Accurate knowledge of a business’s expenses is a critical element of accounting. This information makes it easier to ascertain whether a profit is being made. This is where cost accounting plays a crucial role. Cost accounting analyses the costs associated with running a business, including direct and indirect expenses.

In this article, we will delve into the definition and purpose of cost accounting, explore the different types of costs, and discuss the importance of cost accounting in business and its challenges and limitations. Moreover, we will provide an overview of the various costing methods and examine the differences between cost accounting and financial accounting, as well as the accounting programs used by cost accountants to manage costs and generate reports.

By the end of this article, you will have a comprehensive understanding of cost accounting, its importance in business management, and the various techniques cost accountants use to track, analyze, and manage costs. Ready to master cost accounting? Let’s dive in!

Contents:

2. Types of costs in accounting

3. Cost vs financial accounting

4. Methods of costing in accounting

6. Accounting software for cost accountants

7. Importance

9. Conclusion

10. FAQs

Definition & purpose

Cost accounting is a field of accounting that involves the analysis and management of costs associated with producing goods or services. The main objective of cost accounting is to provide businesses with detailed cost information, which can be used to make informed choices regarding pricing, production levels, and resource allocation.

Cost accountants use specialized accounting software and techniques to analyze and track costs, including fixed, variable, indirect, and direct costs. By providing businesses with comprehensive cost information, cost accounting helps to improve cost efficiency, control expenses, and increase profitability.

Types of costs in accounting

Cost accountants consider fixed, variable, indirect, and direct costs. Let’s examine them more closely.

1. Fixed

Fixed costs do not vary with the level of production or output. They remain constant over a specific period, regardless of whether a business produces more or fewer products or services. Examples of fixed costs include equipment, machinery, insurance, and loans.

2. Variable

Variable costs are the costs that vary with the level of production or output. These costs increase or decrease based on the number of goods or services produced. Examples of variable costs include the cost of raw materials, direct labour costs, and the cost of shipping and distribution.

Variable costs directly affect a business’s profitability. As the level of production increases, variable costs increase, reducing a product’s profit margin.

Read more about variable expenses.

3. Operating or indirect

Operating costs, also known as operating expenses, are expenses incurred in its day-to-day operations. These expenses are necessary to keep the business running, and they include all indirect costs that are not directly related to the production of a product or service. For example, operational costs include rent, utilities, salaries and wages, insurance, office supplies, marketing, and maintenance. Operating costs are an essential component of cost accounting because they affect the overall profitability of the business. By carefully managing operating costs, businesses can improve their bottom line and achieve better financial results.

4. Direct

Direct costs are expenses directly related to producing a specific product or service. These costs can be traced back to a particular product, project, or department. Examples of direct costs include permissible expenses for components, labour, and any expenses directly associated with the production process, such as shipping and handling fees.

Direct costs are an important consideration in cost accounting because they can be easily attributed to a specific product or service and help businesses determine the actual cost of producing a product or service.

Learn more about different types of expenses. Check out our article on Selling, General and Administrative Expenses.

Cost vs financial accounting

Cost accounting and financial accounting are two distinct fields of accounting, each with its own set of objectives, methods, and outcomes. Here are some key differences between the two:

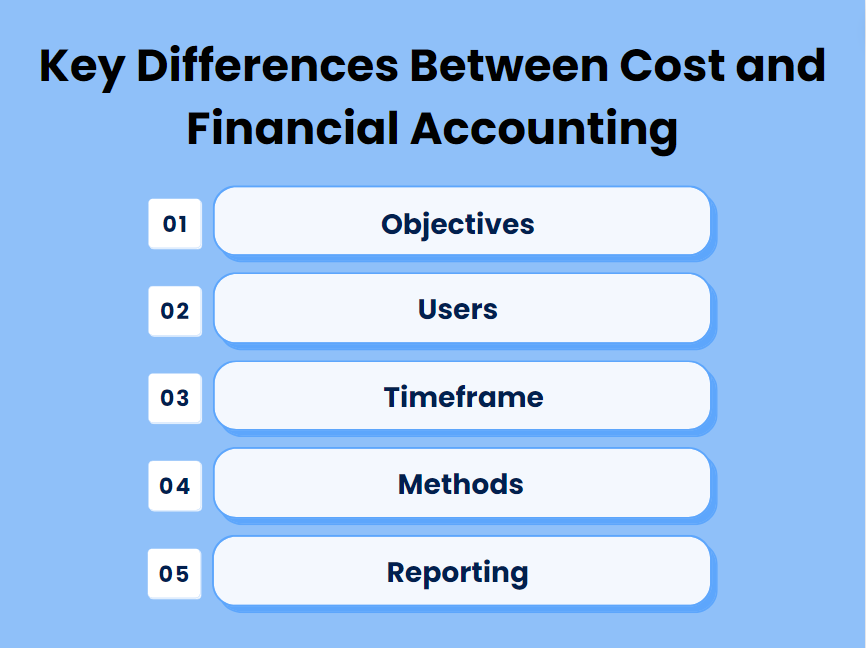

1. Objectives

The main objective of cost accounting is to provide detailed cost information to help businesses make informed decisions about pricing, production levels, and resource allocation. Financial accounting, on the other hand, is primarily concerned with recording and reporting a company’s financial transactions to external stakeholders, such as investors and regulatory agencies.

2. Users

Cost accounting is primarily used by internal stakeholders, such as managers and executives, who need cost information to make decisions about the company’s operations. Financial accounting, in its turn, is used by external stakeholders, such as investors and creditors, who need financial information to evaluate the company’s financial performance and make investment choices.

3. Timeframe

Cost accounting typically focuses on shorter timeframes, such as weekly or monthly periods, while financial accounting concerns longer timeframes, such as quarterly or annual periods.

4. Methods

Cost accounting uses specialized accounting apps and techniques to analyze and manage costs, including fixed, variable, indirect, and direct costs. Financial accounting uses generally accepted accounting principles (GAAP) to record and report financial transactions.

5. Reporting

Cost accounting generates reports that are used internally to make decisions about the company’s operations. Financial accounting creates financial statements, such as balance sheets, income statements, and cash flow statements, that are used externally to provide a snapshot of the company’s financial performance.

Methods of costing in accounting

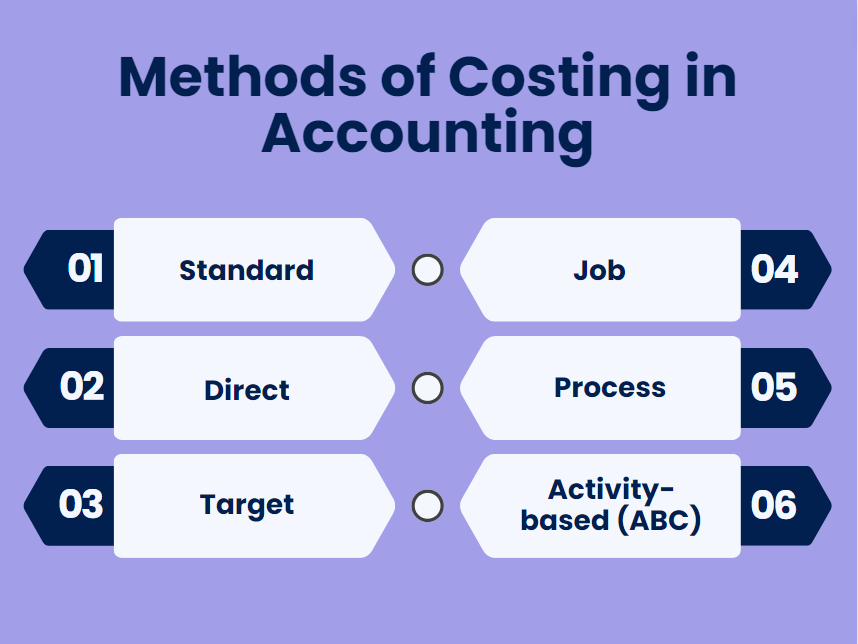

Costing is an essential part of cost accounting, and businesses can use different costing methods to analyze the costs associated with producing goods or services. Here are six common methods of costing:

1. Standard

Standard costing is a method of costing that involves setting predetermined costs for materials, labor, and overhead, and then comparing the actual costs of production against these predetermined costs. By analyzing these variances, businesses can identify areas where costs are higher than expected and take steps to reduce them.

2. Direct

Direct costing, also known as variable costing, is a method of costing that only considers the variable costs associated with producing a product or service. Fixed costs, such as rent and salaries, are not included in the cost calculation. By focusing solely on variable costs, businesses can determine the actual cost of producing a product or service and make more informed pricing and resource allocation decisions.

3. Target

Target costing is a method of costing that involves setting a target cost for a product or service based on customer demand and market conditions and then working backwards to determine the permissible expenses for components, labour, and overhead. By using this method, businesses can ensure that they produce products or services that meet customer demand and are priced competitively.

4. Job

This method involves tracking the direct and indirect costs associated with a particular job or project and allocating those costs to the job or project. Job costing is commonly used in service-based businesses, such as consulting firms, construction companies, or advertising agencies, where each job or project is unique and requires different levels of resources to complete.

5. Process

The product costing method involves tracking the direct and indirect costs associated with each stage of the production process and allocating those costs to the final product. This method is commonly used in manufacturing businesses, where the production process involves a series of stages, and the final product is the result of several intermediate steps.

6. Activity-based (ABC)

This method involves tracking the direct and indirect costs associated with each activity or task and allocating those costs to the final product. ABC is commonly used in service-based businesses, such as financial services, healthcare, or information technology, where the production process involves a series of complex activities.

Each costing method has its advantages and disadvantages, and businesses should choose the method that best suits their needs based on the nature of their operations and the level of detail required for cost analysis.

Who are cost accountants?

Cost accountants are professionals who specialize in analyzing, tracking, and managing costs within a business or organization. They collect and interpret financial data related to production, operations, and other activities to provide insights into cost structures and profitability.

Cost accountants often work closely with management teams to formulate financial plans, establish pricing strategies, and identify areas for cost reduction or optimization. They play a crucial role in helping businesses make informed financial decisions and achieve their strategic objectives.

What is the difference between a CPA and a cost accountant?

While both professions deal with financial matters, there are distinct differences.

A Certified Public Accountant (CPA) is a broad designation covering various areas of accounting, including auditing, taxation, and financial reporting.

On the other hand, a Cost Accountant specializes in cost-related aspects of accounting, focusing specifically on analyzing, tracking, and managing expenses within an organization.

While CPAs may work in various accounting roles, including cost accounting, Cost Accountants specifically concentrate on cost-related activities to help organizations make informed financial decisions and improve efficiency in cost management.

Explore How to Choose Business Accountant: Best Accounting Firms and CPA Professionals.

What skills are required?

Cost accountants require a combination of analytical, mathematical, and communication abilities to effectively analyze financial data and provide insights for decision-making within an organization. They need proficiency in accounting principles, budgeting, cost analysis, and financial reporting. Additionally, strong attention to detail and problem-solving abilities are crucial for identifying cost-saving opportunities and optimizing financial processes.

What degree is required?

A bachelor’s degree in accounting, finance, or a related field is typically required to become a cost accountant. This degree provides a solid foundation in accounting principles, financial analysis, and business management, essential for success in this profession. Additionally, obtaining certifications such as Certified Management Accountant (CMA) or Chartered Global Management Accountant (CGMA) can further enhance career prospects and demonstrate expertise in cost accounting.

Browse our CPA directory to find accounting experts with ease.

Accounting software for cost accountants

Cost accountants use specialized accounting apps to manage costs and generate reports. For example, accounting software programs can help accountants track actual costs versus standard costs, which are predetermined costs used to estimate production costs. By comparing actual costs to standard costs, accountants can identify areas where costs are higher than expected and take steps to reduce them.

If you are a CPA and want to manage your expenses and generate accurate reports, you can do it with the help of smart automated software.

Discover CPA Automation: 5 Benefits of Automated Accounting For CPA Firms.

How Synder can help simplify cost accounting

Synder is a comprehensive business solution offering various features to help manage expenses effectively. With instant analytics and reporting, Synder Sync provides detailed expense reports encompassing all business aspects, including storage, platform fees, shipping, taxes, and more. By integrating with your sales channels and platforms, Synder enables you to track all your expenses in one place, offering a centralized solution for expense management.

You can explore the features of Synder with our specialist by booking office hours, or you can start a free 15-day trial and experience the benefits of automation for yourself. Optimize your expense management with Synder, and take advantage of its advanced capabilities for clean books and better financial results.

Importance

Cost accounting is an important aspect of managing a business, providing valuable insights into the costs of producing goods or services. Here are some reasons why cost accounting is important in business:

- Accurate pricing. Cost accounting helps businesses set accurate prices for their products or services by considering all costs associated with production, including direct and indirect costs. By accurately pricing their products or services, businesses can maintain profitability and remain competitive in the market.

- Improved cost management. Cost accounting allows businesses to identify areas where costs are higher than expected and take steps to reduce them. This can include reducing waste, optimizing resource allocation, and improving production efficiency. Businesses can improve profitability and maintain financial stability by managing costs more effectively.

- Better financial decisions. Cost accounting provides businesses with accurate and detailed financial information, which can be used to make informed decisions, identify areas where investments are needed, such as new equipment or technology, and improve production efficiency and profitability.

- Compliance with regulations. Cost accounting helps businesses comply with regulations related to financial reporting and taxation. By maintaining accurate records of all costs associated with production, businesses can ensure that they are in compliance with regulatory requirements.

- Enhanced budgeting and forecasting. Cost accounting provides businesses with accurate cost information that can be used for budgeting and forecasting. By using this information, businesses can make informed decisions about future investments and production levels, ultimately leading to better financial results and improved profitability.

Challenges & limitations

While cost accounting is an important tool for managing costs and improving profitability, there are some challenges and limitations to consider.

1. Cost allocation accuracy

One of the biggest challenges of cost accounting is accurately allocating costs to products or services. Indirect costs, such as overhead expenses, can be difficult to allocate accurately, and different cost allocation methods can produce different results.

2. Time & resources

Additionally, cost accounting can be time-consuming and require significant resources to maintain accurate records and analyze data. This can be a challenge for small businesses or those with limited resources. That is why it’s important to have a reliable accounting program in use.

3. Standardization issues

Another problem with cost accounting is the lack of standardization. There are many different cost accounting methods, and there is no standardized approach. This can make it difficult to compare costs across different businesses or industries.

4. Assumptions in costs

Cost accounting relies on assumptions about production costs, and these assumptions may not always be accurate. Changes in production methods or other factors can lead to inaccuracies in cost accounting data.

5. Scope limitations

Finally, there is a problem of limited scope. Cost accounting focuses primarily on the costs associated with producing goods or services. It may not take into account other factors that contribute to profitability, such as customer demand or market conditions.

Despite these challenges and limitations, cost accounting remains an important tool for managing costs and improving profitability. By being aware of these challenges and limitations, businesses can take steps to address them and use cost accounting effectively to achieve their financial goals.

Conclusion

Сost accounting is essential for businesses seeking to manage costs, increase profitability, and run their operations more efficiently. Cost accountants use specialized accounting software and techniques to analyze costs, including fixed, variable, indirect, and overhead costs. By using accounting solutions, such as cost-volume-profit analysis, budgeting, and variance analysis, businesses can make better decisions and achieve better financial results.

FAQs

1. What is cost accounting in the public sector?

Public sector cost accounting involves using accounting methods to track and manage finances in government and non-profit organizations. It ensures transparency, accountability, and efficient use of public funds, helping decision-makers make informed choices and deliver services effectively.

2. What does a cost accountant do?

A cost accountant analyzes and tracks a company’s expenses to ensure efficient financial management. They collect and analyze data related to production costs, overhead expenses, and other expenditures to help businesses make informed decisions about pricing, budgeting, and resource allocation. Cost accountants play a crucial role in cost control, identifying areas for cost reduction and optimizing operational efficiency.

3. What is cost accounting software/program?

Cost accounting software/program is a tool that helps businesses track and manage expenses efficiently. It includes features like job costing, budgeting, and financial reporting, enabling businesses to optimize costs and improve profitability.

4. What’s the difference between cost and financial accounting in handling money?

Cost accounting focuses on internal cost management within a business, providing detailed insights into production costs for decision-making regarding money. Financial accounting, however, primarily deals with reporting financial transactions to external stakeholders through statements like balance sheets and income statements.

Reading your blog about cost accounting was such a delight. It’s clear that you’re incredibly knowledgeable and passionate. Thank you for sharing your expertise in such an insightful way!