Have you ever heard of ACH credits or want to learn more about them? Read on! In our guide, we will simplify the financial jargon behind ACH credits and explain what they are, how they differ from other payment methods, and why they could be a good fit for some of your business operations.

Ready to revolutionize the way you handle business transactions? Discover the ease and efficiency of Synder. Say goodbye to manual processing and embrace a world of automated, error-free bookkeeping!

What are ACH payments or transactions?

Automated Clearing House (ACH) transactions are a way to move money electronically between banks in the United States. It’s like an invisible highway for money, allowing funds to travel from one bank account to another. This system is used for all sorts of payments – from your paycheck landing in your bank account to paying bills online, or even when businesses pay each other.

What is an ACH credit?

An ACH credit is a type of ACH transaction where money is deposited into a recipient’s bank account. Think of an ACH credit like sending an email. You’re the one initiating, “pushing” the message (or in this case, money) out to someone else. When you use an ACH credit, you’re telling your bank to transfer money from your account into someone else’s account.

For business owners, this is a key tool. Whether you’re paying employees through direct deposit or sending money to a supplier, ACH credits make these transactions smooth and easy.

What’s the difference between ACH credits and ACH debits?

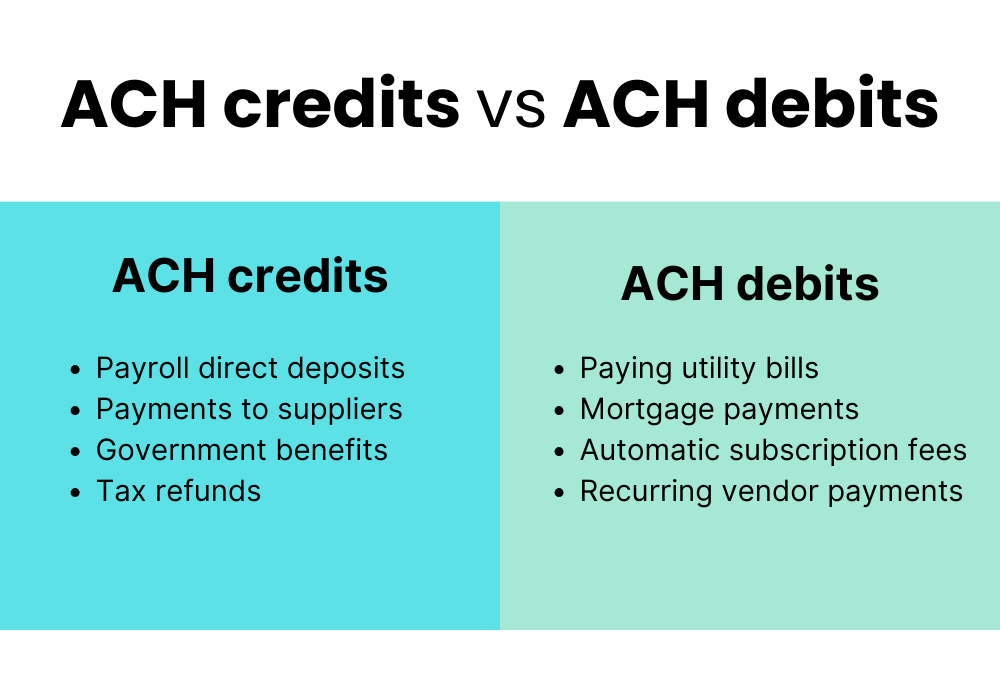

When you use ACH, the transactions can either be debits or credits. An ACH debit pulls money from an account (like when you pay a bill online and the money is taken out of your account). You’re not doing the sending; instead, you’re allowing someone else to “pull” money from your account. On the other hand, an ACH credit pushes money into an account, which is what we’re focusing on in this article.

The common scenario for ACH debits would be paying utility bills where the utility company takes the bill amount from your account each month. If, as a business owner, you offer subscription services, you might pull the subscription fee from your customers’ accounts regularly.

What is an ACH credit refund (ACH return)?

An ACH credit refund, often referred to as an ACH return, is a situation that business owners might encounter when dealing with electronic payments.

Imagine you’ve sent money via an ACH credit – maybe you’ve paid a vendor, an employee, or a customer refund. An ACH return happens when the money you sent is sent back to you. This is like a boomerang effect with electronic payments.

Why does an ACH return happen?

There are a few reasons why the money you sent might come back to you:

- Incorrect account information: Maybe you entered the wrong bank account number or routing number. Just like sending a letter to the wrong address, it comes back to the sender.

- Closed or invalid account: If the recipient’s bank account is closed or invalid, the bank can’t deposit the money, so it returns it to you.

- Insufficient funds: If the recipient’s account can’t cover a transaction, like in the case of an ACH debit, the transaction might be reversed.

- Authorization issues: If there’s a dispute over authorization, for example, if someone claims they didn’t give permission for the debit, the transaction might be reversed.

- Duplicate transactions: Accidentally sending the same payment twice can result in one being returned.

When you get an ACH return, check the reason provided by the bank. It’s usually a specific code that tells you what went wrong. Once you’ve figured out the issue, you can resend the payment with the correct details or after resolving the issue.

Remember to document these incidents for your financial records. It helps in understanding your cash flow and in keeping accurate records.

How ACH credit payments work

Understanding how ACH credit payments work can seem a bit complex at first, but it’s actually quite straightforward once you break it down. But first, let’s simplify the financial jargon used when talking about ACH transactions.

ACH credit: Common terms

Originator (You, the business owner)

You’re the one initiating the transaction, instructing your bank to transfer funds from your account to another account.

Originating Depository Financial Institution (ODFI)

This is your bank or other processing partner. They take your payment instructions, validate them, and then forward them to the ACH network.

ACH network

The central processing system that routes your payment instructions to the correct recipient’s bank.

Receiving Depository Financial Institution (RDFI)

This is the recipient’s bank. They receive the payment instructions from the ACH network, verify it, and credit the recipient’s account with the payment amount.

Beneficiary (Recipient)

The person or entity receiving the funds. In the case of payroll, it’s your employee; for vendor payments, it’s the supplier you’re paying.

Now that we’ve explained the common terms used in ACH payments, we will take a look at how ACH credit transactions work.

1. Initiation of the transaction

It all starts when you, as a business owner, decide to make a payment via ACH credit. You submit a payment order to your bank. This usually involves logging into your online banking platform and entering details like the amount of the payment, the recipient’s bank account information, and the date you want the payment to be processed.

2. Your bank processes the order

Your bank (or other processing partner), known as ODFI, receives your order and prepares to send the funds. They’ll check your account to ensure you have enough funds to cover the payment.

3. Transaction is sent through the ACH network

The ODFI sends the payment instructions through the ACH network. This network acts like a central hub, sorting and directing these payment instructions to the correct destination.

4. The receiving bank gets the instruction

The payment instruction arrives at the recipient’s bank i.e. RDFI. This bank checks the details and prepares to credit the recipient’s account.

5. Funds are credited to the recipient’s account

Finally, the recipient’s account is credited with the payment amount. This step typically happens on the date you specified when you initiated the transaction.

Benefits of ACH credits for business owners

We’ve seen how ACH credits work. Let’s now break down their key benefits.

Cost-effectiveness compared to other payment methods

One of the biggest advantages of ACH credit is its cost-effectiveness. Typically, ACH transactions have lower fees compared to methods like wire transfers or credit card processing. This means you spend less money moving your money.

If you’re paying multiple employees or vendors, ACH allows you to handle all these transactions in one batch. This bulk processing capability not only saves time but also reduces the costs associated with individual transaction fees.

By using ACH credit, you eliminate the need for writing, mailing, and processing paper checks. This reduces costs associated with check stock, printing, and postage.

Speed and efficiency of transactions

ACH credit transactions are processed quicker than traditional checks. This means your employees get paid faster, and vendors receive their payments more promptly, enhancing your business relationships.

What’s more, you can schedule ACH payments in advance. This is particularly useful for regular expenses like payroll, where you can set up the entire process ahead of time, allowing for smoother cash flow management.

Safety and security aspects

ACH transactions are more secure than checks, which can be lost, stolen, or altered. With electronic transactions, there’s a lower risk of fraud. Every ACH transaction is traceable, providing a clear audit trail. This helps in monitoring and reconciling your business’s financial transactions.

In an ACH transaction, sensitive banking information is transmitted securely and is less exposed compared to paper checks, which pass through multiple hands.

Common uses of ACH credits for business owners

Let’s explore how ACH credit can be utilized in everyday business operations.

Payroll direct deposits

As already mentioned, one of the most common and valued uses of ACH credit is for payroll. Instead of cutting individual checks for each employee, you can simply transfer their salaries directly into their bank accounts. With ACH, you can easily keep tabs on payroll disbursements without drowning in paperwork.

Want the dive into the world of payroll? Read this detailed guide to forms in payroll for busy entrepreneurs.

Government benefits

If your business is entitled to any government benefits, such as tax incentives or grants, these are often disbursed via ACH credit. It’s a secure and direct way to receive funds owed to you by government agencies.

The direct nature of ACH credit ensures that you receive these payments swiftly and directly into your business account, without the need for manual depositing of checks.

Vendor payments

ACH credit is also extensively used for paying vendors or contractors. This method is especially handy for recurring payments, like regular supply orders or contracted services.

Timely and hassle-free payments can help in maintaining good relationships with your suppliers and contractors, which is crucial for business continuity and reputation.

Tax refunds

In instances where your business is due for a tax refund, the IRS and many state tax authorities use ACH credit to process these refunds. This means you get your money back faster compared to traditional checks.

Electronic refunds via ACH credit reduce the chance of errors that can occur with paper checks, such as misplacement or postal delays, ensuring that your business’s finances are not disrupted.

Comparing ACH credit to other payment methods for business owners

We will now compare ACH credit with other common payment methods: wire transfers and paper checks, focusing on aspects that matter most to you as a business owner.

ACH credit vs wire transfers

- Cost: ACH credit often comes out on top in terms of cost. Wire transfers can be pricey, especially for international transactions. ACH transfers typically have lower fees, making them more cost-effective for routine transactions.

- Speed: Wire transfers are faster, usually settling on the same day, which is great for urgent payments. ACH credits, on the other hand, might take a day or two but are improving with the advent of same-day ACH processing.

- Security and suitability: Both methods are secure, but wire transfers are often used for high-value or time-sensitive transactions due to their immediacy. ACH is more suited for regular and recurring transactions.

ACH credit vs paper checks

- Efficiency and convenience: ACH credit is far more efficient than paper checks. There’s no need to write, mail, or manually deposit checks, saving you significant time and hassle.

- Cost and environmental impact: ACH payments reduce costs related to check printing, postage, and processing. They’re also more environmentally friendly, cutting down on paper usage.

- Risk and security: Paper checks carry risks like theft, loss, or fraud. ACH transactions are more secure, with encrypted data and fewer hands handling each transaction.

Conclusion

And there you have it! A straightforward run-through of ACH credits. From understanding the basics of what an ACH payment is to deciphering the difference between ACH credits and debits, and even tackling those occasional ACH returns, we’ve covered the essentials that you need to know.

The world of business payments doesn’t have to be complicated, and with ACH credits, you’re looking at a secure, cost-effective, and efficient way to handle your business’s money matters.

Embracing this tool can be a significant step in modernizing and optimizing your business operations. So, go ahead and take full advantage of what ACH credits have to offer – your business’s financial health will thank you for it!

Want to explore payroll options? Read our guide about outsourced payroll.