A founder checks the bank balance every Monday morning and feels good about the number. Then the P&L arrives at month-end showing a loss, the lender asks why the margins compressed two quarters in a row, and a tax bill comes in that doesn’t match anything on the books. None of that necessarily means the business is failing, but it does mean the bank balance was telling a very different story from the financial statements everyone else relies on.

This guide is for business owners, founders, and controllers who want to be fluent in what their books are doing without becoming bookkeepers themselves. You’ll get the accounting equation, double-entry, the six account types, cash vs. accrual, the three financial statements, the principles and assumptions behind GAAP and IFRS, the eight-step accounting cycle, and the point in the process where automation removes most of the manual work.

TL;DR

- The accounting equation always balances: every transaction your business records touches at least two accounts and keeps assets equal to liabilities plus equity.

- Cash vs. accrual is the biggest method choice: cash tracks money in and out; accrual matches revenue to the period it was earned.

- The three financial statements answer different questions: the balance sheet, income statement, and cash flow statement each show a different angle of the same business.

- GAAP and IFRS stand behind the principles you apply: revenue recognition, expense matching, conservatism, going concern, and others guide consistent reporting.

- Manual entry is where books break: reconciliation and categorization across platforms cause most errors, and businesses that automate them cut close time 30–50%.

How many types of accounting are there, and which one matters for you?

Accounting is a family of related disciplines, not one. For an SMB owner, three of them carry the daily weight:

- Financial accounting (how transactions become reports for outside readers)

- Managerial accounting (how those numbers inform internal decisions)

- Bookkeeping (the day-to-day capture that everything else depends on)

Tax accounting and audit are related specialties you’ll work with periodically, usually through a CPA. This guide covers financial accounting and the basics every business owner should be fluent in.

Related read: Retail accounting: how it works, where it breaks, and what it costs you.

What principles and assumptions stand behind GAAP?

Modern accounting standards trace back to the 1929 stock market crash. The Securities Acts of 1933 and 1934 required public companies to publish audited financial statements, and the FASB has set US GAAP since 1973. The principles below are what those standards require any business reporting under GAAP to follow. The AICPA maintains the professional standards that CPAs follow in applying them.

1. Revenue recognition principle. Record revenue when it’s earned, not when cash is received. This is the foundation of accrual accounting. Under the current ASC 606 standard (and its IFRS 15 counterpart), revenue is recognized through a five-step process: identify the contract, identify the performance obligations in it, determine the transaction price, allocate that price across the obligations, and recognize revenue as each obligation is satisfied. The model matters most for subscription, multi-element, and long-term contract businesses, where cash and earned revenue rarely line up.

2. Expense matching principle. Match expenses to the revenue they helped generate in the same period. If you pay for inventory in October that sells in December, the cost is recorded your books in December.

3. Cost principle. Record assets at their original purchase cost, not their current market value. Your equipment appears on the balance sheet at what you paid for it, minus accumulated depreciation.

4. Full disclosure principle. Financial statements must include all information a reader would need to make an informed decision. Nothing material can be hidden.

5. Objectivity principle. Accounting records must be based on objective, verifiable evidence: invoices, receipts, contracts, not estimates or opinions.

6. Going concern. The assumption that a business will continue operating for the foreseeable future. This drives how you value assets and recognize long-term obligations. If going concern is in doubt, financial statements must disclose it.

7. Consistency. The same accounting methods are applied period over period so results are comparable. If you change a method, you disclose the change and its effect. Disclose any change in method in the period you make it.

8. Materiality. Small errors or omissions that wouldn’t change a reader’s decision don’t need to be corrected. Material items must be.

9. Conservatism. When two methods could apply, choose the one that’s less likely to overstate income or assets. Recognize losses early; recognize gains only when realized.

10. Economic entity. The business’s transactions are kept separate from the owner’s personal finances and from any related entities. This is what makes an LLC’s books recognizable as the LLC’s, not the founder’s.

Together these principles and assumptions are what make one company’s financial statements legible to another company’s investors, auditors, and lenders.

GAAP vs. IFRS: how the two standards compare

US GAAP is rules-based and set by the FASB; it’s used by US public companies and most US private companies that report externally. IFRS is principles-based and used in 140+ countries including the EU, UK, Canada, Australia, and most of Asia.

For an SMB, GAAP applies if you operate in the US and produce financials for lenders, investors, or auditors. IFRS applies if you operate or report internationally. The differences matter most in inventory valuation, revenue recognition under specific contract types, and lease accounting.

| Dimension | GAAP (US) | IFRS (international) |

| Approach | Rules-based | Principles-based |

| Standard setter | FASB | IASB |

| Inventory valuation | LIFO allowed | LIFO not allowed |

| Used in | US | 140+ countries |

| Revenue recognition | ASC 606 | IFRS 15 (substantially converged) |

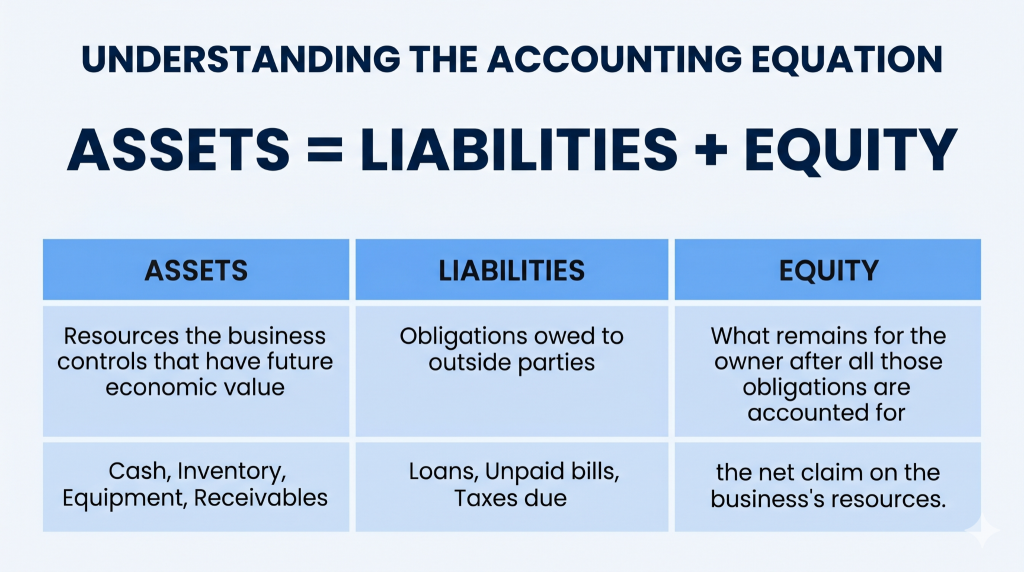

What is the accounting equation and why does it always balance?

Every concept in financial accounting traces back to one key principle: what your business owns must equal what it owes. Not approximately, exactly.

That’s the accounting equation: Assets = Liabilities + Equity.lities + Equity.

- Assets are resources your business controls that have future economic value: cash, inventory, equipment, receivables.

- Liabilities are obligations owed to outside parties: loans, unpaid bills, and taxes due.

- Equity is what remains for the owner after all those obligations are accounted for, the net claim on the business’s resources.

This equation is built into every transaction your business records, so it always stays in balance. If it ever doesn’t, something in the records is off. Start every transaction analysis by asking which side of the equation it touches.

A simple example:

- Put $5 of your own money into a new business: assets (cash) = $5, equity = $5, balanced.

- Borrow $10 from a bank: assets rise to $15, liabilities rise to $10, equity stays at $5, still balanced.

- Spend that $10 on equipment: cash drops by $10, equipment rises by $10, total assets unchanged at $15, balanced again.

Every transaction reshuffles the numbers, but the equation holds throughout.

Equity is the account type most owners misread. It’s tempting to think of it as profit, or as the money you’ve personally put into the business, but it’s neither. Equity is a residual claim: it’s what’s mathematically left after all obligations are subtracted from all assets. That number can grow through retained profits, shrink through owner withdrawals, or stay flat even during a profitable year if cash is being reinvested into assets. Watching equity over time is often more informative than watching revenue.

So if every transaction keeps the equation balanced, how does the software know?

How does double-entry bookkeeping catch errors single-entry can’t?

If the accounting equation must always balance, then every transaction recorded in your books needs to keep it that way. That’s the logic behind double-entry bookkeeping: every financial event touches at least two accounts simultaneously, with equal and opposite effects on each side of the equation.

Accountants label these two sides debits and credits.

- A debit records where value is going, the receiving account.

- A credit records where value is coming from, the source.

One thing that often confuses business owners: debits and credits can feel backwards compared to your bank account. When money comes in, your bank shows a credit, but that’s from their side, since your balance is something they owe you. In your books, the same deposit is a debit to cash, because it’s money your business now has. Same transaction, two perspectives.

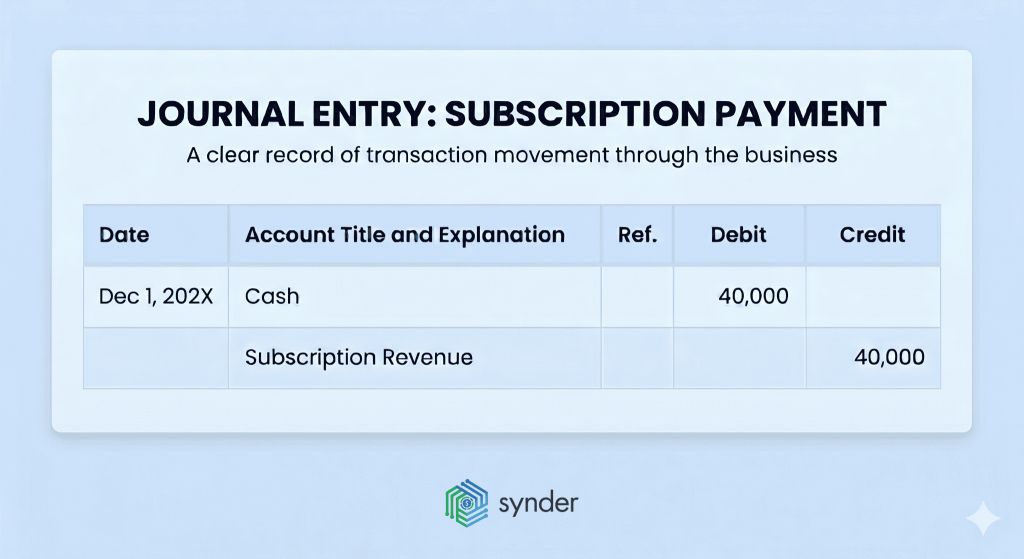

In practice, every transaction becomes a journal entry, a simple record of what changed and where it went. If your business collects $40,000 in subscription payments, cash goes up, so it’s debited, and subscription revenue is credited. Both sides balance, and you have a clear record of how that money moved through the business. Check that every entry has two sides before posting.

| One persistent misconception beginners bring to accounting is that debits are bad and credits are good, probably because of how banks use the terms on statements. In accounting, neither word carries any judgment. Think of debits and credits as the two ends of a pipe: value flows from a source (credit) to a destination (debit). |

Why double-entry catches errors early

This structure is why your accounting software flags issues immediately, since every entry has to balance. Before software, bookkeepers used a trial balance to check that total debits and credits matched, and if they didn’t, something was wrong.

In practice, most errors come from manual entries or spreadsheets where one side is missed. Double-entry bookkeeping, especially when automated, prevents that by forcing every transaction to stay balanced from the start.

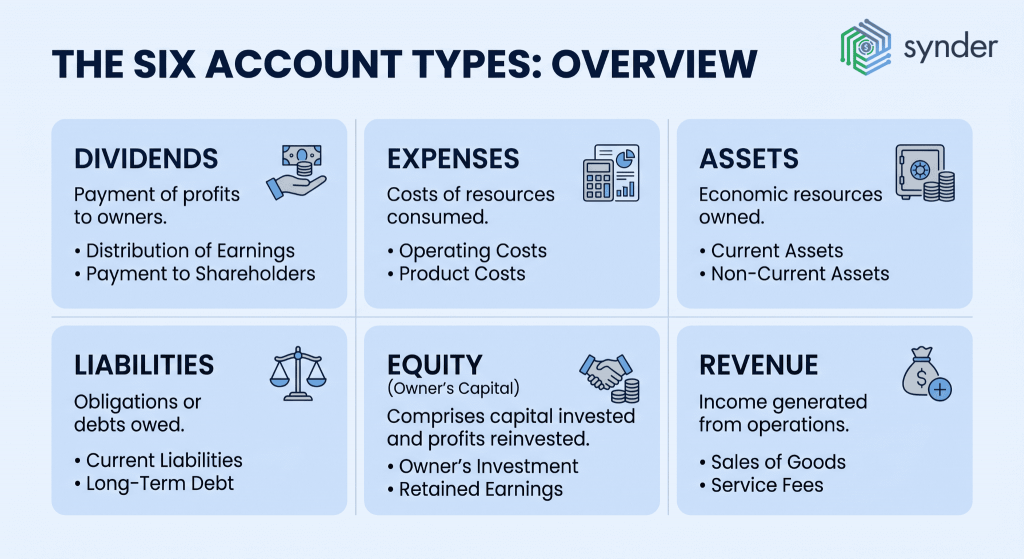

What are the six account types every transaction maps to?

Every transaction in your business maps to one of six account types. Three mirror the accounting equation directly: assets, liabilities, and equity. Three others feed into equity over time: revenue, expenses, and withdrawals (also called dividends in corporate structures).

Each account type has what accountants call a normal balance, the side (debit or credit) that increases it. A helpful way to remember which is which is the mnemonic DEALER, where each letter represents an account type:

- Dividends

- Expenses

- Assets

- Liabilities

- Equity (owner’s equity paid in)

- Revenue

The first three (dividends, expenses, assets) are debit-normal: they grow when debited and shrink when credited. The last three (liabilities, equity, revenue) are credit-normal: they grow when credited and shrink when debited. Keeping this straight removes most of the confusion around why specific transactions are recorded the way they are.

Temporary vs permanent accounts

There’s also an important distinction between temporary and permanent accounts:

- Revenue, expense, and dividend (withdrawal) reset to zero at year-end, and their accumulated balances transfer to retained earnings in equity, which is how a year’s profit gets captured on the balance sheet.

- Asset, liability, and equity accounts carry their balances forward indefinitely.

This is what “closing the books” means: resetting the temporary accounts so the new period starts clean, while the permanent ones preserve the business’s running financial history.

| Account type | Normal balance | Examples | Temporary or permanent |

| Assets | Debit | Cash, inventory, equipment, accounts receivable | Permanent |

| Liabilities | Credit | Loans payable, accounts payable, taxes payable | Permanent |

| Equity | Credit | Owner’s equity, retained earnings | Permanent |

| Revenue | Credit | Sales, subscription income, service fees | Temporary |

| Expenses | Debit | Rent, payroll, cost of goods sold, platform fees | Temporary |

| Withdrawals / dividends | Debit | Owner draws, dividend distributions | Temporary |

For ecommerce and retail businesses in particular, the expense accounts tell a detailed story: platform fees from Shopify or Amazon, payment processing costs from Stripe or PayPal, returns and refunds, shipping costs, and COGS are recorded here. Getting these categorized correctly from the start determines whether your profit margins look accurate or misleading.

Knowing the account types is the framework. So when does the timing of such entries matter?

Cash vs accrual accounting: which method should you use?

This is where many business owners realize their books don’t reflect reality, and it’s one of the most commonly misunderstood concepts in basic accounting.

Cash accounting records income when cash arrives and expenses when cash leaves. Simple, intuitive, and easy to maintain. The problem is that it ties your financial picture entirely to when money moves, and it doesn’t always match when the underlying economic activity actually happened.

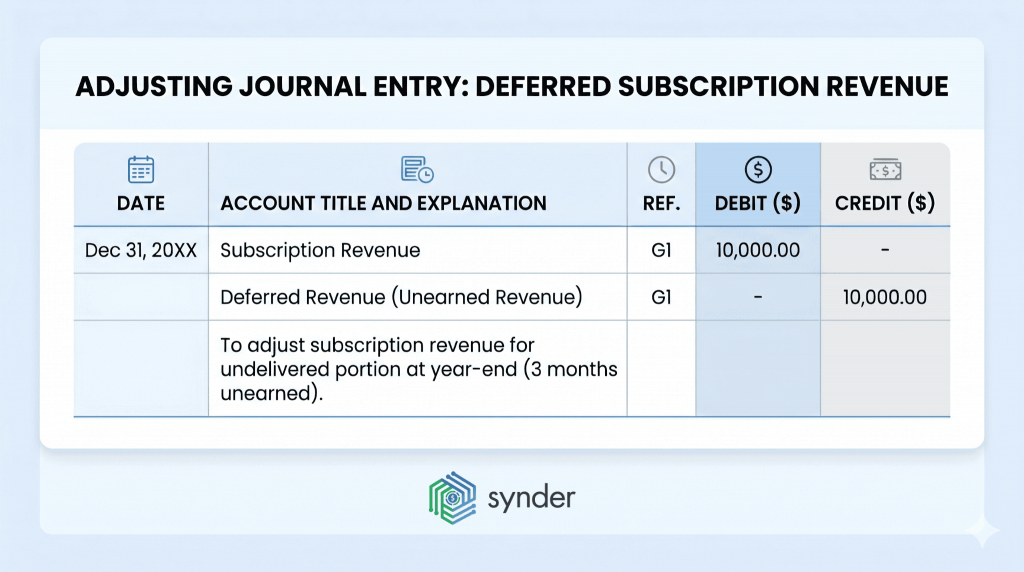

Accrual accounting records revenue when it’s earned and expenses when they’re incurred, regardless of when cash changes hands. For example, a business that collects $40,000 in annual subscription fees in March, for a service that runs April through March the following year, hasn’t actually earned all $40,000 in March. Under accrual, only the portion covering March gets recognized immediately; the remaining amounts are recorded as deferred revenue liability until earned monthly as the service is delivered.

The correction mechanism is adjusting entries: journal entries made at period-end to realign the books with what was actually earned or incurred. In the subscription example above, three months’ worth of revenue ($10,000) would be moved out of income and into deferred revenue at year-end, because that service hasn’t been delivered yet. It’s a small mechanical step that makes a significant difference to how profit is reported.s reported.

Cash vs accrual at a glance

| Dimension | Cash basis | Accrual basis |

| When revenue is recorded | When cash is received | When revenue is earned |

| When expenses are recorded | When cash is paid | When expenses are incurred |

| Required by GAAP/IFRS? | No (for external statements) | Yes |

| IRS requirement | Allowed under $32M gross receipts | Required above $32M |

| Best for | Sole proprietors, very small businesses | Growing companies, investors, lenders |

| Shows | Cash flow | Economic activity |

Which accounting method to choose

Both GAAP and IFRS require accrual accounting for financial statements intended for external use. The IRS generally requires businesses with gross receipts above $32 million to use accrual accounting for tax purposes as well. Below that threshold, many small businesses stay on cash basis, but anyone seeking outside investment, applying for a loan, or preparing for a sale will typically need accrual-basis statements.

The practical implication for ecommerce businesses is significant. A Shopify store that pre-sells inventory or runs subscription boxes, a SaaS business with annual plans, a wholesale brand with net-30 payment terms, all of them will show very different financial pictures under cash vs. accrual accounting. Choose accrual the moment you take on inventory, deferred revenue, or a lender that will read your books.

Switching from cash to accrual mid-stream is more disruptive than most owners expect. It requires restating prior periods, reclassifying revenue that was already recognized, and often filing Form 3115 with the IRS to get approval for the method change. The earlier a business adopts accrual, the less painful that transition becomes. Waiting until a lender or investor requires it is the most expensive time to make the switch.

Learn more about cash and accrual accounting methods.

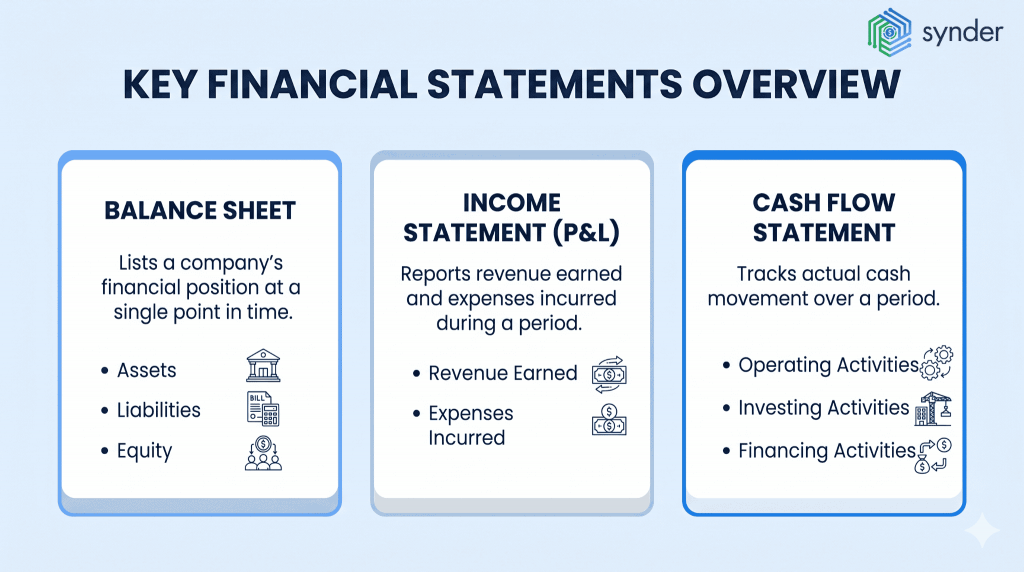

What do the three financial statements actually tell you?

All the recording, categorizing, and adjusting that happens throughout an accounting period leads to one destination: three reports that together describe the financial condition of your business. Each report answers a different question, and each is incomplete without the other two.

The balance sheet captures a single moment in time, typically the last day of a reporting period. It lists assets, liabilities, and equity, and because it’s a direct expression of the accounting equation, it must balance. The balance sheet answers: what does this business own, what does it owe, and what’s left for the owner right now?

The income statement (also called a profit and loss statement, or P&L) covers a span of time: a month, quarter, or year. It reports revenue earned and expenses incurred during that period, with the difference being net profit or loss. Under accrual accounting, this figure reflects economic activity, not cash movement, which means a healthy income statement doesn’t guarantee a healthy bank balance.

The cash flow statement tracks actual cash movement over the same period, broken into three categories: operating activities (running the business), investing activities (buying or selling assets), and financing activities (loans, equity, repayments). Read the three statements together, not in isolation.

How the three financial statements connect

The three statements are interconnected in specific ways. Net income from the income statement flows into retained earnings on the balance sheet. Changes in cash from the cash flow statement show up in the cash line on the balance sheet. If these relationships don’t hold when you look across all three reports, something in the books is wrong. That interdependency is exactly why auditors and lenders review all three together rather than any one in isolation.

For ecommerce and retail businesses, the gap between profit and cash is particularly sharp. A business can show a healthy P&L while cash is tied up in inventory purchased for peak season, or in receivables from wholesale customers on net-60 terms. Understanding that profit doesn’t equal cash flow is what explains why a business can look strong on paper and still run short on cash at the wrong moment.

But the connection runs deeper than most readers realize. As Josh Aharonoff, CPA, founder of Mighty Digits, wrote on LinkedIn:

The Statement of Cash Flows doesn’t actually contain any new information. Everything can be derived from the P&L and Balance Sheet.

Josh Aharonoff, CPA, founder of Mighty Digits

It means that when your three statements stop lining up, the cash flow statement is usually the first place the problem becomes visible, because it tracks how reported income actually connects back to real cash moving through the business.

What most business owners miss in their financial statements

There’s a layer to financial statements that standard accounting guides rarely show, namely how practitioners actually use them and what they reveal beyond the obvious numbers:

- Financial statements are backward-looking. By the time reports are finalized, the data is already weeks old. Many CPAs recommend a flash report, updated weekly or daily, with cash, receivables, year-to-date revenue, and key metrics. Statements show where you have been. The flash report shows where you are.

- The income statement has layers, but most owners focus on net income. Gross profit shows if the core business works. Operating profit includes overhead. The gap between them is where margin erosion hides: headcount, platform costs, and rising fees.

- Most small businesses don’t need an audit, but they often need more than a compilation. CPA involvement ranges from preparation to compilation, review, and audit. A review adds analytical checks and limited assurance, and is often worth it for financing, sales, or complex operations.

- The footnotes explain accounting policies, unusual items, and risks. They include revenue recognition methods, related-party transactions, contingent liabilities, and estimate changes. Most owners skip them, but lenders and acquirers look there first.

The most underused financial tool for small business owners isn’t a statement, but a comparison. Running your income statement against the same period last year, or against a monthly budget, turns a static report into a diagnostic. Without that comparison, strong numbers look fine and weak ones are easy to rationalize. With it, trends become visible: a cost line that’s growing faster than revenue, or a margin that’s been compressing for three quarters.

How does a transaction become a financial statement? The accounting cycle

The accounting cycle is the sequence of steps that transforms a raw business event into a line in a financial statement. It runs continuously during the period for some steps and closes out at period-end for others.

- Identify the transaction. After a sale happens, an expense is incurred, or a loan is received, the first task is recognizing that the event has financial consequences worth recording.

- Prepare a journal entry. Record the transaction: date, description, which accounts are affected, and the corresponding debits and credits.

- Post to the general ledger. The general ledger is the central repository for all account balances. Historically, this was a physical book maintained by hand. Today, it’s the database at the core of any accounting software. Each journal entry updates the relevant account balances here.

- Prepare a trial balance. At period-end, pull every account’s running total into a single report. Debit totals should match credit totals exactly. If they don’t, there’s an error somewhere to track down before proceeding.

- Post adjusting entries. Align the books with accrual accounting: recognize earned revenue that was previously deferred, accrue expenses that have been incurred but not yet paid, record depreciation on fixed assets.

- Prepare an adjusted trial balance. Rebuild the trial balance with adjustments included, confirming that debits and credits still agree.

- Produce financial statements. Generate the income statement, balance sheet, and cash flow statement from the adjusted trial balance.

- Post closing entries. Zero out the temporary accounts (revenue, expenses, dividends), transferring their net balances to retained earnings. The permanent accounts carry forward; the temporary ones reset for the new period.

Together, these steps form a repeating loop: when you close one period, you open the next. Modern accounting software compresses most of this: transactions post automatically from connected platforms, the ledger updates in real time, and statements generate on demand. What software can’t replace is judgment about whether a transaction is categorized correctly, an adjustment is warranted, or the numbers make sense. Walk a single transaction through all eight steps once a quarter to make sure your software is doing what you think it’s doing.

The accounting cycle is also a diagnostic tool. If your financial statements are regularly surprising (profit looks fine but cash is always tight, or tax bills are unexpectedly large), the cycle is where to look. More often than not, the mismatch traces back to steps 4 or 5: a trial balance that wasn’t reviewed carefully, or adjusting entries that were skipped or estimated. The cycle creates a repeatable process for catching errors before they multiply across periods.

When books aren’t right and automation changes that

In practice, ecommerce businesses often arrive at reconciliation time with months of uncategorized transactions, mismatched platform fees, and a growing gap between their accounting software and their bank statements. Audit your reconciliation cadence before you audit your books.

We talk to ecommerce businesses constantly, and reconciliation keeps coming up as the most time-consuming monthly task and the one most likely to go wrong when it’s handled manually across multiple platforms. An Amazon seller handling 15,000 transactions per month who’s manually categorizing FBA storage fees, referral fees, and reimbursements is doing work that doesn’t scale and generates errors that pile up over time.

Accounting automation addresses the cycle at steps 2 through 4 (journal entries, ledger posting, and trial balance preparation) by connecting sales platforms and payment processors directly to accounting software. Transactions sync automatically, categorized according to rules defined upfront, so that when month-end arrives, the data is already structured and ready for review rather than waiting to be entered.

Synder, for example, is an accounting automation tool that helps businesses sync their ecommerce and financial data across 30+ platforms. It connects to QuickBooks, Xero, NetSuite, Sage Intacct, and Puzzle on the accounting side, and to Stripe, PayPal, Shopify, Amazon, and similar sources on the data side. Every sale, fee, refund, and payout is recorded as a properly structured journal entry, categorized according to rules the business sets once. For a multichannel ecommerce business closing the books each month, that means steps 2 through 4 of the accounting cycle run largely on their own.

Healthy Meals Direct, a Long Island meal prep business selling across 30+ locations through Shopify and PayPal, was losing three to four hours every single day to manual reconciliation before automating the workflow. With 100,000+ transactions running through their books and store-level sales tax breakouts required under New York’s Prompt Tax system, the manual process couldn’t keep up. After automating with Synder, their daily reconciliation dropped.

We’re saving real time with Synder. Instead of 3 or 4 hours, I now dedicate around 30–45 minutes to the task of reconciling transactions and making sure everything is perfect in our books. That’s over 70 hours saved each month, which I can now dedicate to more strategic parts of my role.

Victoria Martinez, Customer Service Manager at Healthy Meals Direct

The accuracy improvement mattered as much as the time savings. Fewer errors at the data-entry stage means fewer corrections needed later, and month-end closes that don’t require excavation.

| If your business processes transactions across more than one platform and reconciliation is still a manual effort, book a demo with Synder to see how the setup works for your stack. |

Accounting basics: what to remember and what to do next

Accounting isn’t reserved just for accountants. The major concepts (the accounting equation, double-entry bookkeeping, the six account types, accrual vs. cash, the three financial statements, the principles behind GAAP and IFRS, and the accounting cycle) form a system any business owner can learn to handle. You don’t need to post journal entries yourself, but understanding what your bookkeeper is doing and what your financial statements are showing changes the quality of decisions you make.

The accounting equation always stays balanced, but each report shows a different side of the business. Your income statement reflects profit, not cash, your cash flow statement shows how cash actually moves, and your balance sheet ties the two together at a specific point in time, giving you a clear view of where the business stands. Build the muscle to read your statements before you outsource the discipline of preparing them.

FAQ

When should a business switch from cash to accrual accounting?

Switch the moment you take on inventory, sell subscriptions or pre-paid plans, extend customer payment terms, or start preparing financials for a lender, investor, or buyer. Waiting until an outside party requires it usually means restating prior periods and filing IRS Form 3115 under pressure.

What’s the difference between bookkeeping and accounting?

Bookkeeping is the data-capture layer: recording transactions, reconciling accounts, and keeping the ledger current. Accounting is the interpretation layer: adjusting entries, producing financial statements, and applying GAAP or IFRS. Bookkeepers maintain the records; accountants and CPAs analyze them and sign off on what they show.

Do I have to follow GAAP if I’m a private company?

US private companies aren’t legally required to follow GAAP, but most do when they prepare financials for lenders, investors, or potential acquirers. Loan covenants and investor agreements almost always require GAAP-basis statements. Tax filings follow IRS rules, which differ from GAAP in several areas.

What are the seven pillars of accounting?

The seven pillars vary by framework, but typically include accuracy, consistency, reliability, relevance, comparability, timeliness, and understandability. They describe the qualities a financial statement must have to be useful to investors, lenders, and the business owners themselves.

Do I need an accountant if I use accounting software?

Software automates data entry and statement generation, but it can’t make judgment calls on categorization, accrual adjustments, tax planning, or compliance. Most growing businesses benefit from working with a bookkeeper for day-to-day records and a CPA for period-end review, tax strategy, and financial analysis.y-to-day records and a CPA for period-end review, tax strategy, and financial analysis.

Good

Hi Anastasia. Thank you for the article. It is really useful for fresh student learning accounts.

Thank you for your feedback! Ensuring our content is both educational and useful to our audience is our top priority.

This is a straightforward and crispy method of understanding the subject. It is beneficial and gives confidence too.

Thanks to you

Your blog is comprehensive and well-written, as it addresses almost every facet of the skills that will be in high demand.

Thanks for the article! Was great to learn about the accounting principles.

Anastasia Su’s article on basic accounting principles is super helpful! It breaks down complex concepts into easy-to-understand info, perfect for beginners or pros. I love the “Fantastic Four” steps, making accounting feel less daunting. The detailed explanation of principles like “Revenue Recognition and Conservatism is spot-on.” The article also dives into the importance of accounting software, like Snyder Sync, which is a game-changer. Overall, it’s a must-read for anyone wanting to understand and ace the accounting game!