Research and development (R&D) are the birthplaces of ideas, prototypes, and groundbreaking solutions. But there’s more to R&D than just innovations and experimentation. Operating from behind the scenes, there’s also a complex web of financial decisions and strategies, especially when it comes to accounting and taxes.

If the amortization of intangible assets sounds overwhelming, this article is for you. We will take a step-by-step approach to explain all the key terms in the amortization of R&D expenses. We will also show how the new law affects tax liabilities and why it has been a source of heated debate.

Curious about seamless, accurate bookkeeping? Explore Synder and discover the ultimate solution for your accounting needs. From automated transactions to insightful reports, Synder provides everything you need to streamline your finances effortlessly. Don’t just take our word for it – see for yourself how Synder can change the way you think about bookkeeping.

TL;DR

- R&D expenditures cover both tangible and intangible assets, fueling innovation and competitive advantage.

- The Tax Cuts and Jobs Act mandates the amortization of intangible R&D costs, changing how businesses deduct these expenses.

- Understanding R&D accounting and tax changes is crucial for strategic financial planning and compliance.

R&D costs: What are research and development expenditures

When you have a research and development department, many of its expenses go into the day-to-day running of it, also known as operational expenses (OpEx). These expenses include things like paying salaries to employees, renting a lab space, buying supplies, and paying for utilities. And these are not the types of costs that we will talk about today.

What we will dive into are the type of expenses that create value for years to come, typically referred to as capital expenditures (CapEx) or capitalized expenses. Capital expenditures often include the purchase of physical items like machinery, buildings, or technology, as well as investments in patents or software development.

We clearly can see how such spending could be lifeforce for research and development department. It lets them buy the elements they need to develop new products or services.

From expenses to assets

When reading the above definition of capital expenses you can see, that one hand, a company is spending money and on the other hand, it is gaining something – an asses that they can keep using for a long time to create value for the business. Here, an interesting thing can happen to those capital expenses – they can be turned into assets.

What are assets?

Assets are items or resources a company owns that can help it make more money, spend less, or get better at what it does in the future. In other words, these elements are called assets because they provide future economic benefits to the company. They keep giving value over an extended period of time.

Buying a machine for your research and development activities or a patent are both considered assets but we can see they are not of the same kind. One is a physical item and the other is an intellectual property.

Tangible assets vs. intangible assets

Tangible assets in research and development could include physical items like laboratory equipment, machinery, or computers used in the research activities. These assets have a physical presence.

While intangible assets resulting from research and development activities might include patents, software developed for sale, or other intellectual property. These assets lack physical substance.

How expenses can turn into assets?

Expenses can turn into assets when the money spent on certain activities is expected to provide future economic benefits beyond the current accounting period. This transformation from expense to asset is called capitalization. Let’s see how it works.

Capitalization criteria

For an expense to be classified as an asset, it must meet specific criteria set by accounting standards, such as those outlined by such the U.S. Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS). These criteria include the expectation of future economic benefits, the ability to measure the cost reliably, and, in some cases, evidence of technical and commercial feasibility.

Recognition as assets

Once the criteria are met, the costs are recognized as assets on the balance sheet rather than being immediately expensed in the income statement. This means they are considered a valuable resource owned by the company that will contribute to future income.

Let’s look at a practical example of capitalization. Imagine, a company spends $1 million on developing a new software program. The development meets the capitalization criteria (e.g., technical feasibility has been demonstrated, the company can use or sell the software, and the software is expected to generate future revenue). Instead of expensing the $1 million as it’s incurred, the company capitalizes this cost as an intangible asset and what happens afterward is depreciation or amortization of those costs.

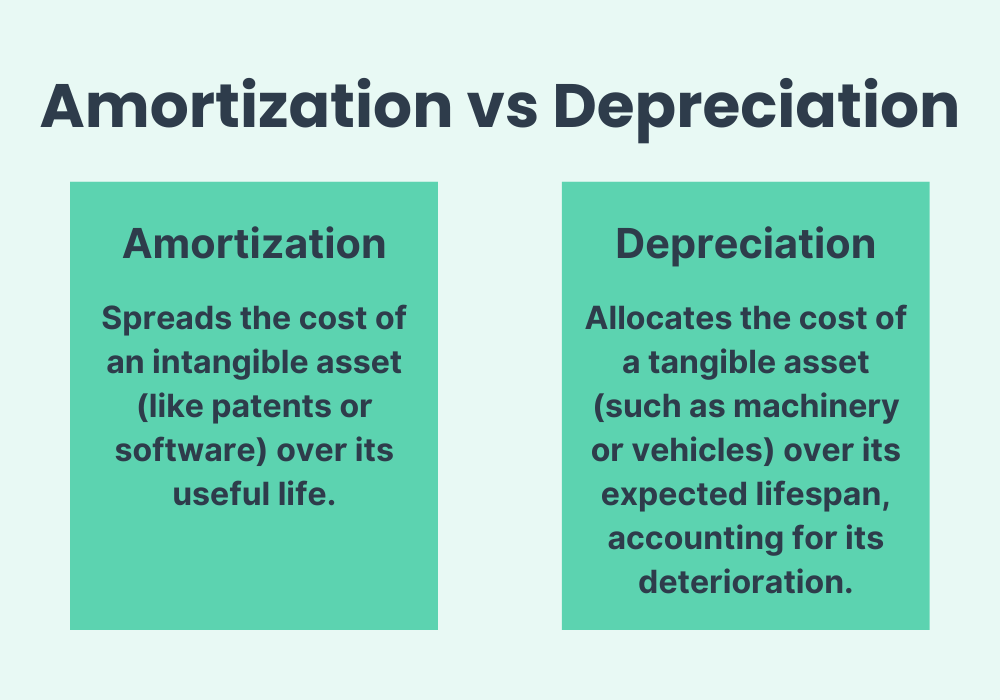

Depreciation and amortization

What’s interesting about tangible and intangible assets is that the way their value changes over time is not the same. Think about it, the machine will be worth less and less every year but a patent, for example, doesn’t have the same wear and tear quality to it. How do you measure the value of a machine after 3 years of usage as opposed to a patent that you have been using during the same time period? That’s where depreciation and amortization come to the rescue.

You use depreciation to reflect the value of tangible assets and amortization to reflect the value of intangible assets. In other words, amortization and depreciation and methods that help you calculate the value of different types of assets, each according to its type.

I hope that by now, the line from the introduction, i.e. the amortization of intangible assets sounds less overwhelming. We will now zoom in on amortization and depreciation to understand in detail how it plays out in research and development.

If you want to employ a bookkeeper for your business, read our article about bookkeeper interview questions.

What is depreciation?

Depreciation is how companies account for the loss in value of their big purchases (like vehicles, machinery, or equipment) over time. That is to say, they spread depreciation expense over the item’s useful life. This way, the expense matches up with the income the asset helps to bring in over the years, giving a fairer view of the company’s financial health.

What is amortization?

Amortization is the process used for spreading the cost of an intangible asset (like software licenses, patents, or copyrights) over its useful life, making your business’s financial statements a more accurate reflection of its yearly expenses and income. This method ensures that the cost of assets that benefit your business over several years is recognized in a way that matches their contribution to generating revenue.

Amortization example

Imagine your business purchases a software license or develops a new software program for internal use, costing a significant amount of money. Software, being something you cannot physically touch but providing value to your business, as we know is considered an intangible asset.

In this case, you don’t record the entire cost of the software in the year it was purchased or developed. Instead, you use amortization to spread out this cost over the software’s useful life, which might be several years. This way, each year, you only account for a portion of the software’s cost as an expense, aligning the expense with the benefits (or revenue) the software helps to generate over time.

Explore what you need to know about excise tax returns with our guide to the IRS Form 720.

How is R&D treated in accounting?

Grasping how research and development costs are handled in accounting is really important for making smart financial decisions, investing wisely, and following the rules of financial reporting. Both GAAP and IFRS give guidelines for how those expenditures should be treated.

Under U.S. GAAP

In the U.S., the rules for handling business expenses related to research and development are pretty straightforward. Generally, when a company spends money on R&D, it has to record these costs as expenses right away. This method is cautious because it’s often uncertain whether the money spent on R&D will lead to profitable products or inventions in the future. Recording these costs immediately can lower the company’s earnings on paper for that time period.

But, there are a few exceptions to this rule. For instance, if a company spends money on developing a product and that product is finally ready to be sold, those costs can be treated differently. Instead of being recorded as immediate expenses, they can be spread out over time. This is also true for software development. Once it’s clear that the software can be completed and will work as intended, the costs involved in creating it can be spread across several years. This method helps in matching the costs of creating the product with the income it generates over its lifetime, making the company’s financial health easier to understand.

Under IFRS

International rules for handling business spending on research and development offer a bit different approach compared to U.S. rules. These international rules, known as IFRS, make a clear split between the early stage of R&D (called the research phase) and the later stage (called the development phase).

For the early stage (research), companies do what they do in the U.S.: they record the money spent as an immediate expense. This means they acknowledge the cost right away because it’s uncertain if this early research will lead to something profitable.

For the later stage (development), things change. If a company can show that what they’re developing is likely to be finished, will be used or sold, and will make money in the future, then they’re allowed to treat these costs differently. Instead of treating the money spent as an immediate expense, they can recognize it as an investment spread out over time. As we know, this is capitalization of the costs.

Key takeaways

Handling research and development expenses is all about finding the right balance. On one hand, we want to recognize that spending money on research and development could lead to big benefits down the road, like new products or better ways of doing things. On the other hand, there’s always a bit of uncertainty with R&D because it’s not often clear which projects will succeed and which ones won’t.

Understanding this balance helps businesses and investors make informed choices and ensures they’re keeping their financial records in line with what’s expected. But it also leaves room for interpretation which can be problematic in its own right.

How the tax changes impact R&D spending

Now that we’ve got clarity on how companies spread out the costs of their R&D projects over time, it’s time to pivot to taxes. The way businesses account for the money they pour into R&D doesn’t just end up on their balance sheets; it also plays a vital role in how much tax they owe. And there’s been a big shake-up in this area, thanks to the Tax Cuts and Jobs Act (TCJA).

Learn more and find out, how long it takes for the IRS to approve a refund after it is accepted, with our guide to tax return & refund process.

Tax Cuts and Jobs Act impact on taxes

Back in 2017, this law changed some rules about taxes, including how companies can write off the money they spend on research and development. Before the TCJA, businesses could deduct these costs right away, which gave them an instant discount on their tax bill for every dollar they spent on innovation. But now, with the new law that started in 2022, companies have to spread those deductions and amortize those intangible R&D costs we talked about.

This change is substantial. It means businesses have to think harder about how their research and development spending will affect their taxes not just this year, but down the road too. Let’s dive into how it’s affecting companies and why it’s got some people in the business world feeling pretty heated.

Tax treatment of R&D under the new ruling

As a part of the Tax Cuts and Jobs Act, the tax treatment of R&D expenditures shifts from immediately expensing R&D costs to requiring amortization over a specified period. Instead of deducting these costs in full in the year they are incurred, businesses must now spread (amortize) the deduction over five years for domestic R&D expenditures and 15 years for foreign research and development expenditures.

For tangible assets used in research and development, the depreciation rules continue to apply, allowing businesses to deduct their cost over the assets’ useful lives according to existing depreciation schedules.

Impact of tax liabilities on companies

If you’re scratching your head thinking that the Tax Cuts and Jobs Act doesn’t fully support the rules set by GAAP and IFRS, you won’t be wrong. The new tax law brought discontent within the industries that invest heavily in research and development as it can create financial issues for their businesses. Here is how.

How deductions lower the taxable income

Imagine a startup company that throughout the year generates $300,000 in revenue and incurs $240,000 in operating expenses. Additionally, the company has decided to invest $60,000 in a new product development project, aiming to innovate and expand its market reach.

Previously, the company’s investment in R&D would be fully deductible in the same fiscal year. This would lead to a scenario where the company breaks even, as its total expenses ($250,000 in operating expenses + $50,000 in R&D) match its revenue ($300,000). So, there would be no income left to tax.

However, under the new rules of R&D amortization, the company can only deduct a portion of its R&D investment in the first year (and the rest in subsequent years). Deducting 10% out of $50,000 of the total R&D investment means they can only deduct $5,000. This adjustment would result in the company reporting a taxable income of $45,000 ($300,000 revenue – $250,000 operating expenses – $5,000 R&D deduction). That’s the income they need to now pay tax on. But as we know in reality there is no profit, and there is no money left.

So to cover the tax on the $45,000, a business might have to think about getting a loan or using any savings it has. This shows how the rule requiring companies to spread out their R&D costs over time can really put a financial burden on them. This is especially tough for new companies that are investing a lot in creating new products or services. And that is why there have been many initiatives that are trying hard to change this law.

Want to learn more? Read our tax filing preparation guide: ‘How to File Income Tax Return’ or 14 tax tips for small businesses, to prepare your company for tax season.

FAQ Section

1. What is R&D amortization?

R&D amortization refers to spreading the cost of research and development expenses over their useful life instead of expensing them all at once. This approach is particularly relevant for intangible assets developed through R&D activities.

2. How does GAAP treat R&D expenses?

Under U.S. Generally Accepted Accounting Principles (GAAP), R&D expenses are typically expensed as incurred, reflecting the uncertainty of future benefits. However, there are exceptions, such as certain software development costs, which can be capitalized and amortized.

3. How did the Tax Cuts and Jobs Act change the treatment of R&D expenses?

The Tax Cuts and Jobs Act, effective from 2022, requires businesses to amortize R&D expenses over five years for domestic expenditures and 15 years for foreign expenditures, changing the previous practice of immediate expensing.

4. Why is the amortization of R&D costs a concern for businesses?

Amortizing R&D costs can lead to higher taxable income in the short term since only a portion of R&D expenses is deductible each year. This can create cash flow issues for businesses, particularly startups that rely heavily on research and development for growth but may not have profits to offset these costs.

5. What are tangible and intangible assets in R&D?

Tangible assets include physical items like laboratory equipment and machinery used in R&D processes. Intangible assets result from research and development activities, such as patents and software developed for sale, and lack physical substance.

6. How can R&D expenses turn into assets?

R&D expenses can become assets through capitalization, where the expenses meet certain criteria indicating future economic benefits. These capitalized costs are then recognized as assets on the balance sheet and amortized over their useful life.

7. How do tax changes impact R&D spending?

The requirement to amortize R&D costs under the Tax Cuts and Jobs Act affects companies’ taxable income and tax liabilities, potentially leading to financial strains as immediate tax deductions for R&D expenditures are limited. For domestic R&D you need to amortize expenses over five years rather than immediately deduct them from the company’s taxable income.

8. Can you amortize research and development?

Yes, research and development costs can be amortized, especially when these costs are capitalized as intangible assets. This process involves spreading the cost over the asset’s useful life, reflecting the period over which it is expected to generate revenue for the company.

9. Does research and development depreciate?

Depreciation specifically applies to tangible assets. While R&D itself doesn’t depreciate, the tangible assets purchased or used in research and development activities, such as laboratory equipment or machinery, can depreciate over their useful life. Intangible assets resulting from R&D, however, are amortized.

10. Should R&D be capitalized or expensed?

The decision to capitalize or expense R&D costs depends on the accounting framework (such as U.S. GAAP or IFRS), the specific circumstances of the research and development activities, the new federal tax law, and other state and local tax laws that affect R&D expenditures.

Conclusion

From the get-go, we’ve journeyed through the essentials of R&D costs, untangling the language of capital expenditures, intangible assets, amortization, and many more.

We hope that the amortization of R&D costs, a topic that might have seemed daunting when we started this article, is now a concept you can navigate with confidence.

As we’ve seen, the path laid out by GAAP and IFRS offers different strategies for capturing the essence of your research and development efforts, each with its implications for your financial statements and tax liabilities. The introduction of the Tax Cuts and Jobs Act adds another layer to this journey, reshaping how businesses need to approach their R&D spending with an eye toward amortization.

So, where does this leave us? Hopefully, with plenty of help from your tax professional as the R&D expenditure situation is nuanced and quite complex.

Remember, the goal is to comply with accounting standards and tax regulations as well as strategically manage your R&D investments to fuel growth, drive innovation, and build a sustainable competitive edge. After all, today’s R&D expenditures are tomorrow’s breakthroughs.

This article has been prepared for informational purposes only and gives a general overview of research and development amortization. It’s not intended to provide any tax advice. It’s highly recommended to consult with a tax professional to ensure that taxes are properly calculated and reported.

Ready to revolutionize your bookkeeping? Dive into the future of finance with Synder! Sign up now for our free trial or secure your spot in our Weekly Public Demo. Experience firsthand how Synder simplifies accounting, offering precision, efficiency, and peace of mind. Transform your financial management today – your ledger will thank you.

Share your experience

Got insights or stories about handling R&D costs, especially with the recent tax law changes? We’re all ears! Drop your experiences, tips, and any challenges you’ve faced in the comments below. Let’s support each other and grow together. Share your journey with us now!