The short answer is no, AI isn’t going to replace accountants, but it’s already replacing a chunk of the work accountants used to do by hand. The U.S. Bureau of Labor Statistics projects 5% employment growth for accountants and auditors from 2024 to 2034, with about 124,200 openings each year, faster than the average across all occupations. So the job is growing, but the daily work is being rebuilt around automation.

This change matters most to working accountants and CPAs worried about job security, students and career-changers weighing whether the profession still pays off, and small firm owners deciding how much to spend on AI tools. The article tells you about which tasks AI now handles, which still need a human, what CPAs should expect over the next five years, and what the changes look like inside retail, ecommerce, and SaaS teams.

TL;DR

- AI won’t replace accountants, but it will change the job: The profession stays, but daily work shifts away from routine tasks toward judgment, review, and client-facing work.

- Demand for accountants remains strong: Fewer professional graduates and a shrinking workforce, combined with licensing requirements, keep CPAs in demand and protect the value of the credential.

- AI already handles routine work well: Data extraction, categorization, reconciliation, and drafting are increasingly automated, saving time and speeding up processes like the close.

- Human judgment is still essential: AI can’t sign audits, make final tax decisions, or handle complex edge cases, which keeps accountants central to the process.

- The role is shifting toward advisory: As routine work declines, accountants who focus on strategy, analysis, and client communication will see the most value in the next phase of the profession.

How AI is changing accounting today

Inside accounting workflows, AI is doing four things reliably:

- Extracting data from documents

- Categorizing transactions

- Matching records across systems

- Drafting first-pass summaries

McKinsey’s State of AI report shows enterprise AI adoption climbing from 78% in early 2025 to 88% by late 2025, with finance and accounting among the fastest-growing functional use cases.

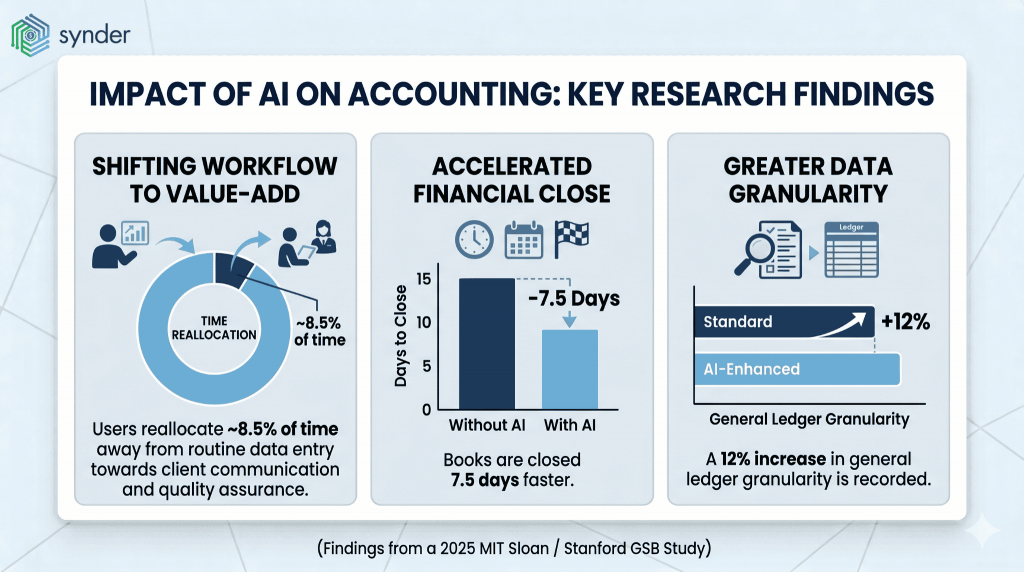

A 2025 MIT Sloan / Stanford GSB study by Choi and Xie ran the numbers on what that adoption actually produces inside the work. Surveying 277 accountants and analyzing transactions from 79 small and mid-sized firms, the researchers found that AI users:

- Recorded a 12% increase in general ledger granularity

- Reallocated about 8.5% of their time away from routine data entry toward client communication and quality assurance

- Closed the books 7.5 days faster

The most useful finding for the “will AI replace accountants” question is what the study calls the experience effect: senior accountants gained materially more from AI than juniors because they knew when to trust the output and when to override it. AI in accounting works best as a collaborator with someone who already understands the work.

What AI can’t do

What AI still can’t do well is stand behind numbers. AI can draft a tax position but can’t sign a return. The technology flags audit anomalies but can’t cross-examine a client about them. Software summarizes contracts but can’t negotiate revenue recognition treatment with an auditor.

The current generation of accounting AI is also weak on edge cases:

- Unusual ownership structures

- Multi-jurisdiction tax interactions

- Ecommerce platforms with non-standard fee deductions

A human accountant catches these situations through experience, while an AI recognizes them only when similar patterns exist in its training data.

| What AI handles reliably today | What still needs a human |

| Bank feed categorization and rule-based coding | Final tax position decisions and return sign-off |

| Document OCR for invoices, receipts, and statements | Audit opinion and professional skepticism |

| Three-way matching of POs, invoices, and receipts | Revenue recognition judgment under ASC 606 / IFRS 15 |

| Reconciliation between source platforms and the GL | Investigating unusual transactions and fraud red flags |

| Anomaly detection on expense patterns | Client conversations about risk tolerance and structure |

| Drafting variance commentary and management reports | Negotiating with auditors, lenders, or tax authorities |

| Routine accounts receivable follow-up and dunning | Cash strategy, FP&A scenario modeling for the board |

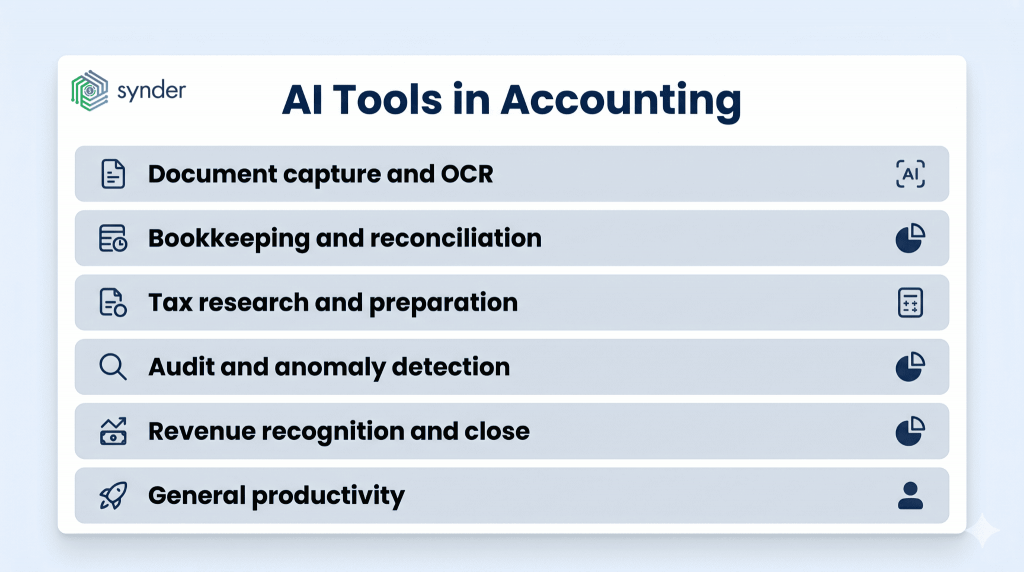

Where AI tools fit by function

The AI accounting market has organized itself into roughly six functional categories. Most finance teams pick one tool per category rather than a single platform that covers everything:

- Document capture and OCR. Tools that read receipts, invoices, and contracts and push extracted data into the ledger. Common examples include Dext and Vic.ai.

- Bookkeeping and reconciliation. Tools that categorize transactions, reconcile accounts, and flag exceptions. This category includes both general-purpose tools and platform-specific reconciliation tools for ecommerce and SaaS.

- Tax research and preparation. AI assistants that search tax codes, return cited answers, and draft returns for review. CoCounsel Tax, TaxGPT, and Bloomberg Tax Answers fall in this category.

- Audit and anomaly detection. Tools that scan complete transaction sets rather than samples to catch fraud and unusual patterns. MindBridge and DataSnipper are typical.

- Revenue recognition and close. Tools that handle ASC 606 schedules, deferred revenue, and month-end close steps. More relevant for SaaS finance teams.

- General productivity. ChatGPT, Microsoft Copilot, and similar assistants used for summarizing, drafting, and ad-hoc analysis across any workflow.

The right starting point is usually whichever category covers the workflow that costs the most hours per month, not whichever tool is loudest in the market.

How AI works in retail, ecommerce, and SaaS finance

The way AI shows up in a finance team depends largely on the business model. Retail and ecommerce finance teams deal with high transaction volume across multiple sales channels, payment processors, and marketplaces. SaaS teams deal with lower volume but harder revenue recognition and deferred revenue tracking. The same AI capabilities apply differently in each environment.

The rollout sequence also looks different by industry. An ecommerce controller usually starts with multi-channel reconciliation, while a SaaS controller usually first gets down to deferred revenue tracking and subscription billing. Picking the workflow with the highest hours-per-month cost is a more reliable rollout strategy than chasing which AI feature is newest.

Retail and ecommerce: connective tissue between channels and the GL

In retail and ecommerce, the highest-value AI work is the connective tissue between sales channels and the general ledger. A finance team running Shopify, Amazon Seller Central, Stripe, PayPal, and Square in parallel typically processes thousands of transactions per month, each with platform-specific fees, refund flows, and tax treatment.

Working with ecommerce and retail teams, we start to see the same thing over and over. The biggest time drain each month is reconciling across channels. Once teams switch to AI-driven sync and categorization, that work drops from days to minutes, and they’re mostly just checking the few things that don’t line up.

Business tip: Instead of recreating reconciliation logic in spreadsheets or internal tools, they use AI-powered automation that knows how Shopify, Stripe, and PayPal behave and sends clean entries into the general ledger. Synder is a great example. It connects 30+ ecommerce and payment platforms to QuickBooks Online, Xero, NetSuite, Sage Intacct, and Intuit Enterprise Suite, handling multi-channel transaction data sync in the transaction-level or summary mode, depending on your volume.

If you want to see how Synder fits your business workflows, you can book a demo.

How likely is AI to replace accountants?

The probability that AI replaces the accounting profession outright is low, but it’s almost certain to redefine what an accountant spends their day doing. Two things drive that gap.

First, the accounting work is layered. A tax return, an audit opinion, or a board-level financial package depends on judgment calls, professional skepticism, and accountability that current AI models can’t own.

Second, the profession is shrinking on its own. The AICPA’s 2025 Trends Report counted 55,152 combined accounting bachelor’s and master’s graduates in the 2023–24 academic year, a 6.6% year-over-year decline, with bachelor’s degrees alone falling to 40,817 (down 3.3%). The pace of decline is easing slightly, but the pipeline of new accountants continues to narrow just as AI begins stepping in to absorb some of that gap.

What experts say

The sharpest version of the difference between replacing the role and replacing the routine tends to come from people who teach the next wave of accountants. Denise Probert, who teaches accounting at the University of Colorado Boulder’s Leeds School of Business, summed up the shift on LinkedIn:

AI isn’t here to take your seat – it’s here to clear the noise so you can focus on higher-value work… AI won’t replace you. But someone who uses it well might.

Denise Probert, CPA, CGMA, Teaching Assistant Professor of Accounting, Leeds School of Business, University of Colorado Boulder

What this means for our audience: A working accountant isn’t competing with AI, but with the colleague who’s quicker to adopt it and works faster as a result. A student or career-changer still sees a strong demand for accountants, especially in roles that require credentials and judgment. And for a small firm owner, the question has shifted from whether to invest in AI to how to introduce it step by step without overspending or disrupting the business.

From technician to strategist: the real shift in accounting

The biggest change in the profession is what gets promoted. As AI handles more of the technical bookkeeping and compliance pipework, the work that drives firm revenue is moving up the value chain to advisory. And it’s becoming the core profit engine for forward-looking firms.

That shift changes what “good work” looks like inside the firm. Junior staff used to learn the trade through repetitive bookkeeping and compliance volume; now that volume is the part most exposed to automation. The result is a faster path to advisory exposure for accountants who lean in, and a slower one for those who don’t.

What advisory means inside a modern firm

Advisory work is what’s left after AI takes the routine. It typically includes:

- Tax planning conversations and business-structure decisions

- Financial modeling for board meetings

- Risk assessments and scenario analysis

- Judgment calls that depend on client context and history

A senior accountant in this environment spends most of the day on client-facing strategy and review work, with AI handling the data prep underneath. The economics shift accordingly: advisory hours bill higher than compliance hours, and the firms moving fastest are repricing engagements around it.

Why not every firm should pivot to advisory

The technician-to-strategist arc is the dominant industry narrative, but it doesn’t fit every firm. Many clients want efficient, accurate compliance work, not strategic consulting, and pushing advisory on a tax-only client base usually backfires.

Solo practitioners and tax-only firms with stable, compliance-oriented clients can stay in their lane and use AI to widen margins instead of repositioning the practice. For these firms, the right question is not “How do I become a business advisor?” but “How do I use AI to deliver better value in my chosen area of tax expertise?”

Conclusions on whether AI will replace accountants and the future of accounting

The future of accounting is one where the profession survives, the credential gains value, and the day-to-day work changes more than it has in any decade since spreadsheets replaced ledger paper. AI isn’t coming for the role, but for the routine that filled the role, which sounds reassuring until you account for the fact that routine work is what trained the next generation of accountants. The pipeline question is the real strategic issue facing the profession over the next five years, and AI is part of the answer because it absorbs capacity that an under-supplied workforce can no longer cover.

For working accountants, students, and firm owners, the practical takeaway is the same: lean into the work AI can’t do. That’s judgment, advisory, communication, and domain depth. The firms and individuals who treat AI as a force multiplier on those capabilities will see the next five years as the best in the profession’s recent history. The ones who treat AI as a threat, or worse, ignore it, will find themselves competing on price for the work AI does best.

FAQ

Can you make $500,000 a year as an accountant?

Yes, but the path runs through specialization or ownership, not through a staff accountant title. Accountants’ pay in the U.S. is roughly $61,000 to $87,750, with senior accountants reaching $80,000 to $109,000. The $500,000 figure starts to appear at the partner level in CPA firms, in director-level FP&A or controllership roles at larger companies, and in specialized tax, audit, or M&A advisory practices.

What percentage of accounting tasks can AI realistically automate today?

Industry estimates put current AI automation of routine accounting work at roughly 40% to 60%, depending on tooling and client complexity. Compliance-heavy firms automate higher; advisory-heavy firms lower, because their work is already non-routine. Data quality and integration depth set the ceiling more than the AI itself does.

Which accounting jobs are most at risk from AI in the next five years?

Roles built mainly on data entry, transaction categorization, basic reconciliation, and routine accounts payable face the highest pressure, including some bookkeeping and entry-level staff accountant positions. Audit, tax advisory, controllership, FP&A, and industry-specialized accounting carry the lowest direct risk because they hinge on judgment AI cannot own.

How does AI change the way junior accountants learn the job?

Routine work that used to teach juniors the trade is the work AI absorbs first. That breaks the traditional training path, so firms are starting to redesign early-career roles around AI oversight: validating outputs, handling exceptions, and learning data flows across systems instead of producing the data manually. Mentorship and structured review get more important, not less.

How should a small accounting firm start adopting AI without overspending?

Start with the workflow that costs the most hours per month, which for most small firms is bank feed cleanup, transaction categorization, or multi-channel ecommerce reconciliation. Pilot one tool against that workflow, measure hours saved over 60 days, and reinvest the savings into either advisory training or senior hires before adding more tools. Tooling sprawl without a process change tends to add cost rather than reduce it.