Often seen as a luxury for small businesses, a welfare package including retirement benefits is considered to be reserved for medium-sized and large companies. However, the variety of retirement plans existing today might help small business owners to get hold on great retirement plan options, thus securing the financial future for themselves and their employees.

In this article, we’re looking closer at different types of 401(k) plans, their benefits for small businesses and the steps to take while adopting a 401(k) plan.

Contents:

1. What is 401(k) for small businesses?

2. Types of 401(k) plans for small businesses

- 401(k) retirement plans: Traditional 401(k) plan

- 401(k) retirement plans: Safe harbor 401(k) plan

- 401(k) retirement plans: SIMPLE 401(k) plan

- 401(k) retirement plans: Solo 401(k) plan

- 401(k) retirement plans: Roth 401(k) plan

3. Benefits of 401(k) retirement plans for small businesses

- Tax benefits

- Talent attraction and retaining

- Financial wellness and security

- Investment opportunities

- Administrative options for small businesses

4. 401(k) contribution limits for small business owners and employees

5. How to establish a 401(k) plan for a small business?

6. Bottom line

Key takeaways:

- 401(k) plans are employer sponsored retirement savings options offering significant benefits for both small businesses and their employees.

- 401 (k) offers a variety of choices (Traditional, Safe harbor, SIMPLE, Solo, Roth plans) suitable for small businesses.

- Small businesses can establish a 401(k) plan by following a number of steps.

What is 401(k) for small businesses?

If we look at the retirement basics in the USA, the normal retirement age varies from 65 to 67 years today and thinking about such a distant future may not be the strong suit for many young people. Even if a retirement plan is offered, some workers don’t participate. Hence, many Americans enter their retirement with little or no savings at all. Sometimes it’s the employer who takes it into their hands enrolling their employees into a retirement plan chosen before.

As there are many different types of retirement plans, let’s look at what 401(k) is. Type 401(k) retirement plans, established under the Internal Revenue Code, offer a tax-advantaged savings mechanism for employees seeking to accumulate funds for their retirement period. Employees enrolled in these plans contribute a part of their pre-tax salary to individual accounts, which fosters disciplined retirement planning. Furthermore, 401 (k) retirement plans are called employer-sponsored, as employers can choose to match employee contributions, increasing the financial benefits of participation. This employer-sponsored incentive makes 401(k) plans a popular choice among eligible employees nationwide.

Types of 401(k) plans for small businesses

401(k) retirement plans include such options as traditional 401(k) plans, safe harbor 401(k) plans and SIMPLE 401(k) plans, Solo 401(k) and Roth 401 (k) plans. All of them can be a good retirement option for a small business. One of the most important things to mention here is that all the 401(k) plans can be divided into pre-tax and after-tax plans. Let’s start with pre-tax plans.

401(k) retirement plans: Traditional 401(k)plan

Traditional 401(k) plans are employer-sponsored retirement savings arrangements based on pre-tax elective deferrals. This means that employee contributions to their 401(k) accounts are deducted from their pre-tax salary, lowering their taxable income and potentially reducing their current tax liability. However, ordinary income tax is applied to the entire amount withdrawn from the account, including both contributions and investment earnings, upon distribution (typically in retirement).

Employer contributions with 401(k) are optional and can be divided into two types:

- Direct contributions are made on behalf of all plan participants.

- Matching contributions match a portion of employees’ elective deferrals, up to a certain limit, as an incentive for participation.

Any employer contributions, regardless of the chosen method, must comply with nondiscrimination testing to ensure fair and equitable treatment for all eligible employees.

401(k) retirement plans: Safe harbor 401(k) plan

Safe harbor 401(k) plans share similarities with traditional 401(k) plans, but offer a key distinction regarding employer contributions. Employer contributions are mandatory, and regardless of the type (matching contributions, employee-deferral contributions, or non-elective contributions), are fully vested at the time of contribution.

Vesting, in the context of retirement plans, refers to an employee’s ownership of their accumulated benefits. Once vested, these contributions can’t be forfeited or retrieved by the employer under any circumstances. This mandatory vesting feature ensures immediate ownership of employer contributions and offers a greater sense of security and control over retirement savings.

Unlike traditional 401(k) plans, safe harbor plans are exempt from annual nondiscrimination testing, which simplifies administrative burdens of testing procedures for employers.

401(k) retirement plans: SIMPLE 401(k) plan

The SIMPLE 401(k) plan is for small businesses with 100 or fewer workers. If a business grows and exceeds 100 employees, they have two years before they need to switch to a different plan. This plan is good for businesses that are growing because it’s cheaper than other retirement plans.

With the SIMPLE plan, the employer has to put in money for their employees’ retirement. This ensures that all the money put in belongs to the employees right away. Unlike other plans, the SIMPLE plan makes employers choose between matching their employees’ contributions up to 3% of their pay or giving a non-elective contribution of 2% of their pay.

For employees to join the SIMPLE 401(k) plan, they need to have earned at least $5,000 from the employer in the previous year. Also, this plan doesn’t have to go through certain yearly tests like other plans do.

The requirements for the employers who intend to establish the SIMPLE 401(k) plan are the following:

- 100 or fewer employees;

- No other retirement plans;

- Filing a Form 5500 annually.

401(k) retirement plans: Solo 401(k) plan

This plan is sometimes referred to as Solo-k, Uni-k and One-participant k. Basically, Solo-k is a traditional 401(k) that covers a business owner with no employees besides spouses. These plans follow the same rules and requirements as any other 401(k) plan, but the employee and the employer are the same person, which means that contributions can be made in both capacities. The contributions shouldn’t exceed the following limits.

If you’re self-employed, you can put 100% of your “earned income” into your retirement account, and up to $23,000 if you’re 50 or older. Your employer can also put in up to 25% of your pay into the account, as defined by the retirement plan.

Let’s look at the option of an after-tax plan and how it works in the context of retirement savings.

401(k) retirement plans: Roth 401 (k) plan

Unlike traditional 401(k) contributions, the tax on Roth deferrals is paid upfront, which means that Roth(k) plans are funded with post-tax dollars and called an after-tax retirement savings option. When you withdraw money from your Roth 401(k) account, you don’t have to pay taxes on it as long as you meet certain rules. However, early withdrawals (prior to age 59,5) from Roth 401(k) plans, except for certain qualified expenses, may be subject to taxation and penalties.

In a Roth 401(k), when you put in money, your employer might match it just like they do in a regular 401(k). The difference is, the money you put in goes into your Roth 401(k) account, while the money your employer puts in goes into a regular 401(k) account. This makes handling Roth plans harder to handle for employers.

Overall, opting for a Roth 401(k) plan may be a strategic decision for those who anticipate being in a higher tax bracket during retirement.

Benefits of 401(k) retirement plans for small businesses

Being a popular choice among employees and employers is attributed to a number of benefits offered by 401(k) plans.

Tax benefits

401(k) plans offer a compelling tax incentive to employees who choose to set aside a portion of their pre-tax salary for their retirement savings. These contributions can then be invested in various investment options such as mutual funds and exchange-traded funds, depending on the specific plan offered by the employer. Employee contributions and associated investment earnings from retirement plans are subject to deferral of taxation until the time of distribution, which generally occurs after retirement. In simple terms, the taxes are postponed until the money is withdrawn. This is especially beneficial if you’re in a lower tax bracket when you retire. It has to be noted that this tax treatment doesn’t apply to Roth 401(k) plans.

Employer contributions to 401(k) plans are tax-deductible on their federal income tax return, up to certain limits established by the IRS, which is a significant tax benefit for small businesses.

Prepare your small business for tax season with these 14 tax tips.

Talent attraction and retaining

Offering a 401(k) can be one of the factors that makes small businesses more attractive for their potential employees prioritizing on retirement savings. As 401(k) is an instrument that helps take control of the financial future, it can contribute to employee loyalty and satisfaction giving a small business a competitive edge in today’s job market. Thus, offering employee benefits can be a real game changer for your small business.

Financial wellness and security

While 401(k) retirement plans allow employees to decide how much to contribute to their accounts, many small businesses offer matching contributions to incentivize employee participation, boosting their retirement savings and demonstrating commitment to their well-being. At the same time participants can take their benefits with them when they leave the company, which makes administrative responsibilities much easier. 401(k) accounts offer protection from creditors if you find yourself in financial troubles.

Investment opportunities

401(k) retirement plans rules allow you to contribute money to grow through investments in stocks, bonds, mutual funds, money market funds, savings accounts, and other investment options.

Administrative options for small businesses

401(k) offers a variety of plans available for small businesses, including SIMPLE and Solo 401(k), which are often simpler and less expensive to administer compared to traditional plans. At the same time, there’s an option to outsource 401(k) services with many investment firms and financial institutions offering affordable administration options for small businesses.

All the benefits considered, 401(k) seems to be a great option for small businesses.

401(k) contribution limits for small business owners and employees

All retirement plans have certain rules on how much money you can defer. In 2024, for 401(k) plans, the most an employee can set aside from their salary is $23,000. According to the Secure 2.0 Act, if you’re 50 or older, you can add an extra $7,500 to your 401(k) plan. The most that both you and your employer together can put into a 401(k) plan in 2024 is $69,000.

For SIMPLE plans, if you’re 50 or older, you can add up to $3,500 extra in 2024. The most you and your employer can put into a SIMPLE plan in 2024 is $16,000.

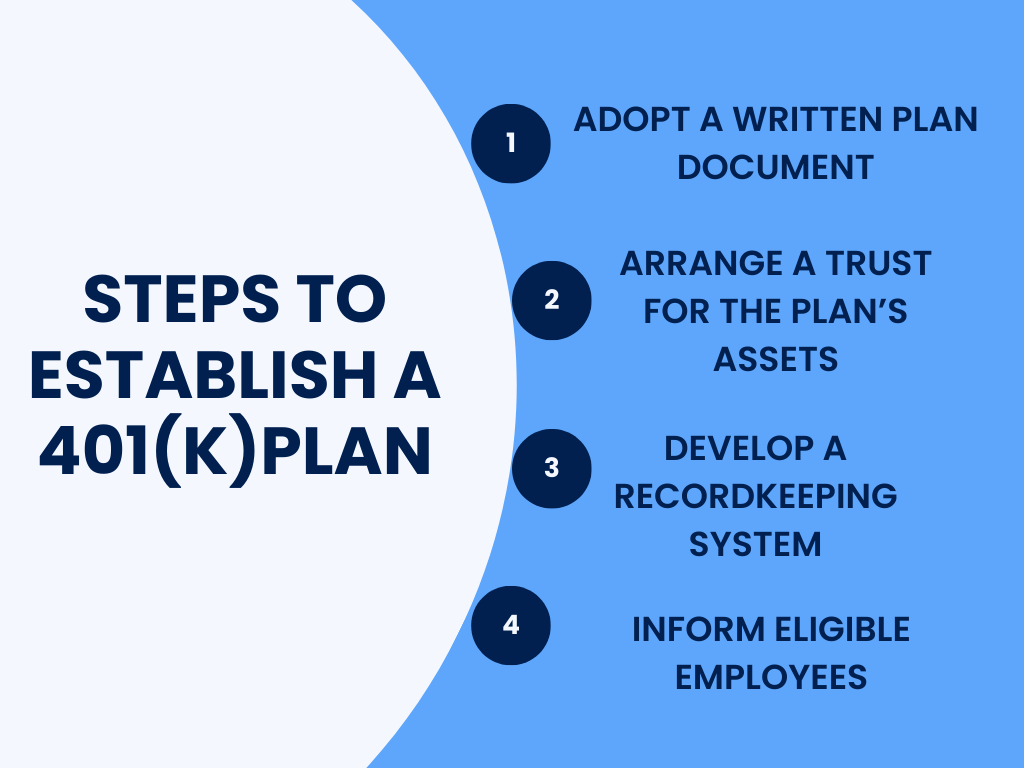

How to establish a 401(k) plan for a small business?

According to the information given by the U.S. Department of Labor’s Employee Benefits Security Administration (EBSA) and the Internal Revenue Service, when you chose the retirement plan for your small business, the options are that you can run it on your own or use a provider of financial services to establish and maintain the retirement plan. If you choose the first option, there are four main points to focus on when establishing a 401(k) plan:

- a written plan document;

- a trust for the plan’s assets;

- a recordkeeping system;

- information you need to provide to employees eligible to participate.

Written plan document

Adoption of a 401(k) plan starts with a written foundation plan covering daily operations needed to maintain it. You’ll also need to choose the type of plan that fits your business best. All the plans described above are suitable for small businesses and provide the opportunity for employees to contribute through salary deductions.

Traditional 401(k) plans give employers the flexibility to decide if they want to contribute for all employees, match what employees contribute, do both, or do neither. The point to be taken into consideration is that while offering freedom, a traditional 401(k) is subject to the annual non-discrimination contributions testing unlike some other plans like safe harbor 401(k), for example. At the same time such plans may require mandatory employer contributions. Therefore, it makes sense to work out which plan is best in each particular case.

After choosing the type of the plan, employers have to decide on the features of the plan. There’s a certain degree of flexibility here depending on the plan and the written plan document must describe the key functions like the way contributions are deposited in the plan, or if there is an option of direct investments by employees.

Trust for the plan’s assets

The second step to focus on is to arrange a trust for the plan’s assets to ensure that the assets are used for retirement benefits only. Normally all the contributions, plan investments, and distributions are handled by at least one trustee, and choosing them is a very important decision. However, setting up the retirement plan through insurance contracts means that you don’t have to keep such contracts on a trust.

Recordkeeping system

Developing and implementing an accurate recordkeeping system will help you track and properly attribute contributions, earnings, losses, plan investments, expenses, and benefit distributions. If you decide to outsource, a contract administrator or financial institution will keep the required records in order, which can later be used while preparing the plan’s annual report for the Federal Government.

Information you need to provide to eligible participants

It’s the duty of employers to inform their employees eligible to participate in the plan on their rights, benefits and the features of the chosen retirement plan. All the participants must be provided with a summary plan description (SPD) with the details about the plan and the way it operates. In addition, it’s a good idea to highlight the information on the benefits of the plan for employees, which might boost their participation. A 401(k) plan may be established as late as the due date (including extensions) of the company’s income tax return in the year you decide to establish the plan.

Bottom line

As the new tendency in the retirement welfare sector is to expand the coverage of retirement plans and increase employee participation in them, it’s the best time for small businesses to choose the appropriate plan and establish it. This step will not only make a small business compliant with the retirement laws but also help attract and retain talented employees by providing them with the opportunity to take charge of their future financial wellbeing.

What’s the best retirement plan for a small business in your view? Share in the comments below!