When you run a business, it might sometimes feel like there are two parallel words: your actual business and accounting. The truth is, however, that accounting is there to capture your business in financial terms. One doesn’t exist without the other.

That’s why, as a small business owner, getting a firm grasp of all those key accounting terms is tremendously helpful and also necessary.

Today’s topic is Accounts Receivable (AR) and its place in your accounting books. Spoiler alert, if you want to know whether Accounts Receivable is an asset, the answer is: yes it is. For all other information relating to how Accounts Receivable fit into your small business assets, read on.

Juggling Accounts Receivable from various sales channels and payment platforms? Check out Synder, software made to automate AR processing for complex ecommerce and SaaS transactions.

TL;DR

- Accounts Receivable is considered an asset that represents expected cash inflows from credit sales.

- Accrual accounting allows businesses to recognize income when earned, highlighting the importance of AR.

- Managing AR efficiently can improve a business’s cash flow and financial health, reducing the risk of bad debts.

- Technology can significantly streamline AR management, offering automated invoicing and real-time reporting.

Laying the groundwork for Accounts Receivable: What you need to know

To be able to comfortably talk about Accounts Receivable in terms of assets we need to clarify a few things first.

In the following sections, we will define:

- Accounts Receivable definition;

- The accounting method that supports AR;

- Types of accounts in accounting;

- Types of assets.

What is Accounts Receivable?

Accounts Receivable (AR) is a type of account used in accounting to track money that is owed to a business by its customers for goods or services that have been delivered or used but not yet paid for. It’s like an IOU from the customer to the business.

This also means that if your small business doesn’t sell anything on credit, it doesn’t have any need for Accounts Receivable.

Imagine you own a small web design company, and you’ve just completed a website redesign for a client. The total cost of the project is $5,000. You issue an invoice to the client with a term of net 30 days, meaning the client has 30 days to pay the invoice.

You’ve earned that money as you completed the project for them, but you don’t physically have this money as the client has 30 days to pay the invoice. What do you record in your books when you issue that invoice?

Is this an income or not? Let’s find out.

When do you record a transaction in your books?

You can see how it makes sense to record this transaction as an income when you completed all the work and issued an invoice and also it makes sense to record it once you receive the actual money for it. That’s the difference between 2 accounting methods: accrual-based and cash-based accounting.

Accrual accounting

If you’re using the accrual basis of accounting, you recognize income when it’s earned and expenses when they’re incurred, regardless of when cash is exchanged. In simpler terms, it means you count your earnings when you make a sale and your costs when you use a service or buy something, no matter when you actually get or spend the money.

Under this method, you’re recognizing the revenue ($5,000 from our example) at the time of sale, not when you receive payment.

Accounts Receivable becomes then a temporary storage for income that has been earned (invoice also issued) but actual payment has not yet arrived.

Cash accounting

If you’re using the cash basis of accounting, you recognize income and expenses only when cash is actually received or paid. With this method, there’s no need to track Accounts Receivable in the traditional sense because transactions are only recorded when payment is received.

Accounting methods and Accounts Receivable: Key takeaways

As you can see, speaking about Accounts Receivable only makes sense, when we use the accrual accounting method, since only there do we record that gap between when we earned the income and when we receive the payment.

Do all small businesses need Accounts Receivable?

As a small business owner, whether or not you need to include Accounts Receivable in your books depends on a few factors, such as your business model, payment terms you offer to customers, and the accounting method you use.

What does ‘receivable’ mean in Accounts Receivable?

Now you can probably begin to get the idea why Accounts Receivable has such a name. The term “receivable” means expected to be received by the business. Who knew there would be an account with so much faith in payments coming through in the future? In the later section, we will look at what happens when that faith is broken.

Having established what Accounts Receivable is, we can turn to the second part of our topic, and that is assets.

Where can you find assets in accounting?

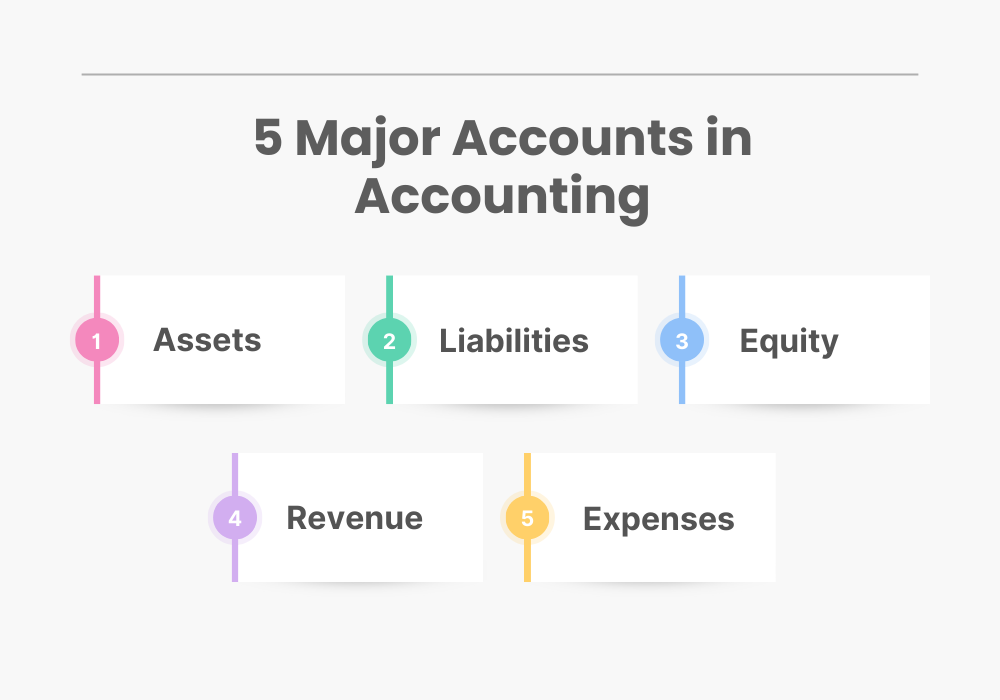

Everything a business deals with can be categorized into five main types of accounts. These accounts help organize finances and provide a clear picture of a business’s financial health. Assets are one of these categories. Let’s have a look.

Assets

Assets are resources owned or controlled by a business, expected to bring future economic benefits. Examples include cash, Accounts Receivable, inventory, equipment, and buildings.

Liabilities

Liabilities are what a business owes to others—these are obligations that need to be paid off, such as loans, Accounts Payable, mortgages, and other debts. While assets are what a company owns, liabilities are what a company owes. The difference between assets and liabilities reflects the net worth or equity of the business.

Equity

Equity represents the owner’s claims on the assets of the business after all liabilities have been deducted. It’s essentially the net assets of a company and includes common stock, retained earnings, and additional paid-in capital.

Equity can be thought of as the residual interest in the assets of the entity after deducting liabilities. It’s what remains for the owners once all obligations are settled.

Revenue

Revenue accounts track the income a business earns from its operations, like sales revenue, service revenue, and interest income. It’s the total amount of income generated by the sale of goods or services related to the company’s primary operations.

Increasing revenue typically leads to an increase in assets (e.g., cash or Accounts Receivable) because it represents income coming into the business.

Expenses

Expenses are the costs incurred in the process of generating revenue, such as rent, salaries, utilities, and cost of goods sold. These are outflows or using up of assets as part of operations of the business to generate sales.

Expenses usually result in a decrease in assets, as they often entail the outflow of cash or other resources.

What are the main types of assets?

Continuing our journey of accounts, let’s zoom in on our main star, which is assets. We already know that assets are resources owned or controlled by a business expected to bring future economic benefits. However, they are further categorized into several main types to provide clarity and organization in financial reporting and analysis.

Current assets

These are assets expected to be converted into cash, sold, or consumed within one year or within the business’s operating cycle, whichever is longer. Current assets include:

- Cash and cash equivalents: Currency, bank balances, and short-term investments that can quickly be converted into cash with little risk of value change.

- Accounts Receivable: Money owed to the business by customers for goods or services delivered but not yet paid for.

- Inventory: Goods and materials held for sale or used in producing products.

- Prepaid expenses: Payments made in advance for goods or services to be received in the future, like insurance or rent.

Non-current assets (long-term assets)

Non-current assets are expected to provide economic benefits beyond one year and are not intended for sale in the regular course of business. These include:

- Property, plant, and equipment (PP&E): Tangible assets used in operations, like buildings, machinery, and vehicles, subject to depreciation (except land).

- Intangible assets: Non-physical assets with economic value, such as patents, trademarks, or copyrights.

- Long-term investments: Investments in bonds, stocks, or other entities expected to be held for more than one year.

- Deferred tax assets: Taxes overpaid or paid in advance, recoverable in future periods.

Fixed assets

Fixed assets, a subset of non-current assets, include property, plant, and equipment that are used in the operation of the business and are not intended for resale. These assets are capitalized and depreciated over their useful lives, except for land, which is not depreciated.

Tangible assets

Tangible assets are physical and can be touched, like machinery, buildings, vehicles, and inventory. They include both current assets (like inventory) and non-current assets (like PP&E).

Intangible assets

Intangible assets lack physical substance but have value based on rights or information, such as patents, trademarks, and goodwill. These assets can provide significant long-term value to a business.

If you want to learn more about intangible assets, read our guide on R&D amortization.

Is Accounts Receivable an asset?

I hope by now it is clear why would we call Accounts Receivable an asset account rather than any other type.

Accounts Receivable is an asset owned by a business and expected to give a future benefit to the business.

Accounts Receivable is expected to be converted into cash within the operational cycle of the business, typically within one year. This expected inflow of cash is considered a future economic benefit, that’s why Accounts Receivable is a current asset.

What’s more, the business has a legal claim to the funds due from the customers even if the money is not in their own pocket yet. This claim is based on the agreement or contract under which the goods or services were provided. So, the business controls the right to receive payment, fulfilling the ownership or control criterion of an asset.

Want to learn more? Read our in-depth article about Accounts Receivables.

What happens if a customer doesn’t pay the invoice?

That’s an excellent question both from the accounting and practical perspectives.

While businesses usually try to collect late payments in many ways possible, sometimes it just might be a sad reality that a client won’t pay. What happens with the Accounts Receivable amount, which by then we know will never actually be received?

If all efforts to collect the payment fail and there’s no realistic expectation of payment, the invoice amount may be written off as bad debt. This means the business recognizes it as an expense, reducing net income for the period.

Before recognizing a specific bad debt, many businesses use an allowance method, where they estimate the amount of receivables that may not be collected and record this estimated amount as a contra asset on the balance sheet. This account is called the Allowance for Doubtful Accounts. When a specific account is deemed uncollectible, it is written off against this allowance, and the bad debt expense is recognized.

For accounting purposes, this is done by debiting the Bad Debt Expense account and crediting Accounts Receivable to remove the amount.

Which financial statement reports Accounts Receivable?

Accounts Receivable is recorded as an asset on your balance sheet.

Accounts Receivable are listed as a line item on the balance sheet under current assets. This placement highlights their role in the company’s financial health and operational funding.

The balance of Accounts Receivable, net of any allowance for doubtful accounts (provision for credit losses), reflects the amount the business expects to collect, influencing both the asset total and the overall valuation of the company.

How technology can help you manage your Accounts Receivable

As you can imagine, matching open invoices in Accounts Receivable with payments can be a very time-consuming and error-prone process. That’s why relying on technology to do this for you is the best way to manage this account and bookkeeping in general.

One such software that is designed to streamline accounting processes for small businesses, including the management of Accounts Receivable, is Synder. By automating various accounting tasks, Synder can significantly help small businesses manage their AR more efficiently.

Automated invoice creation and sending

Synder can automatically generate and send invoices to customers immediately after a sale is made, whether it occurs online or through other channels. This prompt invoicing helps ensure that businesses do not delay or forget to invoice for services rendered or goods sold, potentially speeding up the payment process.

Integration with payment platforms

The software integrates seamlessly with various payment platforms and gateways (such as PayPal, Stripe, and Square), making it easier for businesses to accept payments in multiple forms. This integration ensures that payments are accurately recorded in real time, reducing the manual effort required to match payments with invoices and update the AR ledger.

Automatic reconciliation

Synder offers automatic reconciliation features, meaning it matches incoming payments with the corresponding invoices. This feature significantly reduces the manual work involved in ensuring that payments are correctly applied to outstanding invoices, improving the accuracy of AR records.

Real-time financial reporting

With Synder, businesses gain access to real-time financial reporting, which includes up-to-date information on their AR status. This allows business owners to quickly identify outstanding invoices, aging accounts receivables, and overall cash flow status, enabling more informed financial decision-making.

To find out how Synder can help your business streamline your Accounts Receivable process, book a seat at our Weekly Public Demo or sign up for our free trial.

Accounts Receivable as a current asset: Conclusion

Understanding and managing Accounts Receivable is vital for small business owners. It not only ensures that you recognize revenue accurately but also improves your cash flow and financial stability.

With the insights and tools discussed, from understanding AR as a crucial asset to leveraging technology like Synder to automate your AR processes, we hope that you are now confident in tackling your valuable asset – Accounts Receivable.

Share you experience

Have you had experiences, challenges, or successes with managing Accounts Receivable in your business? Whether it’s tips for effective collection strategies or lessons learned from dealing with unpaid invoices, your insights could help other small business owners navigate their AR journey. Share your stories in the comments below!

Excellent article!

Thank you so much, David! We always appreciate your engagement and support of our blog!