If you’ve ever gotten paid via direct deposit or paid a bill online, you’ve probably used the ACH debit without even knowing it. ACH debit is a behind-the-scenes method of how we handle our money these days. This isn’t just some confusing financial jargon; it’s a part of our everyday money life.

In this article, we’re going to make all ACH debit transactions easy to understand. Ever wondered how your gym automatically charges your monthly membership fee? That’s ACH debit for you. We’re going to walk through what it is, the different ways it pops up in your day-to-day life, and how it stacks up against other ways you might be paying or getting paid. So, let’s get into the world of ACH debit – it’s simpler than you might think, and it’s everywhere in your financial world.

What is ACH debit?

ACH debit is a digital way to move money from one bank account to another without using paper checks, wire transfers, or cash. Imagine you’re setting up an automatic payment for your monthly gym membership. Instead of writing a check or paying in cash every month, you can authorize the gym to pull the money directly from your bank account on a set date. That’s ACH debit in action.

It works through a huge network called the Automated Clearing House (ACH). When you give permission, the gym sends a request through this network to your bank. Your bank then checks to make sure you have enough money and, if everything looks good, it sends the money over to the gym’s bank. This process usually takes 1- 3 business days.

In other words, ACH debit is an electronic, behind-the-scenes method that businesses, governments, and individuals use to move money around securely and automatically. It’s pretty handy for regular payments like bills, salaries, or your Netflix subscription because once it’s set up, the payments happen on their own without you having to do anything each time.

What is the difference between ACH debit and ACH credit payments?

Now that we know what ACH debit is, how does it compare to ACH credit transactions? Let’s have a look.

ACH debit transactions

This is when money is taken out of your bank account. When you’ve set up automatic bill payments for your utilities, each month, the utility company will ‘pull’ the amount you owe directly from your bank account.

ACH credit transactions

In contrast, ACH credit transactions happen when money is put into your bank account. Let’s say your employer pays you through direct deposit. Every payday, they ‘push’ your salary into your bank account. That’s an ACH credit. You’re receiving money, not sending it.

To sum it up, the main difference is about who initiates the transaction and the direction the money moves. In ACH debit, the receiver initiates the transaction to ‘pull’ money from your account. In ACH credit, the sender initiates the transaction to ‘push’ money into your (or someone else’s) account.

What is ACH Network?

When trying to understand how ACH debit transactions work we need to look closer at its components, namely ACH Network. This type of network is a massive, efficient system that banks and other financial institutions use to move money around electronically in the United States. When you make transactions like direct deposits of your paycheck, automatic bill payments, or transferring money to a friend, chances are they’re being processed through the ACH Network.

How does the ACH Network work?

The ACH Network is made up of thousands of banks and financial institutions. They all connect to this network, which is like a central hub for processing payments. When someone initiates a payment, like your employer sending your salary to your bank account, the ACH Network takes charge of moving that money from your employer’s bank account to yours.

The process is overseen by an organization called NACHA (National Automated Clearing House Association). They make sure that all these money transfers happen smoothly and set the rules for how the ACH Network operates.

One of the cool things about the ACH Network is that it batches payments together. Instead of sending each payment one by one, it gathers a bunch of transactions and processes them at specific times throughout the day. This makes the whole system more efficient and helps keep costs down.

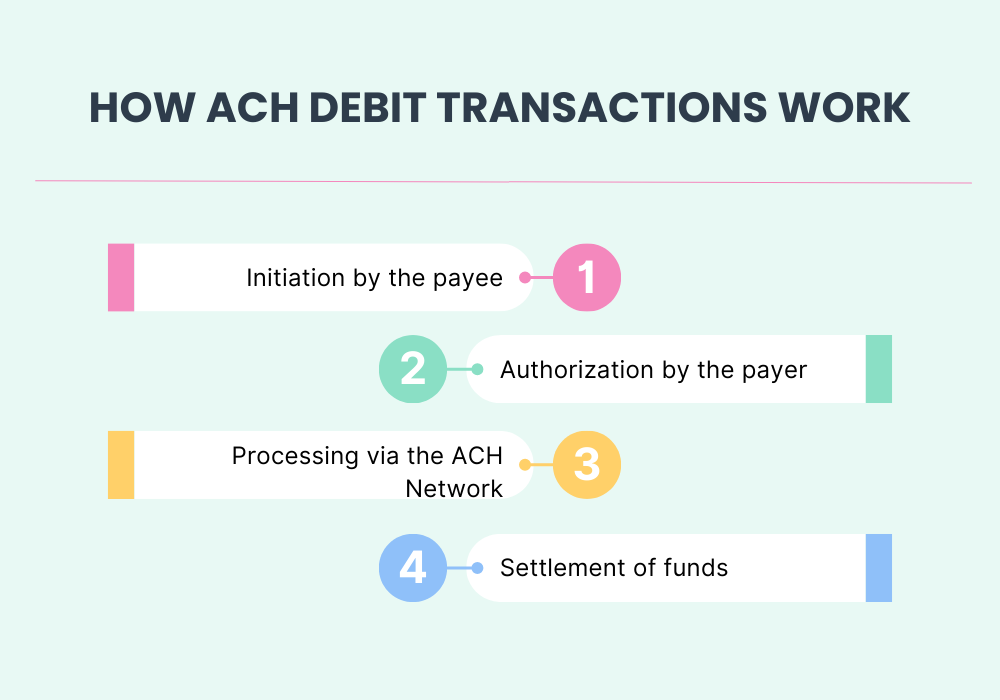

The process of ACH debit transactions

Let’s now take a quick journey through the steps of an ACH debit transaction, using a familiar example – paying your electricity bill. This process ensures your bill is paid securely and efficiently, without the need for cash or checks.

From the electric company requesting payment to your bank settling the funds, we’ll walk through each stage to see how your payment travels from your account to the electric company, all thanks to the marvels of the ACH Network. Let’s dive in!

Step 1. Initiation by the payee

This is where the whole process starts. The payee is the person or entity that wants to receive the money. For example, if you’re paying your electricity bill, the electric company is the payee. They start the transaction by asking to take the payment from your bank account.

Step 2. Authorization by the payer

You’re the payer in this scenario. Before the electric company can take the money from your account, they need your permission. This is what authorization is all about. You give your approval, usually when you sign up for automatic bill payments, providing them the green light to debit your account for the amount you owe.

Step 3. Processing through the ACH Network

After you’ve given your OK, the electric company sends a request through the ACH Network. Your bank receives this request and checks to make sure everything is in order, like ensuring you have enough funds in your account.

Step 4. Settlement of funds

This is the final step. Once everything checks out, your bank transfers the money to the electric company’s bank. This doesn’t happen instantly; it usually takes 1- 3 business days for the funds to move from one bank to another. But once it’s done, the transaction is complete. Your bill is paid, and the funds are successfully moved to the electric company.

Key takeaways

In summary, ACH debit transactions are a series of steps starting from the payee asking for money, you giving your permission, the banks processing this request through a specialized network, and finally, the money getting transferred. It’s a secure and efficient way to handle repetitive payments like bills.

Comparing ACH debit with other payment methods

ACH debit is excellent for routine, scheduled payments directly from your bank account, especially if you’re looking to avoid fees. However, there are other methods like credit cards, wire transfers, and digital wallets that have their own perks. We will now compare ACH debit with other common payment methods.

Wire transfers

Wire transfers are a bit like sending a package via express mail; they’re fast (usually within a day), can be international, but they also come with higher fees. They’re used for large, one-time transfers, like putting a down payment on a house. ACH debit, on the other hand, is more like standard mail. It’s great for regular, domestic transactions and usually doesn’t cost much (or anything), but it’s slower, typically taking a couple of days.

Electronic Funds Transfer (EFT)

EFT is an umbrella term that includes many types of electronic payments, including both ACH transfers and wire transfers. So, ACH debit is a type of EFT. The difference is mostly in the specific method used. For example, ACH is one way to do an EFT, and it’s mostly used for regular, recurring payments within the U.S. Other types of EFT, have different uses and features.

Digital wallets and online payment systems

Digital wallets and online payment systems (like PayPal or Apple Pay) provide you with a so-called virtual wallet. You can store card information, bank account details, or even load money into them. They’re super convenient for online shopping and quick transfers. ACH debit is more straightforward but less flexible. It lacks the instantaneity and the wide online shopping utility that digital wallets offer.

Credit cards

ACH debit involves directly taking money from your bank account (the money you actually have) while credit cards are more like a short-term loan. You use the card to pay for something, and then you pay the card issuer back later. Plus, credit cards often come with reward points, but also interest charges if you don’t pay back on time.

What are the different types of ACH transactions?

Each type of ACH transaction is designed to make transferring money easier, faster, and more secure, whether it’s for personal or business use. Banks use different transfers each with a specific job (and specific bank code) that helps keep your money life organized and running smoothly.

Prearranged Payment and Deposits (PPD)

Prearranged Payment and Deposits are used mostly for personal transactions. If your employer uses direct deposit to pay you, or if you have set up automatic bill payments for your utilities or mortgage, these transactions are likely classified as PPD. They involve a prior agreement between you and the party receiving or sending the funds.

Cash Concentration or Disbursement (CCD)

Primarily used for business-to-business transactions. For example, if a company is transferring funds to another company for services rendered or for supplier payments, this transaction is often categorized as CCD. It’s a way for businesses to manage their cash flow and payments efficiently.

Ready for flawless financials? Discover how Synder can revolutionize your business’s bookkeeping. With seamless integrations with top accounting software, Synder streamlines your financial processes, ensuring pinpoint accuracy and real-time insights. Say goodbye to manual errors and hello to effortless bookkeeping.

Internet-Initiated Entries (WEB)

These are transactions initiated online. If you’re paying a bill on a company’s website, or making an online transfer from your account, it’s typically processed as a WEB transaction. Internet-Initiated Entries signify that the transaction was started in an internet environment.

Telephone-Initiated Entry (TEL)

Telephone-Initiated Entry applies when you authorize a payment over the phone. For instance, if you call your utility company and provide your bank account details to pay your bill, the transaction will be processed as TEL.

Accounts Receivable Entry (ARC)

Businesses use this code when they convert a check you’ve written into an electronic payment. For instance, if you write a check at a grocery store, and the store processes it electronically instead of depositing the physical check, this is an ARC transaction.

Learn how to print checks in QuickBooks Online with our guide.

Back Office Conversion (BOC)

Similar to ARC, but instead of converting the check at the point of purchase, the business converts the check in their back office. This is common in environments where checks are still received, but the business prefers to process them electronically for efficiency.

Re-presented Check Entry (RCK)

If you write a check and it bounces due to insufficient funds in your account, the recipient can use RCK to re-submit the payment electronically. This is a way for businesses to attempt to collect the amount on a returned check electronically.

Point-of-Purchase (POP)

Point-of-Purchase is used when you write a check at a retail location and the merchant processes the check electronically right at the checkout. The Point-of-Purchase indicates that the check conversion happened at the point where the purchase was made.

International ACH Transaction (IAT)

International ACH Transactions (IAT) in the realm of ACH debits are specifically used when money is being debited from a U.S. bank account to send to a recipient in another country.

Corporate Trade Exchange (CTX)

This is a business-to-business transaction that allows for additional information to be sent with the payment. For example, if a company is paying another company and needs to include detailed information about what the payment is for, they would use CTX.

Automated Enrollment Entry (ENR)

Automated Enrollment Entry is used mainly by government agencies. When someone signs up to receive government benefits like Social Security or Veterans’ benefits via direct deposit, the enrollment process uses the ENR.

ACH debits: Conclusion

So, there you have it – the ACH debit system is a trusty tool in our financial toolkit. It’s not just about big businesses and complicated money transfers; it’s actually a part of our everyday money moves.

It’s more than just a convenience; it’s a secure and smart way to handle our money. From a small business paying its team to you setting up that automatic transfer to save for a vacation, ACH debit is the behind-the-scenes hero making sure everything goes smoothly.