Inventory is usually the largest asset on a retailer’s balance sheet, accounting for up to 80% of total assets for small retailers, according to NetSuite’s CPA-authored analysis. The method you use to value that inventory shapes your gross margin, tax liability, cash flow decisions, and what lenders or acquirers see when they evaluate your business.

Retail accounting is a specific approach to that valuation challenge. It lets merchants estimate ending inventory using selling prices rather than painstakingly tracking what every item cost to acquire. For a clothing chain with fifty store locations, that distinction is the difference between completing a monthly close in a day or closing an entire store network to count socks and T-shirts. But the method has real limits – and choosing the wrong one, or applying it incorrectly across channels, causes the kind of invisible financial drag that only shows up when it’s already expensive to fix.

TL;DR

- Retail accounting is an estimation method: It uses a cost-to-retail ratio to approximate inventory value instead of tracking actual item costs, making it faster but less precise.

- It works best under stable conditions: The method is reliable when margins are consistent, pricing is predictable, and operations are relatively simple.

- It breaks in complex, multi-channel setups: Selling across platforms, running promotions, or having mixed margins introduces distortions in COGS, inventory, and profit.

- Financial statements can be misleading: Inaccurate ratios or outdated data can overstate inventory, understate costs, and inflate reported margins and tax liabilities.

- Data quality matters more than the method: Clean, detailed, and automated transaction data is the foundation; without it, any inventory method produces unreliable results.

What is retail accounting?

Most accounting guides describe retail accounting by what it does: estimate inventory without a physical count. That’s true, but it understates the decision you’re making. Retail accounting is, at its core, an averaging technique: it collapses all the individual unit costs in your inventory pool into a single ratio, then uses that ratio to translate your selling-price-denominated records into a cost-denominated balance.

Where it stands legally and under GAAP

The method has been recognized under U.S. Generally Accepted Accounting Principles (GAAP), specifically ASC 330, Inventory, for decades. The IRS accepts it for tax purposes. It’s also available under International Financial Reporting Standards (IFRS), making it applicable across jurisdictions for businesses with international operations. PwC’s accounting guide describes it as an averaging technique “used by retailers to reduce the amount of recordkeeping associated with accounting for inventories,” which is about as honest a one-sentence summary as you’ll find.

Retail accounting vs cost accounting

The difference between retail accounting and cost accounting, which is the question retailers ask most frequently, comes down to what data anchors your valuation. Retail accounting works from selling prices and applies a ratio to estimate costs. Cost accounting tracks actual purchase prices for each item or SKU. Both are GAAP-accepted. Cost accounting is more precise; retail accounting is faster to operate at scale.

Within cost accounting, retailers typically choose between three methods:

- FIFO (first-in, first-out) – values inventory using the oldest purchase costs first; produces lower COGS and higher ending inventory in periods of rising costs

- LIFO (last-in, first-out) – uses the most recent purchase costs first; only permitted under U.S. GAAP, not IFRS

- Weighted average cost – divides total inventory cost by total units to smooth out price fluctuations across a period

Each produces different COGS and ending inventory figures, with direct tax and margin implications. They’re covered in more detail in the FAQ below.

Read more about retail accounting vs cost accounting.

| What retail accounting can’t do: it’s not a cost-tracking method, it is not a substitute for physical counts, and it’s not well-suited to businesses with wildly different markups across product categories. These distinctions matter more as businesses scale. |

How the retail inventory method works

The retail inventory method operates through a cost-to-retail ratio, sometimes called the cost complement percentage, calculated once per period and applied to your ending inventory balance at retail prices to produce an estimated cost.

The formula for ending inventory under the retail method is:

Ending inventory cost = (Cost of goods available for sale ÷ Retail value of goods available for sale) × Ending inventory at retail

Breaking that down into steps:

- Calculate cost of goods available for sale by adding beginning inventory at cost to purchases at cost during the period.

- Calculate the retail value of goods available for sale by adding beginning inventory at retail to purchases at retail, then adjusting for net markups (add) and net markdowns (subtract, but only in the average cost variant).

- Divide cost by retail to get the cost-to-retail ratio.

- Subtract net sales from the retail value of goods available for sale to get ending inventory at retail.

- Multiply ending inventory at retail by the cost-to-retail ratio to convert it to an estimated cost.

Here’s a worked example. A specialty outdoor gear retailer begins Q3 with $60,000 in inventory at cost, which carries a retail value of $100,000. During the quarter, the retailer purchases $40,000 of additional merchandise (cost), with a retail value of $80,000. Net sales for the quarter total $90,000.

- Cost of goods available: $60,000 + $40,000 = $100,000

- Retail value of goods available: $100,000 + $80,000 = $180,000

- Cost-to-retail ratio: $100,000 ÷ $180,000 = 55.6%

- Ending inventory at retail: $180,000 − $90,000 = $90,000

- Ending inventory at cost: $90,000 × 55.6% = $50,040

The retailer reports $50,040 as ending inventory on the balance sheet and derives COGS by subtracting that figure from the $100,000 of goods available for sale: $49,960.

Perpetual vs periodic inventory: the system behind the method

The retail inventory method can run on two different inventory tracking systems, and the distinction is often more operationally consequential than the valuation method itself.

Perpetual inventory system

The perpetual inventory system updates stock records continuously after every purchase, sale, return, or adjustment. Point-of-sale systems connected to accounting software are the most common implementation: a transaction at the register or a fulfilled online order immediately adjusts the inventory ledger.

The upside is real-time visibility into stock levels and current-period COGS at any moment.

The downside is implementation cost and the ongoing need for clean data flows between sales channels, warehouses, and accounting systems.

Periodic inventory system

The periodic inventory system only updates inventory records at set intervals, typically at month-end or year-end, through a physical count. COGS is calculated as a residual:

COGS = Beginning inventory + Purchases – Ending inventory

It’s simpler to implement and less technically demanding, but it means operating without current-period financial visibility between counts. A retailer on a periodic system genuinely can’t know their gross margin for the month until the count is complete.

The practical question for most retail businesses is which their transaction volume and channel complexity demands. A single-location specialty retailer with 200 SKUs can reasonably operate on a periodic basis with quarterly counts. A multi-location retailer processing 8,000 transactions per month across Shopify, Amazon, and a brick-and-mortar location needs real-time inventory data to manage reorders, fulfillment, and cash flow, where the periodic approach creates dangerous blind spots.

You need to be aware that the transition from periodic to perpetual is often triggered by a specific breaking point. One Canadian ecommerce retailer selling sleep apnea products both online through Shopify and through a physical retail location, reached that point when product additions required manual duplication across both Shopify and QuickBooks twice for every SKU, because each channel operated under different government guidelines and created duplicate records. The manual overhead was a source of persistent reconciliation errors and inaccurate reporting across channels.

After automating the sync between Shopify, QuickBooks, and PayPal, the team saved 2–3 hours per week on data entry alone and eliminated the duplicate SKU problem that had been ruining their financial picture entirely.

Where the retail method breaks down and what to do about it

The retail method’s core assumption is that the cost-to-retail ratio is consistent across your inventory. That assumption breaks in several common scenarios.

Multi-channel environment

The retail inventory method was developed for large physical retailers who had excellent records of what they bought and sold but couldn’t practically track individual unit costs across thousands of SKUs. That operational context has changed a lot. A retailer operating Shopify, Amazon, and a physical location with Square POS has three separate systems generating transaction data in three different formats, with fees, returns, chargebacks, and currency conversions complicating every reconciliation.

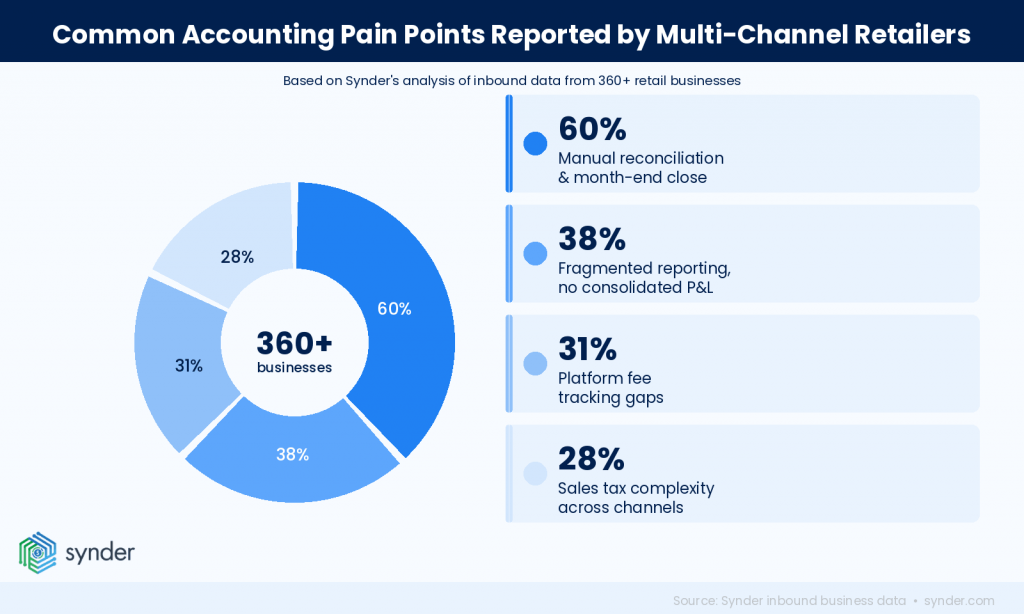

Based on Synder’s analysis of inbound business data, the most common accounting pain points reported by multi-channel retailers include:

The first two of those pain points interact directly with inventory valuation. If you can’t see what Amazon charged you in fees for a given period, your actual landed cost per unit is wrong. If your sales tax categorization is incorrect, your net revenue, and therefore your cost-to-retail calculation, is incorrect. The retail method, applied to bad inputs, produces bad outputs with a misleading veneer of mathematical precision.

This is where the operational architecture matters as much as the accounting method chosen. A retailer on a perpetual system with automated data sync across channels is working from clean, current data regardless of which valuation method they apply. A retailer on a periodic system, manually reconciling three platforms at month-end, is making valuation decisions based on data that may already be 30 days stale and contain undetected errors.

A multi-channel ecommerce company selling through Shopify, Amazon, Stripe, and wholesale, had a similar issue as it expanded. Their CFO was managing all financial operations independently but had no reliable transaction-level detail flowing into QuickBooks: monthly journal entries lacked the granularity needed for meaningful cost analysis or accurate margin reporting. After implementing automated individual transaction sync mode across all four channels, they achieved sub-0.5% variance in monthly reconciliation and reduced what was previously a multi-person accounting function to a single CFO role. The $60,000+ annual staffing savings were secondary to what the CFO described as the ability to “immediately analyze performance” – the operational precondition for making any inventory valuation method actually reliable.

| Business tip: If you’re a retail business selling across multiple channels, the data hygiene problem is usually the first thing worth fixing before revisiting your valuation method. With Synder, you can automatically sync transactions from Shopify, Amazon, Square, Stripe, PayPal, and 30+ other platforms into QuickBooks Online, Xero, Sage Intacct, NetSuite, and Puzzle with fees, taxes, and refunds categorized separately per channel. That gives your cost-to-retail ratio, or any cost-based calculation, clean, current inputs to work from. You can test it on your own data with a free trial before committing to anything. |

Mixed-margin product assortments

The retail method produces one cost-to-retail ratio for your entire inventory pool, which works when your margins are consistent, and breaks down when they’re not. A home goods retailer selling decorative candles at 70% gross margin alongside commodity cleaning supplies at 18% will see the blended ratio shift whichever way sales volume tilts that quarter, understating inventory cost on the high-margin lines in one period and overstating it in the next. Neither direction is benign – both distort COGS and gross margin for that period.

Average inventory accuracy across retail businesses runs at approximately 83%, with physical retail stores averaging closer to 65%. Applying a single blended ratio on top of already-imperfect base data produces valuations with layered error. The fix is to calculate separate cost-to-retail ratios by product category, treating each as its own pool. And it’s the only way the method produces figures that hold up to scrutiny when assortments are mixed.

The markdown problem

What the top search results on this topic often skip over is how the retail method handles price reductions. When a retailer marks down merchandise, for instance cutting a $50 item to $35 for a clearance event, the selling price drops, but the cost to acquire that item hasn’t changed. That gap matters because the cost-to-retail ratio is built from selling prices.

A markdown compresses the ratio: the same item that cost $25 and once carried a 50% cost-to-retail ratio now carries a 71% ratio at the marked-down price. If that markdown isn’t captured in the calculation, the ratio understates cost, and ending inventory ends up valued higher than it should be.

The retail method excludes markdowns from the cost-to-retail ratio by design. That’s a known limitation, not an oversight. Excluding markdowns keeps the ratio stable and conservative – ending inventory is valued lower, which avoids overstating assets on the balance sheet. But it also means the ratio no longer reflects what inventory actually cost on average after a significant price reduction.

| Note: In a quarter with heavy promotional activity, that gap can produce a materially understated COGS and an overstated gross margin – numbers that look better than the business actually performed. It’s one of the clearest signals that a retailer running frequent promotions may get more accurate financials from cost-based tracking than from the retail method, and therefore meaningfully different gross margin numbers on your income statement. |

Shrinkage

The retail method has no mechanism for tracking inventory that disappears before it can be sold, and the scale of that omission matters. U.S. retail shrinkage consistently runs at around 1.6% of total retail sales according to NRF data, with theft accounting for roughly 65% of losses and administrative errors and damage making up the rest. On a $2 million inventory, that’s approximately $32,000 per year that will never appear in the retail method’s calculations.

What makes this a specific problem for the retail method is the timing. Shrinkage never appears in COGS during the period it occurs, only at the physical count. For a business doing annual counts, a year’s worth of losses lands as a single write-down that inflates COGS in the count period rather than distributing the expense across the periods when it actually happened. That distorts both the periods in between (overstated inventory, understated COGS) and the count period itself. A shrinkage reserve or regular cycle counting programme running alongside the retail method is the practical safeguard. Without it, the method produces clean-looking numbers that drift from reality between counts.

Sales tax across channels

Sales tax is where the retail method’s data quality problem becomes a compliance problem. For a multi-channel retailer selling through Shopify, Amazon, and a physical location, the tax collected on any given transaction isn’t revenue – it’s a liability owed to the state where the sale occurred. If it flows into your gross revenue figure uncategorized, your cost-to-retail ratio is built on inflated numbers from the start.

The complexity compounds quickly. Since the Supreme Court’s 2018 South Dakota v. Wayfair ruling, states can require sellers to collect sales tax based on economic nexus, meaning once you cross a state’s revenue or transaction threshold, you’re obligated to collect and remit there, even without a physical presence. Most states set that threshold at $100,000 in sales or 200 transactions annually. A retailer growing across Shopify and Amazon can cross nexus thresholds in multiple states without realizing it until they’re already out of compliance.

Each platform handles tax collection differently, which is the operational problem. Amazon collects and remits sales tax on marketplace sales in most states through Marketplace Facilitator laws, so that tax never touches your books. Shopify sales, by contrast, are your responsibility to collect and remit, and the tax collected shows up in your Shopify payout alongside revenue. If your accounting system isn’t separating those amounts at the transaction level, you’re either overstating revenue or underpaying tax, sometimes both in the same period.

The retail method has no built-in mechanism for this. It assumes clean revenue figures going in, and sales tax contamination is one of the most consistent ways that assumption fails in practice. The fix is upstream: automated transaction sync that categorizes sales tax separately per channel, per state, before any inventory calculation runs. Without it, every cost-to-retail ratio you calculate is working from a revenue figure that may include tax dollars you don’t own.

What retail accounting means for your financial statements

The choice of inventory valuation method isn’t an accounting technicality tucked away in a spreadsheet. It flows through to the three financial statements that owners, CFOs, and lenders actually use to make decisions.

Income (P&L) statement

On the income statement, the retail method determines COGS indirectly:

- It estimates ending inventory first.

- It derives COGS as the residual.

The accuracy of that COGS figure depends entirely on how well the cost-to-retail ratio reflects actual margins during the period. When markups are stable, the estimate is reliable. When margins shift due to promotions, clearance, or channel mix changes, the estimate drifts, and that divergence widens if the ratio isn’t recalculated to reflect what actually happened.

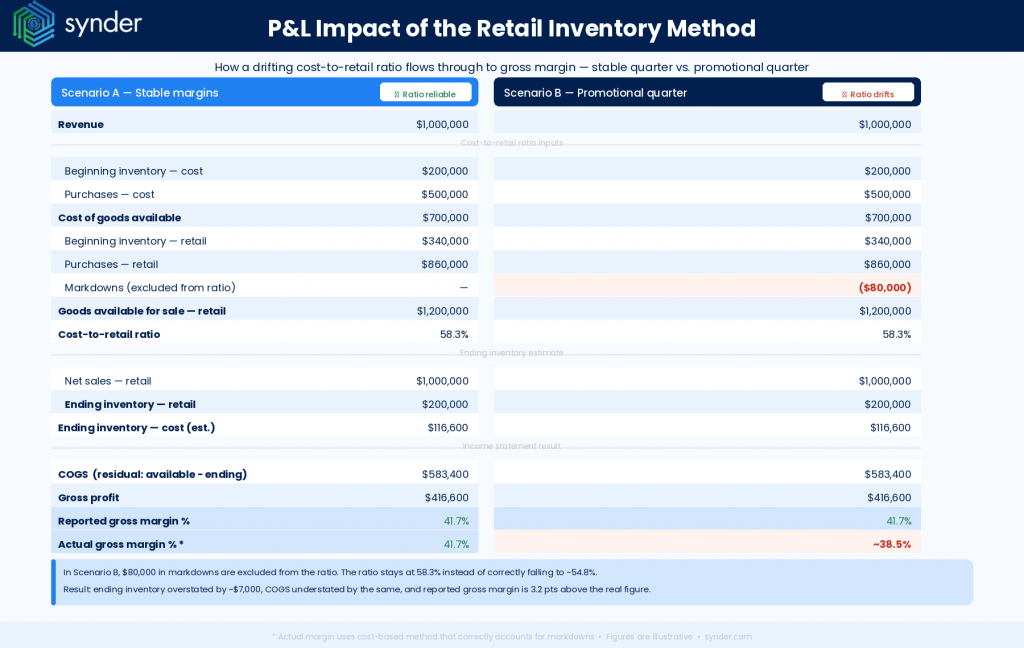

To make this concrete: consider a retailer with $700,000 in goods available at cost and $1,200,000 at retail – a cost-to-retail ratio of 58.3%. In a stable quarter with $1,000,000 in net sales, ending inventory estimates out at $116,600 at cost, COGS lands at $583,400, and gross margin is 41.7%.

Now run the same quarter with $80,000 in markdowns that the method excludes from the ratio. The ratio stays at 58.3% instead of falling to ~54.8%, ending inventory is overstated by ~$7,000, COGS is understated by the same amount, and the reported gross margin reads 41.7%, while the actual margin, correctly calculated, is closer to 38.5%. The books look fine, but the margin gap doesn’t.

Balance sheet

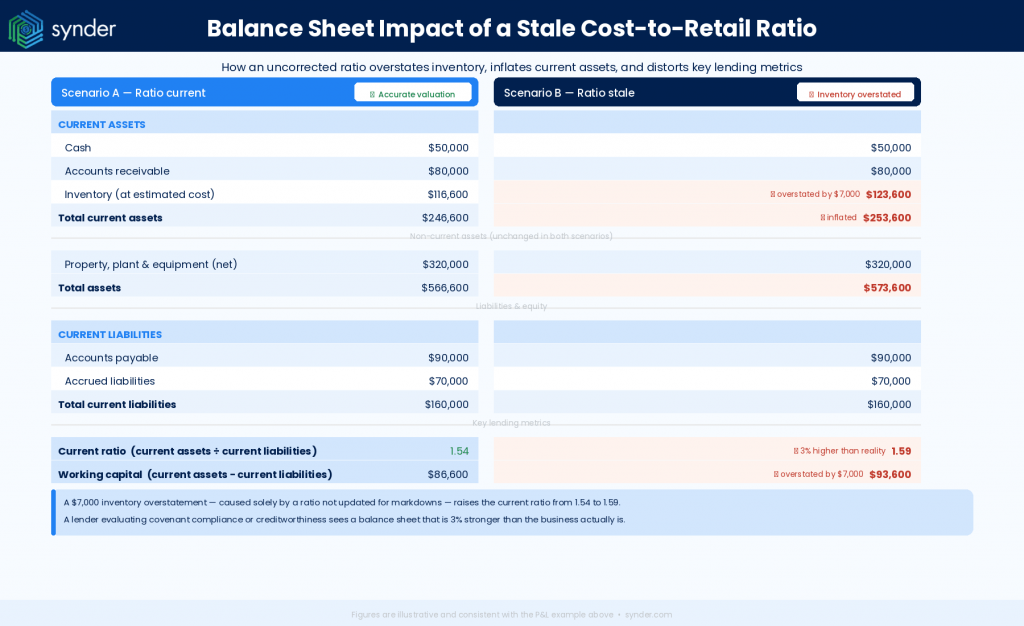

On the balance sheet, ending inventory appears as a current asset valued at estimated cost. Lenders evaluating your current ratio or working capital position are looking at this number directly. If the cost-to-retail ratio is stale or miscalculated, the inventory balance on your balance sheet may be materially wrong, which matters when you’re seeking financing or presenting financials to investors.

Again, the numbers make this tangible. Take a retailer with $116,600 in correctly valued ending inventory, $80,000 in accounts receivable, and $50,000 cash – total current assets of $246,600 against $160,000 in current liabilities. Current ratio: 1.54, working capital: $86,600. Now apply a stale cost-to-retail ratio that overstates inventory by $7,000: current assets become $253,600, the current ratio rises to 1.59, and working capital reads $93,600.

A lender evaluating covenant compliance or creditworthiness is looking at a current ratio that is 3% higher than the underlying business justifies, and the overstatement traces entirely to a ratio that was never updated for markdowns.

Cash flow statement

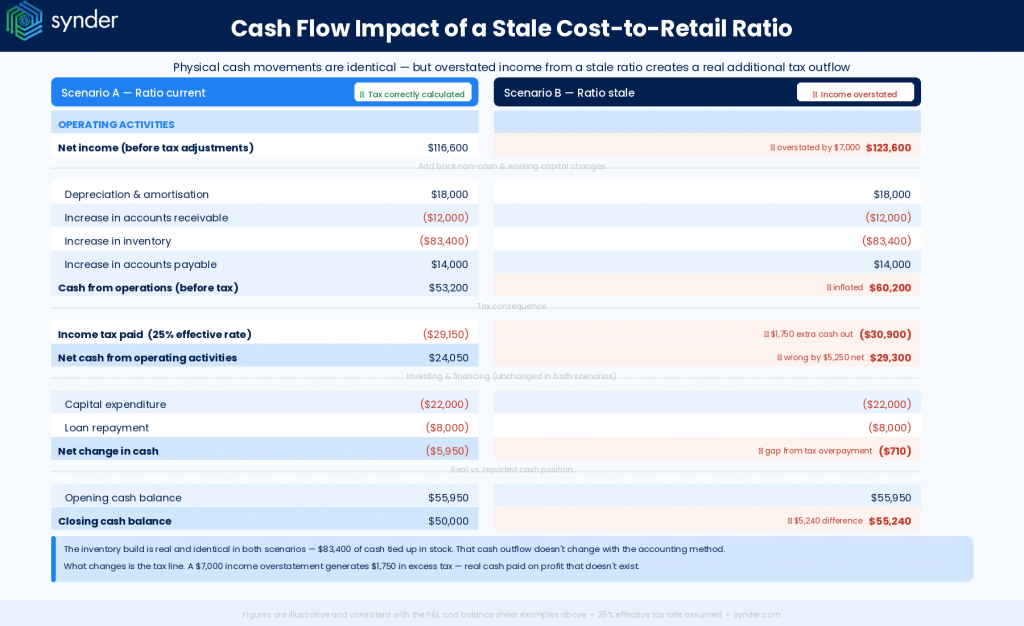

On the cash flow statement, inventory changes appear in operating activities. If ending inventory increases, it represents cash tied up in stock – a use of cash that reduces operating cash flow regardless of how you value it. The retail method doesn’t change the physical cash position, but it changes how your accounting reflects it and, by extension, what tax payment you’ll owe on the resulting income.

Continuing the same example: both scenarios start with identical operating cash: $416,600 gross profit less $300,000 in operating expenses gives $116,600 in pre-tax income under the correct ratio. The stale ratio reports $123,600 in pre-tax income instead, because COGS was understated by $7,000. At a 25% effective tax rate, that difference costs an additional $1,750 in tax – real cash out the door, not an accounting adjustment.

The inventory build itself ($83,400 increase over the period) reduces operating cash flow by the same amount in both scenarios, because the physical stock movement is identical. What differs is purely the tax line.

| Note: The tax dimension deserves its own note. Switching away from the retail inventory method to a cost-based approach requires IRS approval in the United States, must be applied consistently going forward, and needs to be disclosed in financial statements for the year of transition. The resulting inventory valuation adjustment can be spread over multiple years under specific circumstances, but the tax impact needs to be modeled before filing. Consulting a CPA before making any method change is not optional. |

Is the retail method right for your business?

The retail inventory method makes sense under a specific set of conditions. When those conditions aren’t met, it introduces more inaccuracy than it saves time.

The retail method works well when:

- Your product assortment has relatively stable, consistent markups across categories

- You operate at a scale where physical counts every period aren’t practical (multiple locations, high SKU counts)

- You need a fast estimate for interim reporting between full physical counts

- Your business is primarily brick-and-mortar with a consistent pricing structure

The retail method is less appropriate when:

- You sell across multiple channels at materially different price points

- Your margins vary significantly by product category (e.g., mixing accessories at 70% gross margin with commodity items at 15%)

- You run frequent promotions that change actual realized margins

- You need precise unit-level cost data for pricing decisions or vendor negotiations

- You’re a growing ecommerce business where modern platform integrations make per-item cost tracking operationally feasible

The last point deserves emphasis. The convenience argument for the retail method was strongest when the alternative was manual cost tracking. For a Shopify-first retailer whose accounting software receives an automated feed of every transaction including unit cost from the supplier invoice, the retail method offers no operational advantage, and it introduces estimation error that cost-based tracking would avoid entirely.

Bringing it together: retail accounting conclusions

Retail accounting is a chain of decisions that each affect accuracy, tax position, and operational clarity. Choosing the retail inventory method because it’s fast is rational for a large physical retailer with stable margins. Choosing it for a multi-channel ecommerce business with variable pricing across platforms is a source of ongoing inaccuracy that accumulates over time.

The cost-to-retail ratio is a powerful tool when the conditions for its use are met: consistent markup rates, limited markdown activity, and channels that price merchandise similarly. Outside those conditions, the ratio becomes a liability, which looks precise in the financial statements but reflects assumptions that no longer match reality.

But the valuation method you choose is only as good as the transaction data feeding it. Clean, automated, channel-level data flowing into your accounting system in real time gives every method a reliable foundation. Manual, delayed, or aggregated data undermines every method, regardless of how technically correct the formula is.

FAQ

What’s the difference between retail accounting and cost accounting for inventory?

Retail accounting estimates inventory value using a cost-to-retail ratio calculated from selling prices without unit-level cost tracking. Cost accounting tracks the actual purchase price of each item or SKU. Retail accounting is faster to operate at scale; cost accounting produces more precise financial statements and is better suited to multi-channel or variable-margin businesses.

Can you switch from the retail inventory method to FIFO or another cost-based method?

Yes, but a switch requires IRS approval in the United States and must be applied consistently going forward. The change must be disclosed in financial statements for the year of transition. If the switch has significant tax implications, particularly moving out of LIFO, the taxable income impact needs to be modeled before filing. Working with a CPA to manage the transition is advisable.

Does the retail inventory method account for shrinkage?

No. The retail method does not include a mechanism for tracking shrinkage from theft, damage, or administrative error. Shrinkage is only captured at physical counts, when the actual stock on hand is compared to the book balance. Businesses relying solely on the retail method between counts will systematically overstate inventory values, with the correction appearing as a large adjustment at count time.

Is the retail inventory method acceptable under IFRS for international retailers?

Yes. The retail inventory method is available under IFRS as well as U.S. GAAP, making it applicable for retailers with international operations or those reporting under IFRS in non-U.S. jurisdictions. However, IFRS doesn’t permit LIFO, so retailers switching from LIFO in a GAAP context to IFRS will need to restate inventory under an acceptable alternative method.

What do the 5 P’s of retail have to do with accounting?

Each one affects the cost-to-retail ratio. Product mix determines whether a single ratio is meaningful. Price changes and markdowns shift the ratio in real time. Place (channels) introduces variable pricing a single ratio can’t represent. Promotion compresses margins the retail method only partially captures. People (the accounting team) determines how quickly valuation errors get caught.

What types of bookkeeping work for retail businesses?

Retail inventory accounting requires double-entry bookkeeping and accrual-basis accounting. Single-entry can’t support COGS tracking. Cash-basis expenses inventory when purchased rather than sold, distorting profitability. Accrual matches COGS to the period inventory was actually sold, which is the correct foundation for the retail method and any cost-based alternative.

Hi there I am so excited I found your site, I really

found you by accident, while I was researching on Google for something

else, Regardless I am here now and would just like to say cheers for a incredible post and a all round thrilling blog (I also love the theme/design), I

don’t have time to go through it all at the minute but

I have book-marked it and also added in your RSS feeds, so

when I have time I will be back to read a great deal more, Please do keep up the fantastic work.

Thanks for the interesting article. Apart from accounting, you can do a lot more analysis in a store, like competitive analysis. You can succeed or stay caught up in the market. It’s up to you.