Have you ever received your income and wondered why the amount you get is less than what you expected? Understanding post-tax deductions can be critical in managing your own or your business finances and maximizing your income.

In this article, we’ll learn about post-tax deductions, explore their different types, and help you understand how they can impact your finances. So, let’s get started so that you can take control of your financial future!

Contents:

1. What are post-tax deductions?

2. Tax deduction for small businesses

3. How can accounting software help cope with tax season?

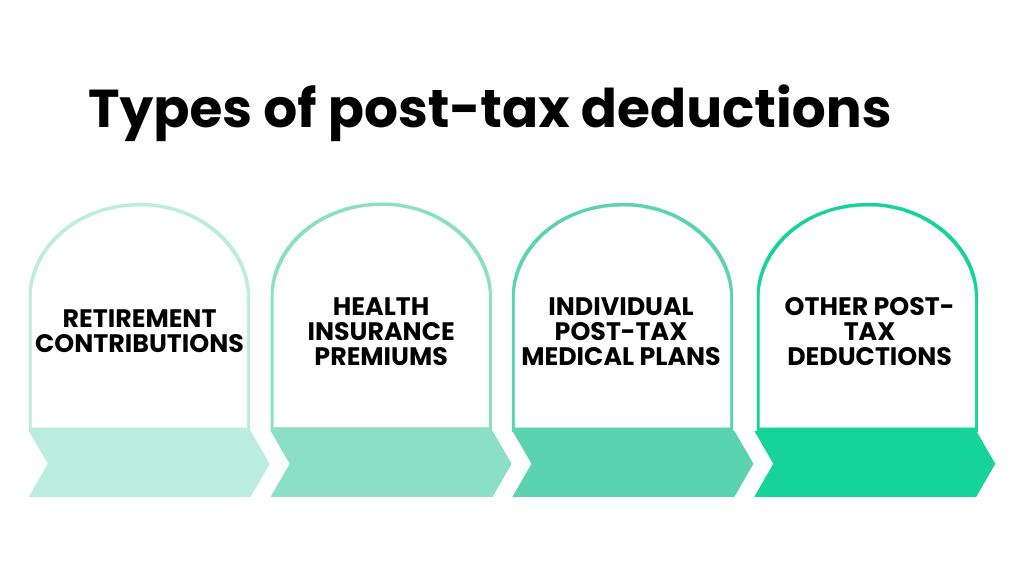

4. Types of post-tax deductions for individuals

- Retirement contributions

- Health insurance premiums

- Individual post-tax medical plans

- Other post-tax deductions

5. The impact of post-tax deductions on your income

6. How to calculate your post-tax deductions

Key takeaways

- Deductible expenses for small businesses include advertising costs, bank fees, business meals, insurance premiums, salaries, taxes, etc.

- Individuals can also benefit from post-tax deductions like retirement contributions and health insurance premiums.

- Post-tax deductions provide an opportunity for individuals and businesses to optimize their tax strategies and improve their financial health.

What are post-tax deductions?

Post-tax deductions are amounts taken from your paycheck after taxes are withheld. They reduce your take-home pay but can offer valuable benefits for your future financial security. On the other hand, business tax deductions help decrease the amount you’ll be taxed on, meaning you’ll owe less to the government during tax season.

Note: To ensure you’re maximizing your deductions, it’s wise to consult with a professional like a CPA. They’re experts in identifying which deductions you qualify for and can help you save money on your taxes.

These deductions, whether mandatory or voluntary, come in various types, which we’ll discuss shortly.

Understanding the difference between post-tax and pre-tax deductions is crucial. Post-tax deductions are taken after taxes, while pre-tax deductions are subtracted before taxes are calculated.

Tax deduction for small businesses

Here you’ll find a list of common expenses that could be subject to taxes for your small business. It’s important to remember that while these deductions are available, not all of them may be relevant or beneficial to your specific business circumstances.

So, it’s really important to think about each deduction and decide if it makes sense for your business before you claim it on your tax return. By doing this, you can make sure you’re making smart choices and saving as much money as possible on your taxes, all while following the rules that apply to your business.

Advertising and promotion

Advertising and promotion costs are fully deductible, such as:

- Hiring someone to design a logo;

- Cost of printing materials;

- Purchasing ad space;

- Sending client cards;

- Launching a website;

- Running social media campaigns.

However, expenses for lobbying or sponsoring political campaigns/events are not deductible.

Bank fees

It’s a good idea to keep your business finances separate by using different bank accounts and credit cards. If your business bank or credit card company charges you annual or monthly fees, transfer fees, or overdraft fees, you can deduct these costs.

In addition, any fees you pay to third-party payment processors such as PayPal or Stripe may also be deducted.

Note: You can’t deduct fees associated with your personal bank accounts or credit cards.

Business meals

You can deduct 50% of qualifying food and beverage costs for your business. To qualify:

- The expense must be necessary for your business.

- The meal should not be overly extravagant.

- You or your employee must be present.

- Meals provided to employees or at office parties are fully deductible.

Keep records of expenses, including amount, date, place, and business relationship.

Business insurance

You can deduct the premiums you pay for business insurance, including:

- Coverage for property;

- Liability coverage;

- Employee health;

- Professional liability;

- Workers’ compensation;

- Business vehicle auto insurance;

- Business interruption insurance.

Business use of your car

If you use your vehicle for business, you can deduct the costs associated with business-related usage. There are two deduction methods:

- Standard mileage rate: Multiply business miles by the standard mileage rate (e.g., $0.655 per mile in 2023).

- Actual expense method: Track all vehicle operating costs for the year (gas, repairs, insurance, etc.), then multiply by the percentage of miles driven for business.

Be sure to keep a record of your business-related mileage, and once you’ve chosen a method for a specific vehicle, stick with it. Remember, you can’t deduct miles for your regular commute.

Contract labour

If you hire freelancers or independent contractors for your business, you can deduct their fees as a business expense. If you pay a contractor $600 or more in a tax year, you must send them a Form 1099-NEC by January 31st of the following year.

Depreciation

When you buy business assets like furniture and equipment, you can’t deduct their full cost immediately. Instead, you spread the cost over several years through depreciation. However, there are ways to write off the full cost in one year:

- De minimis safe harbor election: Small businesses can deduct the cost of items that are less than $2,500 each in the same year they buy them.

- Section 179 deduction: This means you can deduct up to $1,080,000 worth of things you started using in your business during the tax year. This includes both new and used items, as well as off-the-shelf software.

- Bonus depreciation: Businesses can deduct 100% of the cost of certain assets like machinery, equipment, and furniture.

Note: When you buy a new vehicle for your business, there are rules that limit how much you can deduct for its depreciation. However, with bonus depreciation, you can boost your deduction to $18,100 in the first year.

Salaries and benefits

Salaries, benefits, and vacation time paid to employees are tax-deductible if:

- The employee isn’t a sole proprietor, partner, or LLC member.

- The salary is reasonable, ordinary, and necessary.

- The services were actually provided.

Taxes and licenses

You can deduct various business-related taxes and licenses, such as:

- State income taxes;

- Payroll taxes;

- Property taxes;

- Sales tax;

- Excise taxes;

- Fuel taxes;

- Business licenses.

Rent expense

You can deduct rental payments for business locations or equipment as a business expense. However, the rent paid for your home, even if you have a home office, shouldn’t be deducted as a business expense. Instead, it can be part of home office expenses.

Since you’re interested in deductions, probably you’re doing your taxes and want to do them correctly to avoid any stress come tax season.

How can accounting software help cope with tax season?

Accurate records throughout the tax year are essential for effective tax planning and preparation. However, many ecommerce business owners don’t collect financial information regularly and often end up madly bringing their business transaction data into books at the beginning of the tax season.

Automation software can be very helpful when working with money. It allows you to connect all your sales channels and payment platforms with your books and banking records, eliminating manual data entry.

Want to ensure your business is tax season-ready at any time? It’s time to find the automated software to ensure your books are clean and ready for reconciliation.

How can Synder help with tax management?

Synder Sync is just what you might be looking for. Boasting 30+ integrations, Synder’s able to import all your transactions from multiple sales channels and payment gateways.

Every transaction is synchronized hourly to import detailed data, including tax, product, and customer information, with cross-checking for duplicates and discrepancies for thorough financial accounting.

What exactly can Synder do to smooth tax season for you?

Calculating sales tax for ecommerce businesses can be complex due to multiple sales channels and payment platforms involved. Synder simplifies this process by calculating taxes based on the sales total and tax amount, using transaction data from your ecommerce platforms and various payment processors integrated into them (for example, Stripe, Square, PayPal, etc.). It then matches the calculated tax rate to the tax codes in your QuickBooks or Xero accounts.

Check this guide on how to set up sales tax in QuickBooks or Xero with Synder.

Learn the process by using Synder’s free trial or join Synder’s informative Weekly Public Demo. to make sure Synder is your right choice.

Types of post-tax deductions for individuals

There are several types of post-tax deductions that can impact your income and financial well-being. Some of the most common types of post-tax deductions include:

Retirement contributions

Many employers offer 401k plans, which allow employees to contribute a portion of their pre-tax income to a retirement account. While these contributions aren’t tax-deductible, they can provide significant tax benefits in the future, such as tax-deferred growth and tax-free withdrawals in retirement.

In addition to 401k plans, some employers offer other types of retirement plans, such as

- 403(b) plans offered by non-profit organizations, such as schools and hospitals.

- 457 plans usually offered by state, which allow employees to contribute a portion of their pre-tax income to a retirement account.

Contribution limits

It’s important to understand the contribution limits for your retirement plan to maximize your savings and plan for your future.

In 2024, the contribution limit for 401(k), 403(b), and most 457 plans for employees, as well as the federal government’s Thrift Savings Plan was increased to $23,000, up from $22,500.

It’s also important to mention that there may be additional contribution limits based on your income and the type of retirement plan you have.

There are several types of health insurance that may be offered by your employer:

- Medical insurance that covers the cost of medical care, such as doctor visits, hospital stays, and prescription medications.

- Dental insurance covering the cost of dental care, such as cleanings, fillings, and crowns.

- Vision insurance that provides for the cost of eye exams, glasses, and contact lenses.

There are additional types of benefits, which might be interesting to you:

- Life insurance;

- Disability insurance;

- Flexible spending accounts, which can provide valuable protection and financial support in case of illnesses, injuries, or other unexpected events.

Review your benefit options regularly and choose the ones that best meet your needs and financial goals.

Individual post-tax medical plans

Unlike pre-tax medical coverage that’s normally employer sponsored, this type of post-tax health premiums are individually purchased health insurance plans. When you pay for health insurance with money after paying each tax, you can get important coverage for disabilities or accidents.

Choosing a post-tax medical plan, you need to beware of its pluses and downsides. The negative side of such plans is obvious – your payments for medical insurance are non-deferred, so you get to pay now. However, there are certain benefits:

- You can drop your current medical plan and enroll in another one in the middle of the year.

- You don’t need to be officially employed.

- You can still save some money by listing medical premiums as itemized deduction or by using Schedule 1 for line 16 in Form 1040.

Other post-tax deductions

In addition to retirement contributions and medical insurance plans, there may be other post-tax deductions that are taken out of your payroll. These may include voluntary deductions like:

- Union dues;

- Charitable contributions;

- Wage garnishments (unpaid taxes, overdue child support, student loans, etc.).

This means that a portion of the employee’s net pay will be withheld and sent directly to the relevant organization, like a trade union, charity or court.

The impact of post-tax deductions on your income

After-tax deductions can have a big impact on your financial health. Let’s say you make $50,000 a year and contribute 5% of your salary to an individual 401k account. This will result in an after-tax deduction of $2,500 per year or $208.33 per month.

Or consider another example. Imagine you earn $30,000 a year and decide to put aside $50 each month from your paycheck to buy extra insurance for accidents. This money comes out after taxes are taken, so you get to keep the full $50 for insurance. If it were taken out before taxes, you’d have less money left to spend on insurance because taxes would be taken out first. So, using after-tax money means you get better value for your money when purchasing insurance.

That’s why it’s important to consider the impact of after-tax deductions when negotiating your salary and benefits with your employer.

How to calculate your post-tax deductions

Calculating your post-tax deductions can help you understand how they affect your income. To calculate your post-tax deductions, you’ll need to review your pay stub and identify the amounts taken out of your paycheck.

For example, to calculate your retirement contributions, review your 401k plan or other retirement plan information and identify the percentage of your income that’s being contributed. To calculate your health insurance premiums and other benefits, review your benefit information and identify the amounts being deducted from your payroll each month.

Once you’ve identified your post-tax deductions, you can subtract them from your gross pay to determine your take-home pay, which can help you plan your financial future.

For example, your gross wages are $2,000. Your FICA tax rate is 7.65%, additional taxes total $75, and Roth 401(k) after-tax deduction is 4%.

Here’s your take-home pay once FICA, which includes Social Security, Medicare taxes, and other income taxes, has been withheld:

- Multiply the gross pay by the FICA tax rate: $2,000.00 X 0.0765 = $153

- Multiply the gross pay by the deduction percentage: $2,000.00 X 0.04 = $80.00

- Subtract the FICA amount from the gross pay: $2,000.00 – $153 = $1847

- Subtract the additional taxes from the new total: $923.50 – $85.00 = $1762 – what you’d get paid but for your Roth 401(k) after-tax contribution, which has not been subtracted yet.

- Subtract the deduction amount from the new total: $1762 – $80.00 = $1682

Conclusion

Understanding post-tax deductions and deductible expenses is crucial for managing your money effectively and getting the most out of your income.

For businesses, knowing about related deductible expenses such as advertising costs, contract labor, and depreciation, helps in reducing your tax obligations and improving your financial situation.

For individuals, post-tax deductions, like contributions to retirement plans and health insurance premiums, may lower your take-home pay but offer important benefits for financial security and future planning.

And you should always keep in mind two important points: firstly, if you’re unsure or come across any difficulties with taxes, it’s advisable to seek guidance from a professional. Secondly, embracing modern technology to automate routine tasks can simplify your financial management process.

Want to learn more about taxes? Check out how to calculate payroll taxes, how to file income tax return, and what tax preparation tips for 2024 you need to know about.

Disclaimer: This article serves as a general overview and is not designed to offer personalized tax advice. Tax laws and regulations are complex and may vary based on individual circumstances. If you or your business require assistance with post-tax deductions or have specific tax-related inquiries, it is advisable to consult a qualified tax professional. Relying solely on the information provided in this article for tax preparation or decision-making is not recommended.