Direct-to-consumer ecommerce is the model in which a brand sells its products directly to consumers through its own website or app, without a wholesaler, retailer, or marketplace in the middle. The brand controls the storefront, customer data, pricing, and the post-purchase experience, and it absorbs the costs and risks that traditionally sat with retailers.

This article is written for brand owners running DTC businesses on Shopify or their own website, and for the controllers, CFOs, and accountants who keep their books. You’ll learn what DTC is in 2026, how the economics work, where the model is winning and hurting, and how to run the bookkeeping behind it so your margins on paper match your margins in the bank account.

TL;DR

- DTC means owning the customer relationship: Brands control checkout, data, fulfillment, and retention instead of relying on retailers.

- DTC is now one channel, not the whole strategy: Growth has stabilized, and most brands combine DTC with wholesale and marketplaces.

- Profitability depends on unit economics, not growth alone: Rising CAC, higher returns, and research-heavy shoppers make margins harder to sustain.

- Operational complexity increases quickly with scale: Multi-channel sales, returns, and payments require structured data and accurate accounting.

- Clean financial data is a competitive advantage: Brands that automate accounting and track margins by channel make faster, better decisions.

What is DTC ecommerce in 2026?

DTC, short for direct-to-consumer (sometimes written D2C), describes a business that owns the relationship with its end buyer. Instead of selling wholesale to a retailer who then sells to a shopper, the brand runs its own checkout, ships its own orders, handles its own returns, and keeps its own customer list.

The model became famous through digitally native brands like Warby Parker, Casper, Allbirds, and Glossier in the 2010s, and it’s now used by everyone from established CPG companies running their own .com sites to single-founder Shopify stores selling skincare out of a garage.

What separates DTC from basic ecommerce is the relationship layer:

- Selling on Amazon is ecommerce, but the brand doesn’t own the customer, the data, or the unboxing moment.

- Selling through your own Shopify site to someone you can email next week is DTC.

| The same brand can do both, and most of the bigger ones now do, but the unit economics of each channel look very different on the P&L. |

How the DTC model works: a simple walkthrough

A DTC brand earns its margin by removing the wholesale and retail markups between manufacturing and the shopper, then spending part of the saved margin on customer acquisition.

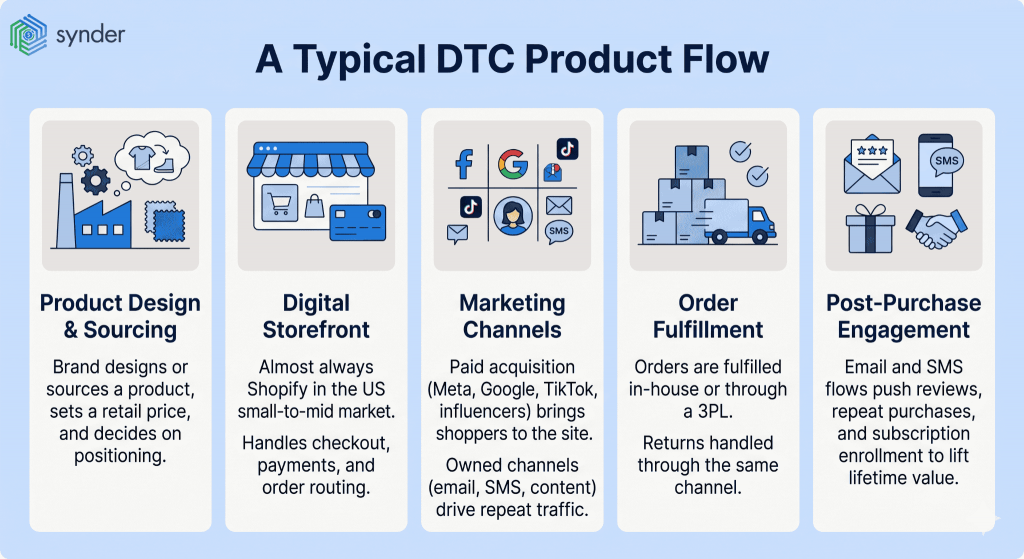

A typical product flow looks like this:

- The brand designs or sources a product, sets a retail price, and decides on positioning.

- A storefront, almost always Shopify in the US small-to-mid market, handles checkout, payments, and order routing.

- Paid acquisition (Meta, Google, TikTok, influencers) and owned channels (email, SMS, organic content) bring shoppers to the site.

- Orders are fulfilled either in-house or through a 3PL, with returns handled through the same channel.

- Post-purchase, email and SMS flows push reviews, repeat purchases, and subscription enrollment to lift lifetime value.

The reason the model is attractive on paper is the margin gap. Selling a $40 product wholesale at a 50% markup gives a retailer the markup, and selling the same product DTC and spending part of that markup on advertising and shipping leaves the brand with the customer email, the data on what they bought, and what’s left of the margin.

| This gap, multiplied across millions of orders and multiplied by repeat purchases, is the whole DTC thesis. |

Check out our article on the ecommerce business life cycle.

The state of DTC in 2026

The DTC category went through a boom, a correction, and a normalization in roughly five years. US DTC ecommerce sales reached $212.9 billion in 2025, a 16.6% jump from 2024, and now represent 19.2% of total US retail ecommerce. But the share figure has stayed roughly flat for two years running and is forecast to remain near that level through 2028, which tells a different story than the dollar growth alone.

The signal here is that DTC is no longer growing faster than ecommerce overall, and the framing has shifted from “DTC as a business model identity” to “DTC as one strategic channel inside a diversified commerce mix.”

The first-wave DTC brands that didn’t make it or had to change

Some well-known DTC names from the first wave have since pivoted to wholesale, opened physical stores, sold to a strategic acquirer, or delisted.

Allbirds and Glossier moved into Nordstrom, Sephora, and Target after years of online-only positioning. Warby Parker now operates more than 270 physical stores in addition to its website. Casper went public in 2020 and was taken private again in 2021 at a fraction of its IPO valuation. Dollar Shave Club was sold to Unilever, Bonobos to Walmart (and later resold), and Blue Apron was acquired for pennies on its original public offering. And the brands that survived largely did so by treating direct-to-consumer as one channel among several rather than the whole business.

What’s changing in DTC right now

A few shifts are reshaping how DTC brands operate, and they’re worth understanding even if your business isn’t ready to act on all of them yet.

- AI is now baseline, not edge. According to a State of AI in DTC Marketing 2025 survey of more than 875 DTC operators by DirectToConsumer.co and Triple Whale, 93% of DTC brands already use AI somewhere in their operations, and over 83% plan to expand their AI use in the next 12 months. The use cases range from creative generation and copywriting to customer service automation, demand forecasting, and bookkeeping. The question for most brand owners is where to deploy AI first.

- Owned channels are eating paid budgets. As Meta and Google CPMs climb, more DTC brands are shifting marginal dollars toward email, SMS, loyalty, and content. The math is: a customer email costs almost nothing to send and converts at a far higher rate than a cold ad impression.

- Physical retail is back on the table. Several of the original DTC brands have opened stores, partnered with retailers, or both. Physical presence acts as a billboard, builds trust with shoppers who want to see the product before they buy, and reduces dependence on paid acquisition. For brand owners on Shopify, this often means handling in-person sales through Shopify POS, which adds another layer of accounting complexity.

- Subscription and replenishment models are winning in consumable categories. For supplements, skincare, pet food, and coffee, converting a one-time buyer into a subscriber transforms the unit economics. It means that CAC is paid once, and revenue increases.

The real advantages of DTC

The reason brand owners keep choosing the DTC route, even after the corrections of the past few years, is that the model delivers things wholesale simply can’t. The advantages are real, they’re just no longer automatic.

- Margin control: Owning the channel means owning the price. Brands set their own discounting calendar, decide which products to lead with, and capture the full retail margin instead of splitting it with a retailer. For categories with strong gross margins, like apparel, supplements, and beauty, this can be the difference between a viable business and a break-even one.

- Customer data and relationships: Every DTC order produces an email, a shipping address, a product preference, and a purchase history that lives in the brand’s systems, not a retailer’s. That data drives email flows, lookalike audiences, product development, and retention programs. In a world where third-party tracking has been cut down, first-party data is what makes paid media still work.

- Speed of iteration: A wholesale brand has to convince a buyer at a retailer to take a new SKU, then wait for the next planogram reset. A DTC brand can launch a new variant on Tuesday, A/B test the landing page on Wednesday, and have weekly sales data by Friday, and the tempo increases. Brands that move quickly on consumer signals tend to outgrow brands that don’t.

- Brand storytelling and customer experience: The DTC brands that survived the shakeout largely did so because the storefront was a real brand experience, not a checkout.

As Suze Dowling, Co-Founder and Chief Business Officer at Pattern Brands, wrote on LinkedIn:

If I were starting a DTC brand from scratch today, here’s what I wouldn’t do: I wouldn’t start with a logo. I wouldn’t start with a paid ads plan. I wouldn’t start with a 50-page pitch deck. I’d start with a problem. A real one. Because the brands that break through today aren’t just selling products. They’re solving urgent, emotional pain points customers already feel. You don’t create demand. You uncover it.

As Suze Dowling, Co-Founder and Chief Business Officer at Pattern Brands

This matters for the bookkeeping side too. Brands built around a clear customer problem tend to have stronger retention, lower refund rates, and more predictable cash flow, which translates into cleaner books and easier closes. The brands that struggle financially almost always struggle on the customer side first.

Where DTC brands lose money

The DTC graveyard is full of brands that had a great product, a great founder, and a great Instagram presence, and still ran out of money. The reasons cluster into a few patterns:

- Customer acquisition cost: Customer acquisition costs have climbed roughly 60% over the past five years, with the average ecommerce CAC now hovering around $70 per customer. That means a brand selling a sub-$70 product can lose money on the first sale and only recover it through repeat purchases. According to Digiday and Klaviyo’s State of DTC Marketing 2025 survey, 63% of DTC brands now rank CAC as a top KPI, which is why retention tools like email, SMS, subscriptions, and loyalty programs have moved from optional to load-bearing.

- Returns and refunds: Online return rates have more than doubled since 2019, climbing from 8.1% to about 16.9%, and the cost of processing a return runs from 20% to 65% of the item’s original value once shipping, restocking, customer service, and occasional write-offs are counted. For apparel and footwear brands, where bracketing (ordering multiple sizes intending to send some back) is common, the effective cost of every “sale” is lower than the gross number suggests. If refunds and chargebacks aren’t categorized correctly in the books, gross sales look healthy while net revenue bleeds.

- Shoppers research more before they buy: 92% of Gen Z shoppers now research before buying, and this is the highest rate of any generation. It means even the orders that do convert have already been compared against three competitors, so weak differentiation translates directly into wasted ad spend.

- Channel concentration risk: A DTC brand that relies heavily on Meta ads for traffic can feel the impact of a single algorithm shift or policy update almost immediately. This kind of vulnerability became clear with App Tracking Transparency in 2021, when targeting and attribution changed overnight for brands built around Facebook acquisition. The same pattern applies to any single source, whether it is one influencer, one TikTok spike, or one referral partner, which is why more mature DTC operators spread acquisition across channels to stay resilient.

- Operational complexity: A brand doing 100 orders a month can run on a founder’s laptop and a Shopify dashboard. A brand doing 5,000 orders a month across Shopify, a 3PL, a payment processor, and a customer support tool, with returns coming in daily and ad spend running across three platforms, cannot. Manual data handling that was annoying at low volume becomes a real constraint on growth, especially in finance and accounting, where reconciliation backlogs delay the close and obscure the numbers leadership needs to make decisions.

What the data says about DTC today: a quick overview

A useful way to read the market is to compare what’s growing against what’s flattening:

| Factor | The trend | What it means for brand owners |

| US D2C sales | Growing in absolute dollars, but share of total retail ecommerce has flattened | Category is large and stable; the easy growth window has closed |

| Customer acquisition cost | Climbing steadily across every major paid channel | Margin per order has to absorb more marketing cost, or retention has to do the work |

| Return rates | Rising sharply, especially in apparel and footwear | Refund and chargeback handling is now a meaningful line on the P&L |

| Channel mix | Most large DTC brands now sell wholesale, marketplace, and retail alongside .com | Pure-DTC is rare at scale; multi-channel accounting is the norm |

| First-party data | Treated as the most important growth lever by the majority of DTC brands | Owned customer relationships are the asset; the storefront is the wrapper |

| AI adoption | Now baseline across most DTC operations, with expansion planned in the next year | Brands that don’t adopt AI in marketing, ops, or bookkeeping fall behind on cost and speed |

DTC versus wholesale, marketplace, and retail: choosing your channel mix

A useful way to think about DTC in 2026 is not “DTC versus everything else” but “what role does DTC play in our channel portfolio?” Each channel has a different economic profile, and the right mix depends on the category, the margin structure, and the stage of the business.

Wholesale and retail give a brand reach, third-party validation, and access to shoppers who don’t live on Instagram, but they take a margin cut and a layer of customer data. Marketplaces like Amazon offer enormous demand and built-in trust, but they squeeze margins through fees and treat the brand as a commodity. DTC gives the brand control, data, and full margin, but the brand has to find every customer itself and cover the cost of doing so.

| Most successful brands settle into a hybrid: DTC as the brand-defining flagship channel where new launches happen first and customer data lives, plus selective wholesale or marketplace presence to capture demand the brand can’t reach on its own. The accounting setup has to handle that mix from day one, because here brand owners might run into trouble. |

What DTC brand owners need to track financially

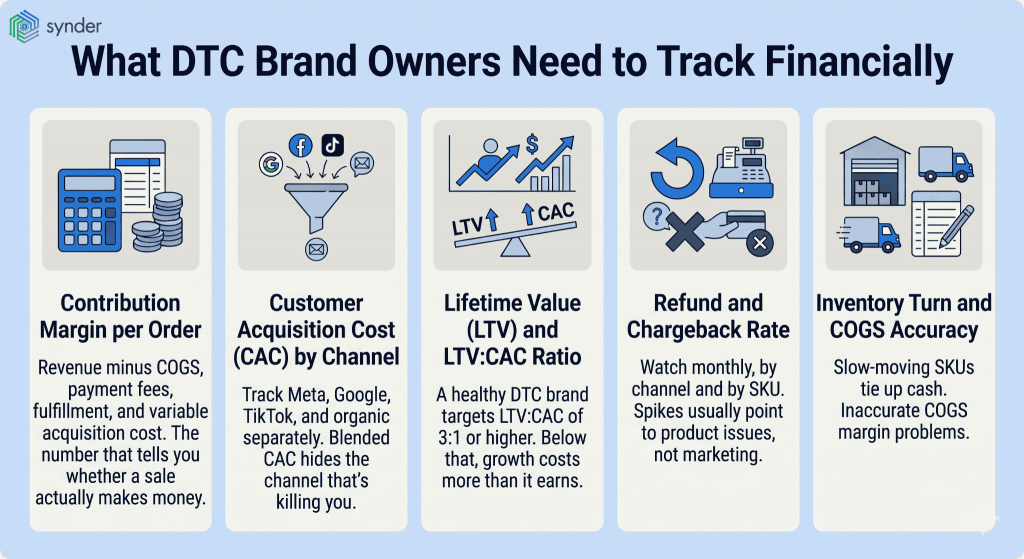

The financial picture of a DTC business is more complicated than it looks. The numbers below matter most, the ones a controller or CFO should be able to pull on demand without waiting for month-end:

- Contribution margin per order. Revenue minus COGS, payment fees, fulfillment, and variable acquisition cost. This is the number that tells you whether a sale actually makes money.

- Customer acquisition cost (CAC) by channel. Track Meta, Google, TikTok, and organic separately. Blended CAC hides the channel that’s killing you.

- Lifetime value (LTV) and LTV:CAC ratio. A healthy DTC brand generally targets LTV:CAC of 3:1 or higher; below that, and growth costs more than it earns.

- Refund and chargeback rate. Watch this monthly, by channel and by SKU. Spikes usually point to product issues, not marketing.

- Inventory turn and COGS accuracy. Slow-moving SKUs tie up cash. Inaccurate COGS hides margin problems.

Learn about how to build an ecommerce tech stack.

How brand owners are simplifying the back office

The DTC operators who are still profitable in 2026 generally have one thing in common: they don’t let manual bookkeeping become the bottleneck. Reconciling Shopify, Stripe, PayPal, and the bank account by hand is workable at low volume and impossible at scale. The brands that scale cleanly automate the data flow into their accounting system early, so the books match the platforms in real time, and the close happens in days rather than weeks.

This is where tools like Synder fit into the DTC stack. Synder is an accounting automation platform that syncs ecommerce and payment data across 30+ platforms into QuickBooks Online, Xero, NetSuite, Sage Intacct, and other accounting systems. Its job is to pull every transaction, fee, refund, and payout from Shopify and the payment processors into the accounting system with the right categorization, so the controller isn’t rebuilding the P&L from CSV exports every month.

A practical example: an ecommerce retailer selling sleep and wellness products through Shopify and a brick-and-mortar location, called SleepEh, was managing duplicate SKUs across both channels and reconciling Shopify sales against QuickBooks by hand. After automating the sync between Shopify, QuickBooks Online, PayPal, and Affirm with Synder, the team cut 2–3 hours per week of manual data entry, eliminated duplicate SKUs from the books, and reached 100% accuracy on Shopify-to-QuickBooks syncing. That saved roughly 12–18 full workdays per year, which is real time the operations team got back for customer service and growth work.

| The point is that brand owners running multi-channel DTC operations need a clean pipeline from their selling platforms into their books, and the brands that figure that out early tend to make better decisions because they have better numbers. |

If you want to see how this works for a specific setup, you can book a demo with Synder.

Conclusions on DTC ecommerce in 2026

DTC ecommerce isn’t a golden ticket, and it isn’t a dying category. It’s a mature, ~$240 billion channel inside a much larger retail economy, and the brands that win in it now do so on the strength of their unit economics, their customer relationships, and their operational discipline. The dogma that built the original DTC era – that brands should sell only direct, that paid social was infinite, that growth-at-all-costs was a strategy – has been replaced by something more workable: DTC as one channel in a smart portfolio, retention as the engine of profitability, and owned data as the long-term asset.

For brand owners, the practical takeaway is that the back office matters as much as the storefront. Strong DTC brands have clean books, accurate margins by SKU and channel, and reconciliation processes that don’t fall over at scale. The ones that don’t tend to discover their problems too late. Get the unit economics right, get the data flow into accounting right, and the rest of the strategy has somewhere solid to stand on.

FAQ

Is DTC profitable for brand owners today?

DTC can be very profitable, but profitability is no longer automatic the way it felt in the late 2010s. Brands with strong contribution margins, disciplined acquisition spend, and meaningful retention generally make money. Brands relying on paid social alone, with thin margins and low repeat-purchase rates, tend to struggle. The math is the answer.

What does a DTC ecommerce business actually need to succeed?

The reliable list is a clearly differentiated product, an honest understanding of CAC and LTV by channel, an owned-channel strategy (email, SMS, content) that doesn’t depend on paid social, clean fulfillment and returns operations, and an accounting setup that produces accurate margins by SKU and channel without weeks of manual work.

How does DTC accounting differ from regular ecommerce accounting?

It’s similar in shape but heavier on platform-level detail. A DTC brand typically needs payout-level reconciliation between Shopify, Stripe, or PayPal and the bank, fee categorization that separates payment processing from advertising and fulfillment, multicurrency handling for cross-border sales, sales tax breakouts by state for nexus compliance, and clean refund and chargeback tracking. Most general accounting setups don’t handle this natively, which is why brands at scale automate the sync.

Is Amazon considered DTC?

Selling through Amazon is generally not considered direct-to-consumer in the strict sense because Amazon owns the customer relationship, the data, and the experience. The brand is a vendor on a marketplace. Many brands sell on Amazon and DTC simultaneously, but the two channels have very different economics and should be tracked separately on the P&L.