Welcome to the practical world of variance reports! Just like checking how much you spent on a vacation versus what you budgeted, businesses use variance reports to manage their finances. These reports are not just about numbers; they’re tools that help companies understand where they stand financially compared to their plans.

This guide will walk you through everything you need to know about variance reports in a simple, down-to-earth way. From understanding the basics of variance analysis to learning how to create and interpret these reports, we’ll cover all the essentials, ensuring you’re well-equipped to handle your business’s financial health.

Looking for a seamless way to manage your financial data? While you’re mastering variance reports, let Synder simplify your bookkeeping and transaction management.

What is a variance report?

A variance report is a financial tool used to measure the difference between planned (budgeted) and actual financial performance. This report highlights where you spent more or less than you expected.

The term variance comes from the fact that it shows the variance, or the difference, between what a company planned and what actually happened in financial terms.

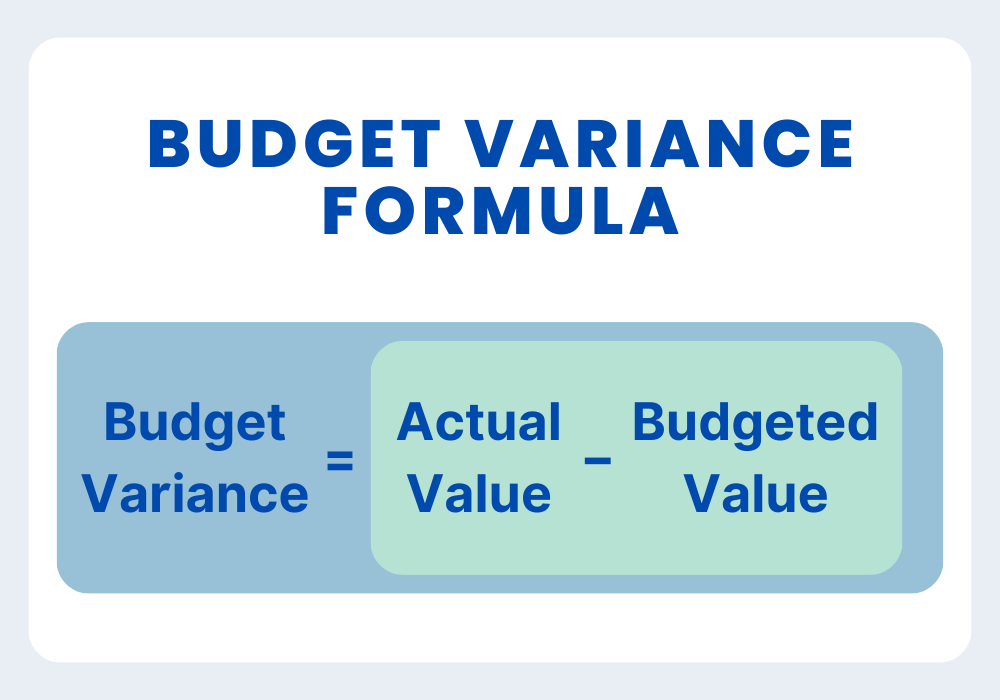

How to calculate variance with budget variance formula: Budget Variance = Actual Value − Budgeted Value

The variance formula is a fundamental tool used in financial analysis and management to assess performance against financial plans and budgets.

Here is the basic formula for calculating variance:

Budget Variance = Actual Value − Budgeted Value

Where:

- Actual value: This is the real, observed value that you record. For instance, if it’s about sales, it’s the sales revenue you actually earned. If it’s about expenses, it’s the amount you actually spent.

- Budgeted value: This is the value you had planned or expected. It’s the target or estimate you set in your budget for revenues or expenses.

- Budget variance: The difference between the budgeted and actual values. It can be favorable (better than expected) or unfavorable (worse than expected).

Variance analysis vs. variance report

Variance analysis is the process of figuring out why there are differences in financial performance, and a variance report is the document that shows and explains these differences.

Variance analysis

Think of variance analysis as the detective work in finance. It’s all about investigating the differences between how much they thought they would sell or spend and what actually happened.

It’s not just about finding these differences but also figuring out why they occurred. Was it because of more customers than expected? Higher costs for materials? This analysis helps in understanding the story behind the numbers.

Variance report

A variance report is like the summary of this detective work. It’s a document or a tool that shows these financial differences in a clear, organized way.

It typically includes columns or sections showing planned (budgeted) numbers, actual numbers, and the variance between them. It might also have notes explaining the reasons behind the variances.

This report is used to share the findings of the variance analysis with others in the company, like managers or department heads, so they can understand what’s going on with the finances.

Favorable and unfavorable variance vs. positive and negative variance

In financial management, interpreting variances is key to assessing company performance. Let’s explore the concepts of unfavorable and favorable variances, as well as the nuances of positive and negative variances, to see what they actually mean and how they impact a business’s financial health.

Favorable and unfavorable variances

- Favorable variance: This is when things turn out better than you planned. For sales, it means you sold more than you expected (which is great). For costs, it means you spent less than you budgeted (also great).

- Unfavorable variance: This is when things don’t go as well as you hoped. For sales, it means you sold less than you planned (not so great). For costs, it means you spent more than your budget (also not great).

Positive and negative variances

The terms positive and negative variances can be a bit confusing because they depend on the context (sales or costs):

- Positive variance in sales: This means you sold more than expected (favorable outcome).

- Negative variance in sales: This means you sold less than expected (unfavorable outcome).

- Positive variance in costs: Interestingly, this could be considered unfavorable because it means spending more than budgeted.

- Negative variance in costs: This is usually favorable since it means spending less than planned.

In a nutshell:

Favorable = Better than expected (more sales or less cost).

Unfavorable = Worse than expected (less sales or more cost).

Positive/Negative can mean different things based on whether you’re talking about sales or costs. Positive is always good for sales but not necessarily for costs, and vice versa for negative.

Types of variances typically reported

Now let’s explore three key types of variances – budget variance, sales variance, and expense variance – to see how they help businesses track their financial performance.

Budget variance

This involves comparing the overall budgeted financials with the actual results. For example, if your company planned to spend $10,000 but actually spent $12,000, there’s an unfavorable budget variance of $2,000.

Sales variance

Here, you compare actual sales against forecasted sales. If you predicted sales of $5,000 but achieved $6,000, you have a favorable sales variance of $1,000.

Expense variance

This looks at the difference in expected versus actual expenses. An example would be budgeting $2,000 for office supplies but only spending $1,500, resulting in a favorable expense variance of $500.

How to make a variance report

Creating a variance report is a structured process. We will now walk you through the six key steps, from gathering data to interpreting the results of the final report, to see how this crucial tool can provide insights into a company’s financial performance.

Step 1. Gather your data

First, collect all the necessary financial data. This includes your budgeted numbers (what you planned to spend or earn) and your actual numbers (what you actually spent or earned).

Step 2. Set up your template

Create a template with columns for budgeted figures, actual figures, and variance. You can do this in a spreadsheet program like Excel. Think of it like setting up a comparison chart.

Step 3. Input the figures

Fill in your budgeted and actual figures in the respective columns. Be careful to put each figure in the right place.

Step 4. Calculate the variances

For each item, subtract the budgeted figure from the actual figure to find the variance. If the actual figure is higher it will indicate that you’ve spent more or earned less than planned.

Step 5. Analyze the results

Look at where the variances are significant. These are areas that need attention. Ask yourself why these variances occurred.

Step 6. Write explanatory notes

For each significant variance, write a note explaining what caused it. This could be an unexpected expense, a change in market conditions, or a calculation error.

Tools and software for generating variance reports

Spreadsheet programs (like Microsoft Excel or Google Sheets) are the most common tools for creating variance reports. They are flexible and allow for easy calculations and formatting. Also, many accounting software like QuickBooks or Xero packages have built-in features for variance reporting.

For more advanced analysis, business intelligence tools such as Tableau or Power BI can create detailed and visually appealing variance reports.

Learn about business budgeting software for small businesses.

How to read and understand variance reports

First, look at the big picture. How does the overall actual performance compare to the budget? Are you generally over or under your planned figures?

Then, scan through the report and spot the areas with large differences between the budgeted and actual figures. These are your key focus areas. For each significant variance, note whether it’s favorable or unfavorable. A simple way to remember: if it’s about income, more than planned is good (favorable); if it’s about costs, less than planned is good (favorable).

If there are explanatory notes for variances, read them. They often provide context and reasons behind the numbers.

Interpreting the results: How do you know where the variance comes from?

When you see a variance in your report, figuring out where it comes from involves a bit of investigative work. By combining a thorough analysis of the numbers with internal and external reviews, you can usually trace back to where and why a variance occurred in your report. It’s about piecing together different bits of information to get the full picture.

Here’s how you can pinpoint the source of the variance:

- Analyze specific categories: Break down the report into categories like sales, expenses, production costs, etc. See which categories have the largest variances.

- Look at historical data: Compare the current variance with past trends. Is this a one-time occurrence or a recurring issue? Historical data can provide context.

- Check external factors: Consider market trends, economic changes, or industry updates. Sometimes variances are due to external factors beyond your control.

- Internal review: Look inside your company. Were there any operational changes, staffing issues, or policy updates that could have caused the variance?

- Discuss with teams: Talk to the people involved in the areas where variances occurred. They might provide firsthand information on why things didn’t go as planned.

- Identify patterns: Sometimes, the source of variance becomes clear when you notice patterns. For example, if marketing expenses are consistently over budget, maybe your advertising strategy is more costly than expected.

Case examples to illustrate common interpretations

We will now explore three real-life examples to see how companies can interpret and act on different types of variances in their reports.

Case example 1: Better-than-expected sales

Variance report: Your report shows a favorable sales variance.

Interpretation: The company sold more than they thought they would, which is great news. It looks like the sales team’s efforts are paying off or the new ad campaign is really hitting the mark.

Action: To invest more in what’s working, like additional training or marketing efforts.

Case Example 2: Higher utility bills

Variance report: There’s an unfavorable variance in utility expenses.

Interpretation: The company’s electricity and water bills came in higher than they expected. Maybe they’ve been using more power than usual, or energy prices have gone up.

Action: To consider ways to save energy, like using more efficient equipment, or maybe even talking to the power company to get a better deal on rates.

Case Example 3: Slower production

Variance report: You notice an unfavorable efficiency variance in production.

Interpretation: The company is finding that making their products is taking longer than they planned, which isn’t ideal. It could be because their machines are old or they don’t have enough people on the job.

Action: To investigate production processes for potential delays or bottlenecks.

If you’re finding our insights on variance reports valuable, you’ll also benefit from our article about product cost and period costs which delves into another crucial aspect of business finance and costing strategies.

What are the key things to remember when working with variance reports

Working with variance reports doesn’t have to be complicated. Here are some key things to keep in mind.

Preparation and analysis

First, make sure you have accurate data coming in and that all revenues and expenses are accounted. Any errors or missing data at this point can lead to the wrong conclusions.

Focus on big differences between your budget and actual figures. These are the red flags that need your attention. If you budgeted $1,000 for supplies but spent $2,000, that’s something to dig into. Most importantly, don’t just spot the differences; try to understand why they happened.

Communication and decision-making

Your variance report should be easy to read so use clear headings and simple language. Share what you find with your team or other departments. If everyone understands where the money’s going, it’s easier to make smart financial decisions.

Continuous improvement

Update your variance reports regularly – ideally monthly or quarterly.

Use your variance reports to improve future planning. If you always spend more than planned, maybe your budgets are too tight. It’s all about learning from the past to do better in the future.

Variance reporting: Conclusion

Variance reports can be the financial compass that guides you through the often complex world of financial management. By now, you should have a clear understanding of what variance reports are, how to create them, and, most importantly, how to use them to make informed decisions.

Whether it’s identifying areas for cost-saving, improving efficiency, or adjusting strategies, variance reports play a crucial role in steering a business toward success. So, keep these tips in mind, embrace the power of variance analysis, and watch your business navigate its financial path with more confidence and clarity.

Your blog has been a source of inspiration and learning for me. Thank you for your valuable contributions.