assessing compliance. In a globalized business landscape, comparability fosters a common language of financial reporting that transcends national accounting standards.

4. Materiality and full disclosure for transparency

Materiality and full disclosure take center stage in financial reporting, working in tandem to foster transparency and provide stakeholders with a comprehensive view of a company’s financial health. These concepts ensure that the right information is presented in the right context, empowering decision-makers to make well-informed choices. In this article, we delve into the significance of materiality and full disclosure, highlighting their role in shaping transparent financial reporting.

Materiality is the compass that guides what information is included in financial statements. It revolves around the principle that financial information should only be disclosed if its omission or misstatement could influence the economic decisions of users. In other words, materiality seeks to highlight information that has the potential to impact an entity’s financial position or performance in a significant way.

Materiality’s impact extends beyond mere numbers. It underscores the importance of context and relevance. By focusing on material information, financial statements avoid clutter and ensure that stakeholders’ attention is directed to what truly matters. This principle prevents the drowning of significant information in a sea of data, allowing users to make decisions based on insights that can lead to meaningful outcomes.

Full disclosure is the practice of providing all relevant and necessary information in financial statements and accompanying notes. This principle ensures that stakeholders have a complete understanding of a company’s financial position and performance, even if the information might not be deemed “material” in isolation. Full disclosure paints a comprehensive picture, enabling users to assess risks, potential obligations, and future prospects accurately.

Full disclosure also includes the transparency of off-balance sheet items and contingent liabilities. These are potential obligations that might arise in the future due to existing conditions. By disclosing these, financial statements provide a holistic view of the company’s financial obligations, ensuring that stakeholders can assess risks comprehensively.

Materiality and full disclosure are intertwined in the pursuit of transparent financial reporting. Materiality ensures that the most significant information takes center stage, while full disclosure guarantees that all pertinent information is available to stakeholders who seek a deeper understanding. Together, they create a balance that allows stakeholders to form accurate perceptions of a company’s financial position and the risks it faces.

Materiality and full disclosure serve as tools that empower stakeholders to make well-informed decisions. Investors, creditors, regulators, and analysts rely on these principles to assess a company’s risk profile, financial performance, and prospects accurately. By adhering to these principles, companies not only fulfill their ethical responsibilities but also bolster their credibility and foster trust among stakeholders.

These core principles collectively form the framework upon which GAAP is built, guiding accountants and organizations in their pursuit of accurate and meaningful financial reporting.

Key components of GAAP

Balance sheet

A balance sheet is a financial statement that gives a picture of a company’s financial performance at a definite point in time. It presents a summary of an organization’s assets, liabilities, and shareholders’ equity, indicating how the company’s resources are financed and allocated. The balance sheet is a fundamental component of financial reporting and offers insights into a company’s financial health, solvency, and overall stability.

The equation for a balance sheet i as follows:

Assets = Liabilities + Shareholders’ Equity

Here’s a breakdown of the key components:

- Assets: These are the resources owned or controlled by the company, which have economic value and can be used to generate future benefits. Assets are typically categorized into current assets (such as cash, accounts receivable, and inventory) and non-current assets (such as property, equipment, and long-term investments).

Liabilities: These are debts and obligations that the company owes to other parties. Liabilities are categorized into current liabilities (such as accounts payable, short-term loans, and accrued expenses) and non-current liabilities (such as long-term debt and deferred tax liabilities). - Shareholders’ equity: Aka net worth or owners’ equity, represents the interest in the company’s assets after its liabilities have been deducted. It includes common stock, retained earnings, additional paid-in capital, and other components that reflect the ownership interests of the company’s shareholders.

The balance sheet presents a crucial insight into the company’s financial structure and its ability to meet its obligations. It also helps stakeholders assess the company’s liquidity, leverage, and overall financial health. Changes in the balance sheet over time can indicate trends in a company’s financial performance and its ability to manage its resources effectively.

Income statement

An income statement, also known as a profit and loss (P&L) statement, is a financial statement that provides a summary of a company’s revenues, expenses, and profits or losses over a specific period of time. The income statement is a vital tool for assessing a company’s financial performance and its ability to generate profits from its core operations.

The primary purpose of the income statement is to show how much money a company earned (revenues), how much it spent (expenses), and the resulting net income or net loss for a certain period, like a month, a quarter, or a year.

The structure of an income statement typically includes the following components:

- Revenues or sales: This section lists the total amount of money generated from selling goods, providing services, or any other business activities. Revenues are sometimes broken down by categories such as product lines or geographic regions.

- Cost of goods sold (COGS): This category includes the direct costs associated with producing or delivering the goods or services sold. It encompasses expenses like raw materials, labor, and manufacturing costs. Subtracting COGS from revenues gives the gross profit.

- Gross profit: This is the difference between total revenues and the cost of goods sold. It represents the amount of money the company has left after accounting for the direct costs of production.

- Operating expenses: Operating expenses include various costs incurred in the day-to-day operations of the business. These may include expenses like salaries, marketing costs, rent, utilities, and administrative expenses.

- Operating income or operating profit: This is calculated by subtracting operating expenses from the gross profit. It depicts the company’s core operations profitability before you consider taxes and interest.

- Other income and expenses: This section includes income or expenses not directly related to the company’s core operations. It might include interest income, interest expenses, gains or losses from the sale of assets, and more.

- Income before taxes: This figure is obtained by adding or subtracting other income and expenses from the operating income. It represents the company’s profit or loss before accounting for income taxes.

- Net income or net profit: Also referred to as the “bottom line,” net income is the final figure on the income statement. It’s calculated by subtracting income taxes from the income before taxes. A positive net income indicates the company’s profitability, while a negative net income signifies a net loss.

The income statement provides valuable insights into a company’s revenue-generating capabilities, expense management, and overall profitability. By analyzing trends and changes in revenues, expenses, and net income over different periods, stakeholders can gauge a company’s financial performance, efficiency, and potential for growth.

Cash flow statement

A cash flow statement is a financial statement that provides a detailed summary of the cash inflows and outflows within a company over a specific period of time. It presents a clear picture of how cash is generated and used by the business, offering insights into its liquidity, operating activities, investing activities, and financing activities.

The primary purpose of the cash flow statement is to help stakeholders understand the company’s ability to generate cash, meet its financial obligations, and support its various activities. Unlike the income statement, which focuses on profits and losses, the cash flow statement emphasizes the actual movement of cash in and out of the business.

There are usually three sections in a cash flow statement:

- Operating activities: This section includes cash flows related to the company’s core operating activities, such as the buying and selling of goods and services. It involves cash transactions from sources like customer payments, supplier payments, and operating expenses. The net cash provided by or used in operating activities reflects the company’s ability to generate cash from its main business operations.

- Investing activities: This section covers cash flows related to investments in assets that are not intended for immediate resale. It includes purchases and sales of long-term assets like property, equipment, and investments in securities. Cash flows from investing activities provide insights into how the company is managing its capital expenditures and growth initiatives.

- Financing activities: This section focuses on cash flows related to the company’s financing and capital structure. It includes transactions involving the company’s owners (equity) and creditors (debt). Common financing activities include issuing or repurchasing stock, borrowing or repaying loans, and paying dividends. Cash flows from financing activities reflect changes in the company’s capital and debt structure.

The cash flow statement ultimately provides a reconciliation between the opening and closing balances of the company’s cash and cash equivalents. It ensures that the changes in cash during the period are explained by the various operating, investing, and financing activities.

The cash flow statement is a valuable tool for assessing a company’s cash-generating ability, its ability to meet its financial obligations, and its financial flexibility. By analyzing the cash flow statement, stakeholders can gain insights into a company’s financial health and its ability to sustain operations, invest in growth, and manage its debt obligations.

Notes to financial statements

While financial statements provide a structured overview of a company’s financial health, the “Notes to Financial Statements” section serves as a treasure trove of additional information that enhances understanding and clarity. In this article, we delve into the significance of these notes and how they offer valuable insights to stakeholders seeking a deeper comprehension of a company’s financial position and performance.

The “Notes to Financial Statements” section is a critical component of financial reporting. It accompanies the main financial statements (balance sheet, income statement, and cash flow statement) and provides explanations, details, and disclosures that complement the presented figures. The notes help clarify accounting policies, assumptions, uncertainties, contingencies, and significant events that may impact the interpretation of financial data.

The primary purpose of the notes is to offer clarity on complex accounting treatments and to provide context for the reported numbers. They help readers understand the underlying reasons for certain financial figures, thus preventing misinterpretation or confusion. For example, notes may elaborate on the methods used for inventory valuation, the depreciation schedule for assets, or the recognition of revenue in long-term contracts.

Notes to the financial statements often disclose the significant accounting policies adopted by the company. These policies explain the choices made by the company in measuring and presenting financial information. This disclosure is crucial because different accounting policies can lead to varying financial results. By understanding these policies, stakeholders can better assess the implications of accounting choices on the reported numbers.

Notes also highlight potential contingencies and risks that may impact a company’s financial future. Contingencies can include pending legal cases, warranty obligations, environmental liabilities, and more. By disclosing these contingencies, companies provide stakeholders with a comprehensive view of potential future financial obligations and risks that might affect decision-making.

Notes may also include information about subsequent events that occurred after the end of the reporting period but before the financial statements were finalized. These events could have a material impact on the company’s financial position and performance and are therefore disclosed to ensure that stakeholders have the most up-to-date information.

Transactions with related parties, such as key management personnel and entities under common control, are often disclosed in the notes. These transactions could potentially create conflicts of interest, and disclosure allows stakeholders to assess their potential influence on the company’s financial outcomes.

In cases where a company engages in complex financial instruments or contracts, such as derivatives or lease agreements, the notes provide details about their nature, terms, risks, and potential impact on financial results.

The notes section serves as a bridge between the technical aspects of accounting and the practical implications for stakeholders. They empower investors, analysts, creditors, and regulators to make well-informed decisions based on a deeper understanding of a company’s financial information. The insights provided by the notes allow stakeholders to evaluate risks, assess the quality of earnings, and comprehend the broader context surrounding reported figures.

On the whole, the notes to financial statements aren’t mere footnotes; they’re vital components of transparent and informative financial reporting. By offering supplementary information, clarifying accounting treatments, and disclosing critical details, these notes provide a holistic view of a company’s financial position and performance. As stakeholders navigate the complexities of financial information, the notes stand as beacons of insight, guiding them toward decisions rooted in a comprehensive understanding of a company’s financial reality.

These key components of GAAP ensure that financial statements accurately reflect an organization’s financial position, performance, and cash flows, allowing stakeholders to make informed decisions.

Importance of GAAP compliance

Ensuring accurate and reliable financial reporting

GAAP compliance is the cornerstone of accurate and reliable financial reporting. By adhering to standardized principles and guidelines, organizations can consistently record and present financial transactions in a manner that reflects their true economic reality. This accuracy bolsters the credibility of financial statements and contributes to informed decision-making by stakeholders.

Facilitating investor and stakeholder confidence

Investors and stakeholders heavily rely on financial information to assess the financial health and performance of an organization. When companies follow GAAP, they provide a consistent and transparent basis for assessing their financial standing. This, in turn, instills confidence among investors and stakeholders, as they can trust the information presented in financial statements for evaluating investment opportunities and business partnerships.

Legal requirements guiding the performance of publicly traded companies

Publicly traded companies are bound by legal and regulatory requirements to adhere to GAAP. Regulatory bodies and securities commissions mandate the use of GAAP-compliant financial statements for external reporting, ensuring a level playing field for investors. Compliance with GAAP assists these companies in meeting these legal obligations and avoiding potential legal repercussions.

Enhancing borrowing and financing opportunities

Financial institutions and lenders often require GAAP-compliant financial statements when evaluating loan applications and financing proposals. Compliance with GAAP lends credibility to an organization’s financial information, increasing its eligibility for favorable borrowing terms and financing opportunities.

Standardizing global financial reporting

GAAP compliance also contributes to global financial reporting consistency. As companies operate in a globalized economy, adherence to consistent accounting standards aids in comparing financial information across borders and jurisdictions. It fosters a common language for financial reporting, making cross-border business activities and investments more manageable.

Minimizing fraud and mismanagement

GAAP’s structured guidelines help detect and prevent financial irregularities and fraudulent activities. The transparency and accountability promoted by GAAP discourage manipulative reporting practices, reducing the risk of financial mismanagement and misconduct.

Supporting internal decision-making

Beyond external reporting, GAAP compliance benefits organizations internally. It aids in the generation of accurate management reports, which in turn support strategic decision-making. By adhering to consistent accounting principles, companies can better understand their financial position and plan for the future.

Adhering to GAAP principles isn’t just about regulatory compliance; it’s about maintaining financial integrity, transparency, and accountability that extend to all aspects of an organization’s operations and relationships with stakeholders.

GAAP vs. IFRS (International Financial Reporting Standards)

Key differences between GAAP and IFRS

GAAP and IFRS are two prominent accounting frameworks used globally. While they share common objectives of providing reliable financial information, they differ in various aspects. Some key differences include:

- Standard-Setting Bodies: GAAP standards are set by country-specific bodies, like FASB in the U.S., while IFRS is overseen by the International Accounting Standards Board (IASB).

- Principles vs. Rules: GAAP often employs rules-based standards, while IFRS leans more towards principles-based standards, allowing for professional judgment and interpretation.

- LIFO vs. FIFO: GAAP permits the use of Last-In, First-Out (LIFO) inventory costing, while IFRS does not allow LIFO.

- Inventory Valuation: IFRS allows the reversal of inventory write-downs, but GAAP doesn’t.

- Research and Development Costs: IFRS allows for capitalization of certain development costs, while GAAP is more stringent in this area.

- Lease Accounting: IFRS and GAAP previously had different lease accounting models, but recent changes have brought them closer in alignment.

- Impairment Testing: GAAP and IFRS have differing approaches to assessing impairment of assets.

Global adoption trends and challenges

The global financial landscape has seen a movement towards IFRS adoption in recent years. Many countries have transitioned or are in the process of transitioning from their local GAAP to IFRS. This adoption trend is driven by the need for uniformity in financial reporting, especially for multinational companies. However, challenges exist in the form of differing cultural, legal, and business environments, which may impact the application and interpretation of IFRS.

Convergence efforts to harmonize standards

Given the benefits of uniform accounting standards, there have been efforts to converge GAAP and IFRS where possible. Convergence aims to reduce discrepancies between the two frameworks, making it easier for companies to navigate international business activities. While some progress has been made, full convergence remains challenging due to the inherent differences between the systems and the complexities of their implementation.

Impact on investors and stakeholders

The differences between GAAP and IFRS can lead to variations in reported financial figures. This poses challenges for investors and stakeholders trying to compare companies across different regions. The ongoing evolution and potential convergence of these standards aim to address this issue and provide a more seamless global financial reporting environment.

Future prospects and potential benefits

The continued alignment and convergence of GAAP and IFRS could potentially lead to improved consistency, comparability, and transparency in global financial reporting. Such harmonization would simplify cross-border investments and business activities, benefiting both companies and investors in a more interconnected world economy.

Understanding the distinctions and commonalities between GAAP and IFRS is essential for businesses operating on a global scale and for investors seeking accurate and comparable financial information.

Challenges and criticisms of GAAP

Complexity and rigidity of certain standards

One challenge faced by GAAP is the complexity of some accounting standards. As businesses grow and evolve, transactions can become intricate, requiring intricate accounting treatment. This complexity can lead to confusion, errors, and increased costs for implementation. Additionally, the rigidity of certain standards can make it challenging for companies to adapt to unique circumstances, potentially resulting in financial statements that don’t accurately represent economic realities.

Interpretation issues leading to inconsistent application

The principles-based nature of GAAP can lead to varying interpretations by different organizations and even among accounting professionals within the same organization. This inconsistency in application can erode the comparability of financial statements and create confusion among users. Furthermore, interpretations may change over time, leading to shifts in reported financial figures that aren’t reflective of actual changes in the underlying business operations.

Addressing emerging areas like cryptocurrency and intangible assets

The rapid pace of technological advancements presents challenges for GAAP, which may struggle to keep up with emerging business practices. For instance, accounting for cryptocurrency transactions and valuing intangible assets like intellectual property can be complex and subject to debate. As the business landscape evolves, GAAP must continually adapt to encompass new financial instruments and assets, maintaining its relevance and applicability.

Lack of global standardization

While GAAP is widely followed in various countries, differences persist due to the varying accounting principles set by different standard-setting bodies. This lack of global standardization can complicate cross-border financial reporting and hinder international comparability. This challenge has prompted calls for greater convergence between GAAP and other frameworks like IFRS.

Costs and burdens of compliance

Adhering to GAAP standards can be resource-intensive for businesses. Implementing complex rules, training staff, and updating systems to stay compliant can result in significant costs. Smaller businesses might find it particularly challenging to keep up with changing standards, potentially leading to errors or non-compliance.

Balancing principles and rules

The ongoing debate between principles-based and rules-based accounting standards raises questions about striking the right balance. While principles-based standards allow for professional judgment and flexibility, they can also lead to inconsistent interpretations. On the other hand, rules-based standards risk becoming overly prescriptive and failing to address unique business situations.

Difficulty in keeping pace with business evolution

The business environment is constantly evolving, with new business models, industries, and financial instruments emerging. GAAP may struggle to keep pace with these changes, leading to delayed guidance or retroactive adjustments that can disrupt financial reporting and decision-making.

Addressing these challenges is essential for maintaining the effectiveness and relevance of GAAP in an ever-changing business landscape. As technology, industries, and markets evolve, the accounting standards must be agile enough to capture economic realities accurately.

Recent developments and future outlook

Impact of technology on accounting standards

The digital revolution is reshaping accounting practices. Automation, artificial intelligence, and blockchain are transforming how financial transactions are recorded, analyzed, and reported. While these technologies offer efficiency gains, they also raise questions about data security, privacy, and the need for new accounting standards to accommodate novel transaction methods, such as cryptocurrency and smart contracts.

Sustainability reporting and its integration into GAAP

Increasingly, businesses are recognizing the importance of sustainability and environmental, social, and governance (ESG) factors. There is a growing demand for transparent reporting on these aspects. Integrating sustainability reporting into GAAP would provide a standardized framework for businesses to disclose their ESG performance. This integration aligns with the evolving expectations of investors, regulators, and society at large.

Potential reforms and updates to adapt to changing business landscape

The accounting landscape is constantly evolving, driven by globalization, digital transformation, and shifts in business models. To stay relevant, GAAP may undergo reforms and updates. These could include:

- Streamlining Complex Standards: Addressing complexity by simplifying certain standards and reducing the burden of implementation.

- Flexibility and Interpretation: Balancing principles with clearer guidance to minimize inconsistencies in application.

- Embracing Emerging Areas: Adapting to new challenges like valuing intellectual property, intangible assets, and digital goods.

- Convergence and Harmonization: Collaborating with international standard-setting bodies to achieve greater global consistency.

- Enhancing Disclosure: Encouraging more comprehensive disclosure to provide a clearer picture of a company’s financial position and risks.

Digital reporting and standardization

The move toward digital financial reporting, such as XBRL (eXtensible Business Reporting Language), is streamlining the process of preparing and analyzing financial statements. The future may see more sophisticated technologies that allow real-time reporting and predictive analysis, enabling stakeholders to make informed decisions with up-to-date information.

Ethical and social implications

As technology continues to shape the future of accounting, ethical considerations become paramount. Issues like data privacy, cybersecurity, and the ethical use of AI in decision-making processes must be addressed in tandem with technological advancements.

Continual evolution for relevance

GAAP’s ongoing evolution reflects its commitment to maintaining relevance in a rapidly changing world. Adaptations, reforms, and innovations will help ensure that accounting standards effectively capture the complexities of modern business practices and provide meaningful insights to stakeholders.

Looking ahead, GAAP’s ability to embrace technology, sustainability, and evolving business dynamics will play a pivotal role in shaping the future of financial reporting and decision-making.

Conclusion

GAAP’s enduring role as a bedrock of financial integrity can’t be overstated. By providing a structured framework for recording and reporting financial transactions, GAAP ensures that financial statements are accurate, reliable, and comparable. It serves as a foundation upon which investors, stakeholders, regulators, and businesses make informed decisions and navigate the complex world of finance.

As GAAP continues to evolve in response to technological advancements, emerging business practices, and global demands for transparency, it’s essential for accountants, businesses, and stakeholders to stay current with its guidelines. Continuous learning, adapting to changes, and embracing new standards will empower professionals to navigate the challenges and harness the opportunities presented by a rapidly changing financial landscape.

Overall, GAAP’s principles, flexibility, and commitment to transparency make it an indispensable tool for maintaining trust and credibility in financial reporting. As we move forward, let us recognize the dynamic nature of GAAP and its role in shaping the future of accounting practices worldwide.

Read more about What is forensic accounting.