Inventory is often a retailer’s largest asset, and how you account for it shapes everything downstream: your COGS, your gross margin, your tax bill, and what your balance sheet looks like to a lender or acquirer. According to IHL Group’s 2025 research, the global retail industry loses $1.73 trillion annually to inventory distortion, much of which traces back to gaps in inventory visibility that start with the accounting method a business uses. When your method produces imprecise valuations or misses shrinkage entirely, the numbers you’re managing from aren’t the numbers that reflect reality.

Both retail accounting and cost accounting are GAAP-accepted approaches to valuing inventory, but they suit fundamentally different businesses and answer different questions. This article compares them head-to-head: how each works, how to calculate inventory value under each, how the choice ripples through your financial statements, and how to decide which fits your operation.

TL;DR

- Retail accounting uses selling prices: The retail inventory method estimates ending inventory value by applying a cost-to-retail ratio to the goods available for sale without counting every item.

- Cost accounting tracks actual purchase costs: Methods like FIFO, LIFO, and weighted average cost value inventory based on what you paid, making them more precise but more demanding to maintain.

- The method choice affects your income statement and balance sheet: FIFO, LIFO, and the retail method all produce different COGS and ending inventory figures for the same business, which has real implications for reported margins and asset values.

- Perpetual inventory systems have changed the equation: Modern ecommerce platforms track inventory in real time, which makes cost-based accounting significantly more practical than it was a generation ago.

- The right fit depends on your product mix and reporting needs: Uniform-markup, high-volume retailers often use the retail method; multi-channel sellers with variable pricing typically don’t.

What is retail accounting?

Retail accounting, more precisely called the retail inventory method (RIM), is an averaging technique that lets retailers estimate the value of their ending inventory without conducting a full physical count. Instead of tracking what each item cost to acquire, it works backwards from selling prices. The American Institute of CPAs recognizes it under GAAP (specifically ASC 330, Inventory), the IRS allows it for U.S. tax reporting, and it’s also available under IFRS, giving it wide applicability across jurisdictions.

The method has been popular with large retailers for decades precisely because physical counts across hundreds of SKUs and multiple store locations are impractical to run every reporting period. A clothing chain with 50 locations can’t realistically close every store to count socks and t-shirts each quarter, but it can apply the retail method to generate an estimated inventory balance quickly and cost-effectively.

How the cost-to-retail ratio works

The engine of the retail method is the cost-to-retail ratio, sometimes called the cost complement. It tells you what percentage of your retail selling price your cost of goods actually represents. If you stock a jacket that costs $60 to buy and sells for $100, your cost-to-retail ratio is 60%.

This ratio is calculated across your entire inventory pool, not item by item:

| Step 1: Add up the cost of all goods available for sale. Step 2: Divide it by the retail value of those same goods. |

That single percentage then converts any retail-priced figure, including your ending inventory balance, into an estimated cost figure.

The important nuance is what you include in the ratio:

- The conventional retail method counts markups but not markdowns, which produces a lower estimated cost and a more conservative inventory value – useful for financial reporting where understating assets reflects a recognized conservative approach.

- The cost retail method includes both markups and markdowns, producing a result closer to the actual average cost.

Neither version accounts for inventory shrinkage, which isn’t a small omission: the most recent National Retail Federation data puts U.S. inventory shrinkage at $112.1 billion (approximately 1.6% of total retail sales), and the NRF has since shifted to tracking retail theft and violence separately, signalling the problem has only grown more complex.

Inventory pooling: how large retailers make RIM work

One reason the retail method remains viable at scale is inventory pooling. Rather than applying a single blended cost-to-retail ratio across all merchandise, large retailers, like department stores, fashion chains, and multi-category operations, divide their inventory into groups, or “pools,” based on similar markup characteristics. Each pool gets its own ratio.

A department store might maintain separate pools for footwear, outerwear, cosmetics, and home goods, because the margin on a $300 coat is structurally different from the margin on a $20 lip liner. Mixing the two produces a ratio that’s inaccurate for both categories. Pooling preserves the speed advantage of the retail method while reducing the distortion that comes from averaging across very different price structures.

For smaller retailers and ecommerce businesses that lack the infrastructure to maintain category-level pools reliably, this complexity works against RIM rather than for it. When pooling isn’t feasible, that single ratio starts to fall apart as your product mix gets more varied.

Related read: “How to Create an Inventory System: A Guide for Businesses New to Inventory Management.”

Step-by-step: calculating ending inventory with the retail method

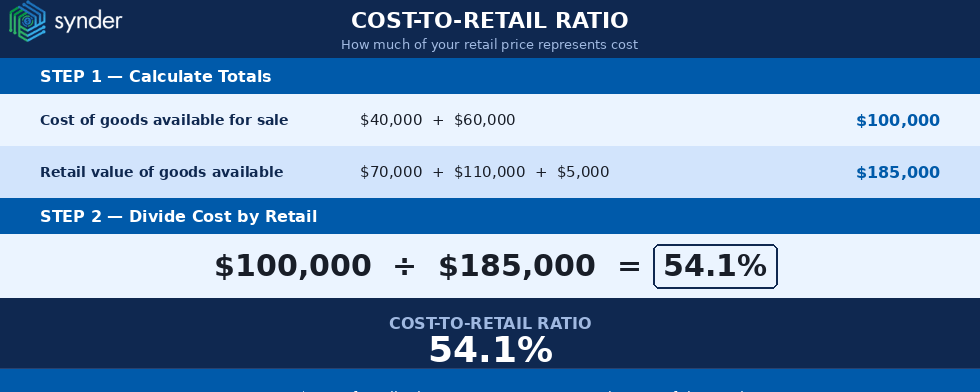

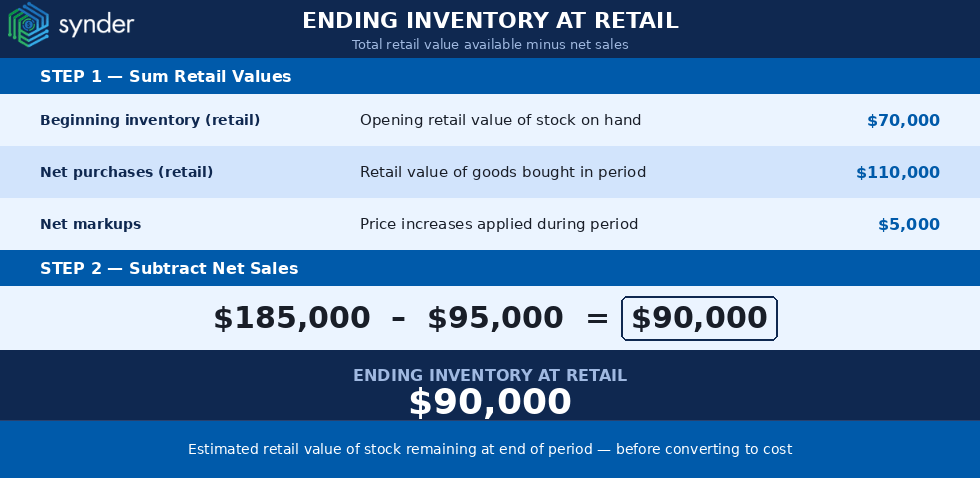

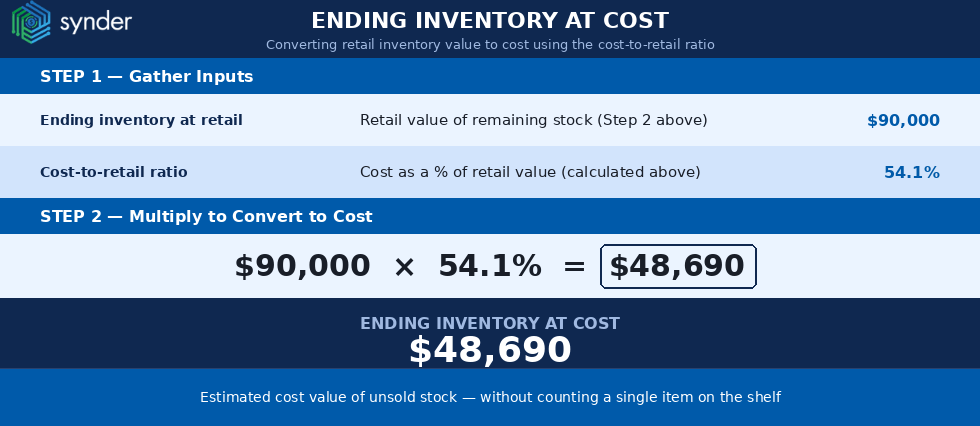

Here’s how the retail method looks for a mid-size apparel retailer at the end of a quarter. The figures:

- Beginning inventory: $40,000 at cost / $70,000 at retail

- Purchases during the period: $60,000 at cost / $110,000 at retail

- Net markups applied: $5,000

- Net sales for the period: $95,000

Step 1 – Cost-to-retail ratio:

Step 2 – Ending inventory at retail:

Step 3 – Ending inventory at cost:

The retailer estimates its ending inventory at approximately $48,690 in cost terms without counting a single item on the shelf. That’s the efficiency the retail method is designed to deliver.

What is cost accounting?

Cost accounting, in the context of inventory, means valuing your stock based on what you actually paid for it, not what you charge customers. Every item entering inventory is recorded at its purchase or production cost, and that cost is tracked through to the point of sale, where it becomes cost of goods sold (COGS) on the income statement.

It’s worth taking a moment to clarify where cost accounting fits, since people often ask how it’s different from accounting more broadly. Accounting generally divides into four branches:

- Financial accounting (producing external financial statements)

- Managerial accounting (internal decision-support data)

- Tax accounting (compliance)

- Cost accounting (detailed cost tracking for pricing and profitability)

In retail and ecommerce, “cost accounting” is most often used to refer specifically to the cost-based methods for valuing inventory, which is what this article is about.

The practical distinction for a business owner comes down to scope. Financial accounting captures all activity, while cost accounting zooms in on the cost side, tracking what things cost to acquire, produce, and sell. For a CFO or controller, that distinction matters most when analyzing margins, setting prices, or determining what inventory is actually worth on any given day.

The four main inventory cost accounting methods

When accountants refer to the four types of cost accounting in the inventory context, they mean the four cost-based valuation methods that determine which cost gets matched to which sale.

1. FIFO (First In, First Out)

The FIFO method assumes that the oldest inventory is sold first. The cost of ending inventory reflects your most recent purchases, which in inflationary periods means a higher balance sheet figure and lower COGS. FIFO is the most commonly used method among U.S. retailers and ecommerce businesses, in part because it typically mirrors actual physical flow and is accepted under both GAAP and IFRS.

2. LIFO (Last In, First Out)

It assumes the most recently purchased items sell first. This tends to produce higher COGS and lower taxable income in inflationary environments, which makes it attractive for tax purposes. There is, however, a significant structural constraint: the LIFO conformity rule. Under IRS regulations, if a U.S. business elects LIFO for tax reporting, it must also use LIFO for its primary financial statements, and it can’t show FIFO results to investors while filing LIFO on its tax return.

That forces a real tradeoff: lower taxes today against a balance sheet where ending inventory reflects older, lower costs that can look significantly understated relative to current market values. LIFO is also not permitted under IFRS, which eliminates it for any business reporting under international standards or planning to do so.

3. Weighted average cost (WAC)

This method smooths out price fluctuations by dividing the total cost of goods available for sale by the total number of units available. Every unit carries the same average cost, which simplifies recordkeeping when goods are interchangeable – a popular approach for commodity-style products where distinguishing one purchase batch from another doesn’t make operational or financial sense.

4. Specific identification

The method of specific identification assigns the actual cost of each individual unit to the sale of that specific unit. It’s precise but only practical for low-volume, high-value inventory – jewellers, car dealerships, art galleries – where each item has a distinct cost that’s worth tracking individually.

Comparing the methods

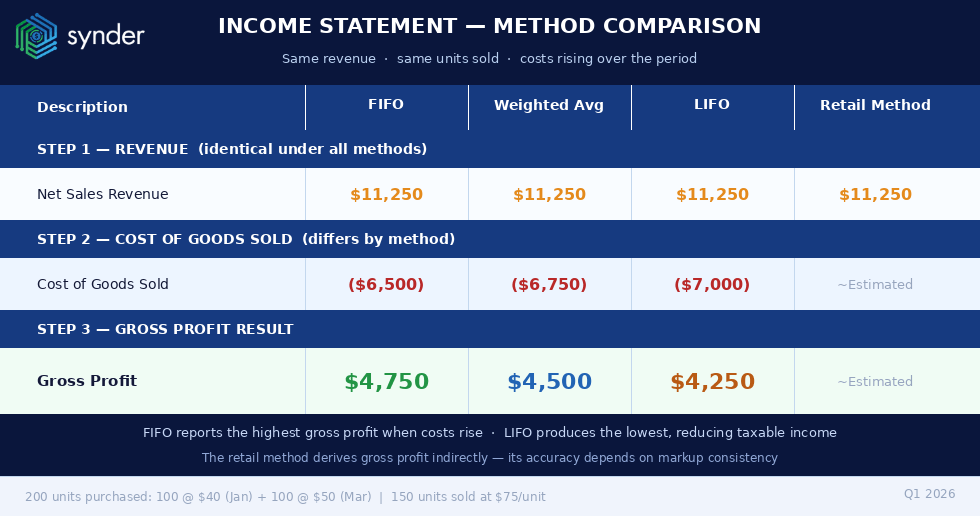

To make the difference between methods concrete, consider a business that buys 100 units in January at $40 each and another 100 units in March at $50 each. Then it sells 150 units at $75 each by quarter end, generating $11,250 in revenue under all methods.

FYI: Specific identification is intentionally excluded here as it’s only practical for individual high-value items tracked unit by unit.

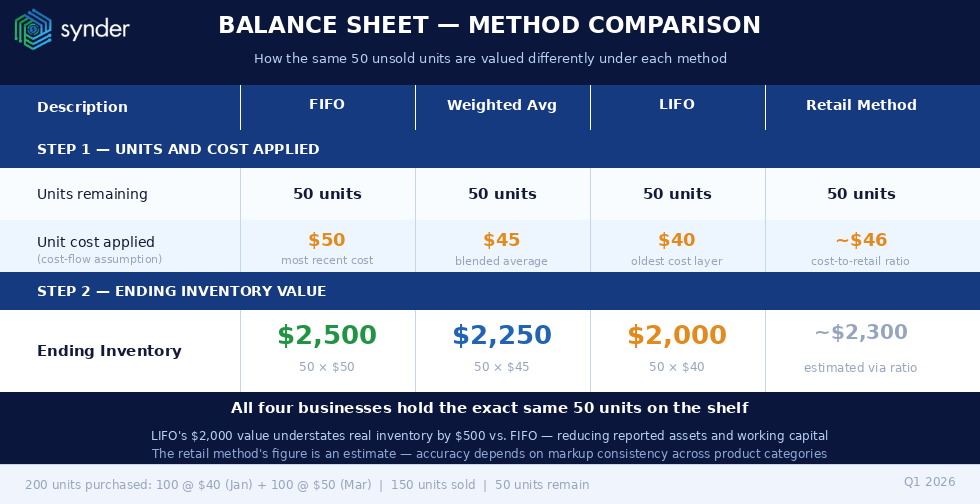

- Under FIFO, the first 100 units sold carry the January cost of $40, and the remaining 50 carry the March cost of $50. COGS = (100 × $40) + (50 × $50) = $6,500. Gross profit = $4,750. The 50 unsold units are valued at the most recent purchase price: ending inventory = 50 × $50 = $2,500.

- Under weighted average cost, total cost is (100 × $40) + (100 × $50) = $9,000 across 200 units, giving an average of $45 per unit. COGS = 150 × $45 = $6,750. Gross profit = $4,500. Ending inventory = 50 × $45 = $2,250.

- Under LIFO, the most recent 100 units at $50 sell first, and the remaining 50 come from the January batch at $40. COGS = (100 × $50) + (50 × $40) = $7,000. Gross profit = $4,250. Ending inventory = 50 × $40 = $2,000 – the lowest of the three, reflecting older, cheaper costs that understate what that stock is actually worth today.

| Note: In a period of rising costs, FIFO produces a lower COGS, a higher gross profit, and a higher inventory balance on the balance sheet. Weighted average cost lands between the two. LIFO produces the highest COGS and the lowest ending inventory value, which is why it’s attractive for tax purposes but can make the balance sheet look weaker than the business actually is. |

Retail accounting vs cost accounting: key differences

Both methods are GAAP-compliant and serve legitimate purposes. The right question is which fits your specific business model, product mix, and reporting requirements.

| Factor | Retail method | Cost method (FIFO / LIFO / WAC) |

| Basis of valuation | Retail selling price, converted via cost-to-retail ratio | Actual purchase or production cost |

| Precision | Estimate only | Exact, based on recorded costs |

| GAAP compliance | Yes (ASC 330) | Yes (ASC 330) |

| IFRS compliance | Yes | FIFO and WAC: yes; LIFO: no |

| Shrinkage accounted for? | No | No – requires separate adjustment |

| Inventory pooling required for accuracy? | Yes, for varied product mixes | Not applicable |

| Best for | High-volume, uniform-markup, multi-location retailers | Ecommerce, multi-channel, variable-markup businesses |

| Record-keeping complexity | Lower | Moderate to higher |

| Physical count required? | Recommended annually; method enables interim estimates | Recommended regularly |

| COGS accuracy | Approximate | Precise |

| Tax election constraint | None specific | LIFO: conformity rule applies |

| Software support | Major retail ERP and POS systems | QuickBooks, Xero, NetSuite, and most ERPs |

The starkest contrast is between precision and practicality.

- The retail method wins on speed and simplicity for businesses where counting physical inventory is genuinely difficult.

- Cost-based methods win on accuracy, especially when COGS tracking directly affects pricing decisions, investor reporting, or multi-channel margin analysis.

Which method is right for your business?

The retail inventory method tends to make sense for brick-and-mortar retailers with large, similar product assortments, consistent markup percentages across categories, and limited technology infrastructure for item-level cost tracking.

A single-format grocery chain, a chain of gift shops, or a department store with stable, category-level markup pools can apply RIM effectively because the cost-to-retail ratio stays reasonably stable across the inventory pool.

| Note: The retail inventory method should not replace periodic physical counts; it works as a fast estimate within a broader inventory management strategy, not as a standalone approach. |

Cost-based accounting is almost always the better fit for ecommerce businesses, multi-channel sellers, and any retailer where margins vary significantly by product or channel. Based on conversations with hundreds of our ecommerce and retail businesses, we know that COGS accuracy is one of the top financial reporting challenges, and the retail method doesn’t resolve it, it side-steps it.

A few practical signals that point toward cost accounting:

- Selling across multiple platforms at different price points

- Carrying product bundles where component costs need separate tracking

- Having significant variation in markup between product lines

- Needing GAAP-compliant margin reporting for investors or lenders

| Note: The retail method comes from a time when manually counting inventory was the main challenge. With modern systems in place, that limitation is largely gone for businesses that set them up properly. |

Perpetual vs periodic inventory systems

Actually, the choice of the method also interacts with something more fundamental: how often you update your inventory records. There are two approaches, and the distinction matters directly when evaluating whether the retail method or a cost method is practical for your business.

A periodic system updates inventory records at fixed intervals: monthly, quarterly, or annually. You count what’s left, calculate what must have sold, and derive COGS as the residual. The retail inventory method was designed for this environment. Without real-time cost tracking, estimating inventory via a cost-to-retail ratio was genuinely the most practical option available.

A perpetual system updates inventory in real time with every transaction – every purchase, sale, and return adjusts the running balance immediately. This is how modern ecommerce platforms and accounting integrations operate by default. When a Shopify sale syncs into QuickBooks, the item quantity decrements and COGS posts automatically.

Perpetual tracking has made cost-based accounting significantly more practical than it was a generation ago, and it’s a large part of why the retail method’s original efficiency advantage has narrowed considerably for online sellers. For any business running a modern ecommerce stack, perpetual tracking is almost certainly already in place, which means FIFO or weighted average cost is accessible without meaningful additional effort.

How the method choice flows through your financial statements

Accounting method decisions aren’t confined to the inventory line on the balance sheet. They ripple through the income statement (P&L statement), affect gross margin reporting, and in some cases change how a business looks to lenders or investors, even when the underlying operations are identical.

Effect on the income statement

The most direct impact lands on COGS and gross profit. Because each method assigns a different cost to each unit sold, the same physical sales volume produces different gross margin figures depending on which method you use.

In a period of rising costs, which describes most inflationary environments:

The retail method derives COGS indirectly – as goods available for sale at cost minus estimated ending inventory at cost – which means its COGS figure carries the same imprecision as the inventory estimate itself.

FIFO expenses the oldest, cheapest inventory first, keeping COGS lower and gross profit higher.

Weighted average cost smooths the impact, landing between FIFO and LIFO on both lines.

LIFO expenses the most recent, costlier inventory first, raising COGS and compressing gross margins, which reduces taxable income but makes the business look less profitable on paper.

Effect on the balance sheet

The balance sheet effect mirrors the income statement. Because the units that sell determine COGS, the units that remain determine ending inventory, and these two figures are always two sides of the same calculation.

In a period of rising costs:

The retail method values ending inventory at an estimated cost derived from the cost-to-retail ratio, approximate by design, and only as reliable as the consistency of your markup across product categories

FIFO carries ending inventory at the most recent purchase costs, producing a higher inventory value and stronger current assets on the balance sheet

Weighted average cost blends all purchase prices into a single per-unit figure, landing between FIFO and LIFO on reported asset value

LIFO carries ending inventory at the oldest, cheapest costs, sometimes reflecting prices from years or even decades ago, a phenomenon known as LIFO layers. A LIFO company and a FIFO company holding identical physical stock can show meaningfully different asset positions, not because the businesses are different, but because of the cost-flow assumption applied

Implications for financing and acquisition

For businesses seeking external financing or preparing for an acquisition, these distinctions are not academic. Here’s what changes depending on who’s reading your financial statements:

- Lenders evaluating working capital use inventory as part of their collateral and liquidity assessment – understated inventory under LIFO can reduce borrowing capacity even when physical stock is healthy

- Acquirers will adjust for method differences in due diligence, but a LIFO balance sheet requires more explanation and restatement work

- Investors comparing gross margins across companies need to know which method each uses before the comparison is meaningful

Switching methods mid-stream, say, from LIFO to FIFO ahead of a fundraise, is possible but requires IRS approval, prospective application, and disclosure in the financial statements. The method you choose today tends to have a longer shelf life than it might initially appear.

Keeping inventory accounting accurate across sales channels

Whichever method you choose, accuracy depends on the quality of your data. The retail method needs complete records of all goods received at cost and retail prices, all markups and markdowns applied, and all net sales across every channel and location. Cost-based methods need the purchase cost of every item mapped correctly to COGS as it’s sold, with returns and refunds handled consistently.

For single-channel businesses with one platform and one accounting system, that’s manageable without much automation. For businesses selling across Shopify, Amazon, eBay, and a brick-and-mortar POS simultaneously, the manual reconciliation becomes both the bottleneck and the source of error. Based on our experience working with multi-channel retailers, reconciliation across platforms is consistently the most time-consuming part of the month-end close, and discrepancies between what sales channels report and what the books show are common.

One multi-channel ecommerce business‘s CFO described the pre-automation situation directly:

Before, I would have had to hire additional staff at a cost of $5,000–$6,000 a month to help me operate the accounting department. By cutting out data entry, we’re saving on labor costs while improving efficiency by removing the errors.

Andy Pozniak

CFO at Dermeleve

That’s a $60,000+ annual impact from eliminating the manual matching work that multi-channel cost accounting otherwise requires.

Business tip: One approach to closing that gap is automation tools that sync transaction-level data, including sales, returns, and fees, directly into accounting software, thus tracking COGS in real time. For this purpose you might consider using Synder – an accounting automation tool that connects 30+ ecommerce and payment platforms to QuickBooks, Xero, NetSuite, Sage Intacct, and Puzzle, automatically tracking COGS against item-level costs as transactions flow through. For a multi-channel retailer tracking inventory under FIFO or weighted average cost, that kind of real-time sync removes the manual matching work that typically makes cost accounting harder to sustain at scale. If you want to see how that works in practice, you can book a demo with Synder.

Retail accounting vs cost accounting: what to take away

Both methods exist because neither is universally superior. The retail inventory method solves a real problem, estimating inventory value quickly when physical counting is impractical, and it does so in a GAAP-compliant way that’s served large-format retailers for decades. But its accuracy depends on stable, uniform markups; its COGS figure is approximate by design; and it leaves shrinkage entirely unaccounted for.

Cost accounting methods – FIFO, LIFO, weighted average cost, specific identification – demand more recordkeeping but return precise COGS figures, reliable profit margins, and financial statements that hold up under audit and investor scrutiny. For most ecommerce and multi-channel retail operations today, cost-based inventory accounting is both the more accurate and the more practical choice, particularly as accounting software and real-time perpetual tracking have made item-level cost accounting routine rather than burdensome. The question worth asking today is which one will give your business the financial visibility it needs as it grows.

FAQ

Can a business switch from the retail method to cost accounting?

Yes, but the switch requires IRS approval in the United States and must be applied consistently going forward. The change typically needs to be disclosed in the financial statements for the year of transition. If the switch has tax implications (for example, moving from LIFO to FIFO in a year with significant inventory build-up), the impact on taxable income needs to be carefully modelled before filing. Working with a CPA to manage the transition is advisable.

Does the retail inventory method work for ecommerce businesses?

It can, but with significant limitations. Ecommerce businesses typically sell across multiple channels at different price points, which creates variable markups that undermine the accuracy of a single cost-to-retail ratio. Most ecommerce accounting setups default to FIFO or weighted average cost tracked at the item level, because modern platforms and accounting integrations make cost-based tracking feasible without significant manual overhead. The perpetual inventory systems used by Shopify, Amazon, and similar platforms are built for cost-method accounting, not RIM estimates.

What are the four types of cost accounting?

In the broadest sense, the four branches of accounting are financial accounting, managerial accounting, tax accounting, and cost accounting. In the inventory-specific context, which is what most retailers and ecommerce businesses mean when comparing methods, the four cost-based inventory valuation methods are FIFO (First In, First Out), LIFO (Last In, First Out), weighted average cost, and specific identification. Each produces different COGS and ending inventory figures and has different implications for financial statements and tax reporting.

How does markup percentage affect the retail method’s accuracy?

The retail method assumes a reasonably consistent markup across the entire inventory pool, or across defined sub-pools if the business has segmented its inventory by category. When markup percentages vary widely between product types (from 30% on electronics to 80% on accessories, for example), the blended ratio produces inaccurate results for both. Businesses with highly variable markups should either segment inventory into pools by markup range, as large department stores do, or consider switching to a cost-based method. The wider the variance, the less reliable the retail method’s estimates become.

What happens to COGS under the retail accounting method?

Under the retail method, COGS is calculated as goods available for sale at cost minus estimated ending inventory at cost. It’s a derived figure, not a direct record of what each item cost. This makes it less precise than COGS calculated under FIFO or weighted average cost, where each sale is matched to its specific or averaged acquisition cost. For financial reporting that requires accurate gross margin data by product or channel, cost-based COGS is significantly more reliable. And for businesses where margin analysis drives pricing or purchasing decisions, the imprecision of the retail method’s COGS can translate directly into poor decisions.