Ready to dive into a complete guide on IRS Form 2848? It’s your key to understanding the ins and outs of handling tax matters in the United States. Let’s break it down together. As taxpayers, we often encounter situations where seeking professional assistance becomes essential for effective communication and representation before the Internal Revenue Service (IRS). Form 2848, titled ‘Power of Attorney and Declaration of Representative’ (POA), serves as the bridge between individuals and their appointed representatives, granting a range of powers to navigate tax complexities.

In this article, we delve into the intricacies of Form 2848, exploring its purpose, filing procedures, key parties involved, and tips for seamless completion.

Understanding this powerful document is crucial for individuals looking to streamline their interactions with the IRS and ensure that their chosen representatives have the necessary authority. Join us on this journey as we clarify Form 2848 and empower you to take control of your tax affairs.

Disclaimer: This guide is provided for informational purposes only and is not intended to substitute professional advice. Accounting, tax, and financial matters can be complex, and the information presented here may not cover all possible scenarios or considerations specific to your situation. It is crucial to consult with a qualified professional accountant or tax advisor to address your individual needs and ensure compliance with applicable laws and regulations.

Contents:

2. What is the purpose of Form 2848?

3. What is the procedure for filing Form 2848?

6. What is the difference between IRS Form 8821 and 2848?

7. IRS Form 2848: Tips and tricks

8. IRS Form 2848: Key takeaways

9. Conclusion

10. FAQs

What is Form 2848?

Form 2848 is a document used in the United States by taxpayers to authorize someone else, typically a tax professional or representative, to be the point of contact for the IRS. The full name of the form is ‘Power of Attorney and Declaration of Representative.’

When a taxpayer fills out Form 2848, they are giving their representative the authority to perform various actions on their behalf, such as:

- accessing their tax information,

- receiving and responding to IRS notices,

- and representing them in meetings or hearings with the IRS.

This form is often used by individuals who want to hire a tax professional or attorney to handle their tax matters.

It’s important for both the taxpayer and the authorized representative to complete the form accurately, including providing details about the specific powers granted to the representative. Once completed and signed, the form is submitted to the IRS.

Key notes

Note 1: Taxpayers should be aware that Form 2848 does not grant the representative the authority to sign the taxpayer’s tax return unless they specifically authorize it on the form. Additionally, the authorization is typically limited to specific tax matters and may have an expiration date.

Note 2: Form 2848 can be utilized to authorize a representative to act on behalf of a diverse business entity, including a corporation, partnership, or LLC. This is particularly beneficial when addressing tax matters unique to this entity.

Power of attorney validity period

The Form 2848 does not have a fixed expiration date. The authorization granted through Form 2848 typically remains in effect until:

- it is revoked by the taxpayer,

- the representative withdraws,

- or the authorization is otherwise terminated.

The taxpayer, when filling out the form, can specify any limitations on the duration of the authorization. For example, they can indicate a specific expiration date or event that triggers the termination of the power of attorney. However, if no specific expiration date is provided, the authorization generally remains valid until it is explicitly revoked.

Key notes

Note 1: It’s crucial for individuals to carefully review the terms of Form 2848 and, if needed, consult with a tax professional or legal advisor to ensure that they understand the implications of the authorization and any limitations they may want to impose.

Browse our CPA directory to find accounting experts with ease.

Note 2: Since tax laws and forms can be subject to updates and changes, it’s advisable to check the latest version of the form and any accompanying instructions on the official IRS website or consult with a tax professional for the most current information.

What is the purpose of Form 2848?

The IRS Form 2848 serves the primary purpose of allowing a taxpayer to grant authority to another individual to act on their behalf before the IRS.

This form is commonly used when individuals or businesses want to appoint

- attorneys,

- certified public accountants (CPAs),

- enrolled agents,

- or any other persons authorized

to practice before the IRS to handle their tax affairs and communicate with the IRS on their behalf.

The main purposes of Form 2848 include:

- Accessing confidential tax information.

- Representing the taxpayer during IRS interviews, meetings, and conferences.

- Signing agreements, consents, or other documents related to tax matters.

- Receiving and inspecting confidential tax information.

Key notes

Note 1: The representative’s authority is limited to the matters specified on Form 2848, and the authorization may have a specific expiration date.

Note 2: The taxpayer can revoke the power of attorney at any time by submitting a new Form 2848 or by other written means.

What is the procedure for filing Form 2848?

Form 2848 allows a taxpayer to authorize a representative to act on their behalf in tax matters before the IRS. Here’s an overview of how the IRS Power of Attorney process works:

1. Obtain Form 2848

Download the PDF version of Form 2848 from the official IRS website (www.irs.gov) or obtain a physical copy from an IRS office.

2. Read the instructions

Carefully read the instructions provided with Form 2848. The instructions guide you on how to:

- complete the form,

- specify the scope of authority,

- and provide details about where to submit the form.

3. Complete Form

Fill out Form 2848 with the necessary details.

4. Specify the scope of authority

Clearly define the scope of the representative’s authority. This involves indicating:

- the specific tax matters,

- tax forms,

- and periods for which the representative is authorized to act on your behalf.

5. Sign and date the Form

Both the taxpayer (principal) and the representative must sign and date the form. The representative’s signature acknowledges their acceptance of the appointment, and the taxpayer’s signature indicates consent to the representation.

6. Attach additional information (if needed)

If the representative needs to receive copies of notices and communications, or if you want to authorize more than one representative, provide this information on the form or attach a separate statement.

7. Submit the Form to the IRS

Mail or fax the completed Form 2848 to the appropriate IRS office. The instructions provide specific information on where to submit the form based on your location and the type of tax matter involved.

Ensure that you send the form to the correct address or fax number. Incorrect submissions may result in processing delays.

8. Verification and processing by the IRS

The IRS will review the submitted Form 2848 to ensure that it is properly completed and signed. Once verified, the IRS will associate the representative with your taxpayer account.

9. Receive Confirmation (optional)

While not always necessary, you may receive a confirmation letter from the IRS acknowledging the acceptance of the Power of Attorney. This letter can serve as proof that the representative is authorized to act on your behalf.

10. Revocation (if needed)

If you need to revoke the representative’s authority at any point, you can do so by submitting a new Form 2848 or by other written means. The revocation becomes effective once processed by the IRS.

Key notes

Note 1: It’s essential for taxpayers to carefully consider the scope of authority granted to the representative and to choose a trusted and qualified individual or firm to act on their behalf.

Note 2: Additionally, keeping the form up-to-date and promptly revoking authorization when necessary ensure that the taxpayer has control over who represents them before the IRS.

Note 3: Remember to keep a copy of the completed Form 2848 for your records.

If you want to learn more about tax filing strategies, take a moment to read through this insightful article: How to File Taxes for Ecommerce.

Who can file Form 2848?

Form 2848 can be filed by taxpayers who want to authorize another individual to act on their behalf before the IRS.

Key parties involved in 2848

Here are the key parties involved:

- Taxpayer (or Client).

- Representative.

Taxpayer (or Client)

The taxpayer, also referred to as the ‘client’ on the form, is the individual granting the power of attorney. This is the person who owes the tax or has a tax-related matter for which they are seeking representation.

Representative

The representative is the individual authorized by the taxpayer to act on their behalf. This can be:

- an attorney,

- CPA,

- enrolled agent,

- or any other person authorized to practice before the IRS.

More information about it you will find in the section below.

Who can handle IRS matters on your behalf?

The authority to act on behalf of a taxpayer before the IRS is not granted to just anyone. While immediate family members can be authorized, the primary use of this authority, as outlined in the form, is to empower tax professionals to handle IRS matters on your behalf.

This includes individuals such as

- attorneys,

- CPAs,

- enrolled agents,

- enrolled actuaries,

- unenrolled return preparers (specifically if they prepared the relevant tax return),

- corporate officers or full-time employees (for business tax issues),

- enrolled retirement plan agents (for retirement plan tax matters),

- and representatives affiliated with qualified Low Income Taxpayer Clinic or Student Tax Clinic Programs.

How to file Form 2848

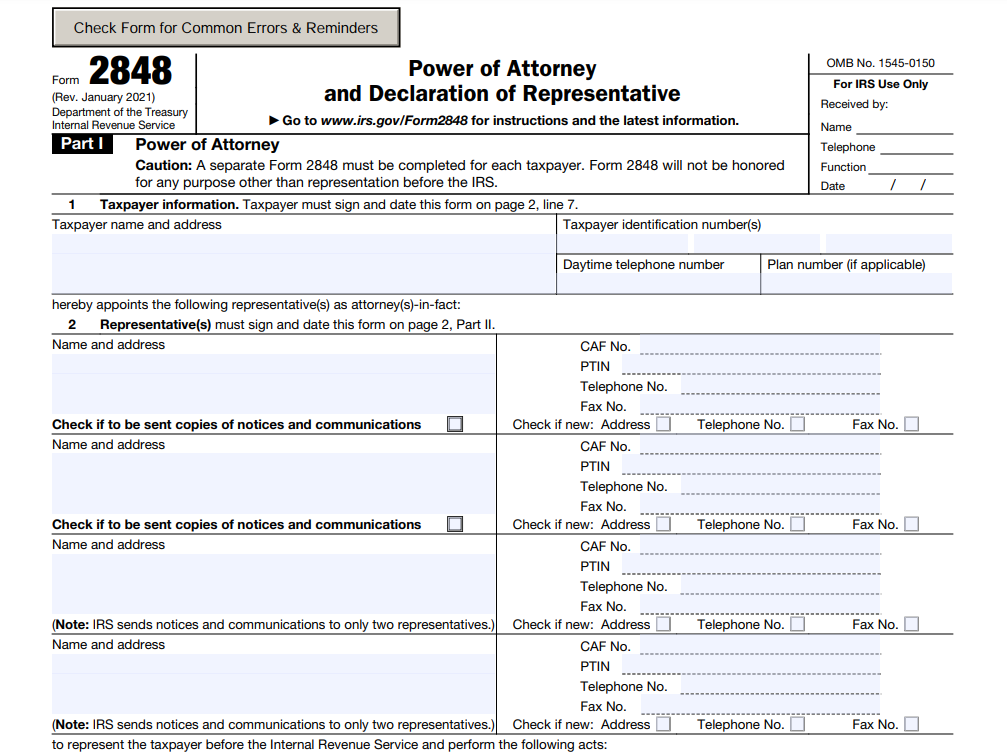

Form 2848 is the form that will need to be filed in order to create an IRS POA. Form 2848 has two parts: Part I and Part II.

Parts are broken into seven different sections that establish the various aspects of the agreement.

How to complete Form 2848: Part I

Part I of Form 2848 requires you to provide basic information about:

- yourself,

- the taxpayer,

- and the representative you are appointing.

Follow these steps to complete Part I:

Section 1: Taxpayer information

Line 1: Taxpayer’s name.

Enter your full legal name as it appears on your tax return.

Line 2: Taxpayer’s Identification Number (TIN).

Enter your:

- Social Security Number (SSN),

- Employer Identification Number (EIN),

- or Individual Taxpayer Identification Number (ITIN).

Section 2: Representative(s)

Lines 3-6: Representative’s name and address.

Enter:

- the full legal name,

- address,

- and telephone number of the representative(s) you are appointing.

Line 7: Centralized Authorization File (CAF) Number.

If the representative already has a CAF number, enter it here. If not, leave it blank.

Lines 8-14: Designation of representative.

Check the box that describes the authority you are granting to the representative. Typically, you’ll check either ‘Specific acts authorized’ or ‘All matters.’

Line 15: Specific acts.

If you checked ‘Specific acts authorized,’ provide a brief description of the specific tax matters the representative is authorized to handle.

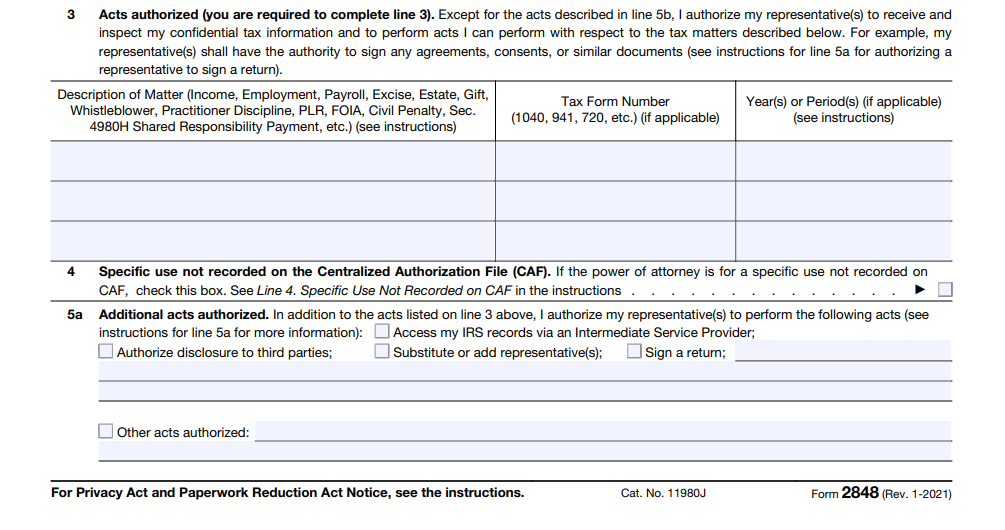

Section 3: Tax matters

Lines 16-20: Tax matters.

Check the box that corresponds to the type of tax matter for which the representative is authorized. You can choose from a variety of tax matters, such as:

- income tax,

- employment tax,

- excise tax, etc.

Section 4: Signature

Line 21: Taxpayer’s signature.

Sign and date the form. If you are a business, the form must be signed by an individual authorized to act on behalf of the business.

Section 5: Third-party designee

Lines 22-24: If you want to allow the IRS to discuss this form with a third-party designee (someone other than the representative), provide:

- their name,

- phone number,

- and any five-digit personal identification number (PIN) they will use.

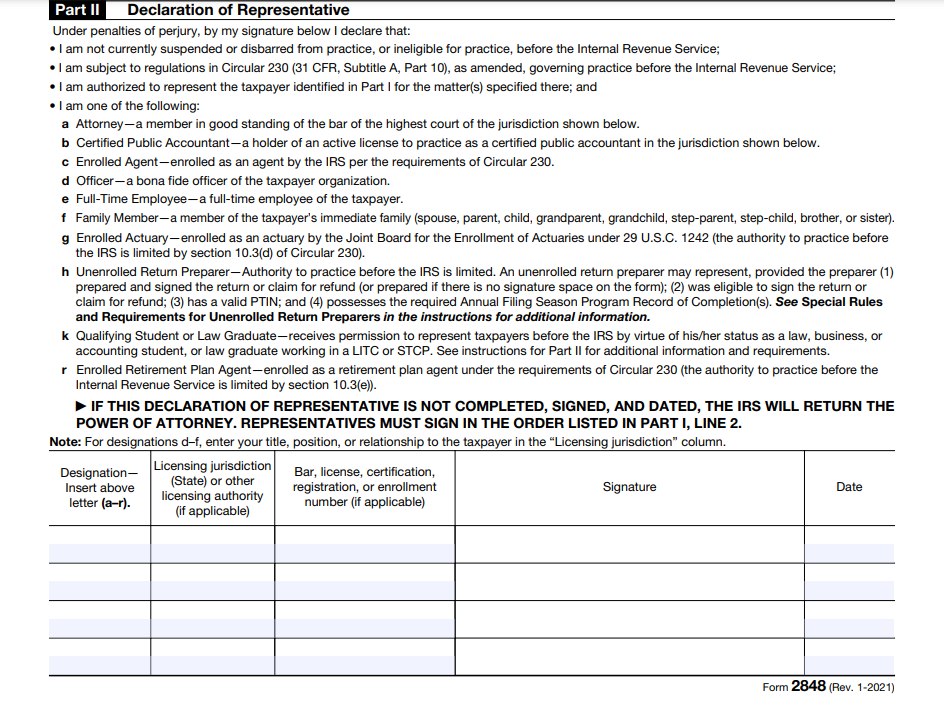

Section 6: Declaration of representative

Lines 25-28: The representative must sign and date the form, affirming that they are aware of their responsibilities and limitations.

How to complete Form 2848: Part II

This part provides additional information about the representative you have designated in Part I.

Also, Part II focuses on specific acts authorized and the tax matters involved.

Below is a guide to completing Part II:

Section A: Acts authorized

Line 29: Tax Form Number.

Enter the specific tax form number (e.g., Form 1040, Form 941) for which the representative is authorized to act on your behalf.

Lines 30-37: Check the applicable boxes to indicate the specific acts authorized. You can choose from a range of options, such as:

- signing returns,

- receiving confidential information,

- representing you at conferences, etc.

Section B: Representation before the IRS

Lines 38-47: Provide details about the specific tax matters for which the representative is authorized.

Include tax periods, type of tax, and any additional information necessary for clarification.

Section C: Retention/revocation of prior power(s) of attorney

Line 48: Check this box if you want to revoke any prior powers of attorney.

Section D: Signature of taxpayer or officer

Line 49: The taxpayer or authorized officer must sign and date the form in this section.

Note: Keep a copy for your records.

Some important notes

- Remember that the representative must be eligible to practice before the IRS.

- Check the instructions for the most up-to-date information and any additional requirements.

- It’s also a good idea to consult with a tax professional if you have any questions or concerns.

How do I get a CAF number?

Once you’ve completed and submitted Form 2848 to authorize a representative to act on your behalf before the IRS, the next crucial step is the processing by the IRS. During this process, the IRS assigns a unique identifier known as the Centralized Authorization File (CAF) number to the authorized representative.

Understanding the CAF number

The CAF number is a distinctive code that helps the IRS track and manage authorizations efficiently. This number is specific to the authorized representative and is crucial for their interactions with the IRS on your behalf.

Locating the CAF number

Upon successful processing of the authorization, the IRS typically issues a confirmation letter or notice. This documentation may include important details, including the assigned CAF number.

Taxpayers are advised to review the confirmation letter carefully to obtain and record the CAF number associated with their authorized representative.

Feel free to discover more in A Comprehensive Guide on Accounting for Taxes. We hope you find it as informative as this one!

What is the difference between IRS Form 8821 and 2848?

IRS Form 8821 and Form 2848 serve different purposes, even though they both involve authorizing individuals to represent you before the IRS.

Here are the key differences between the two forms:

| Form name | IRS Form 8821 | IRS Form 2848 |

| Name | ‘Tax Information Authorization’ | ‘Power of Attorney and Declaration of Representative’ |

| Purpose | Used to authorize a third party, such as a tax professional or tax preparation service, to access and receive your tax information. | Used to grant a broader authority, allowing a representative to act on your behalf and represent you before the IRS. |

| Scope | It is a limited authorization and does not grant the representative the authority to act on your behalf or make decisions. The representative can only receive and inspect your confidential tax information. | It grants the representative the power to perform various actions on your behalf, such as: signing agreements, receiving notices, and providing information to the IRS. |

| Representation | Does not authorize the representative to represent you in dealings with the IRS or sign documents on your behalf. | The representative can represent you in matters related to the specified tax forms and periods, including: communicating with the IRS, attending conferences, and signing agreements. |

| Specific information | You can specify the tax information and tax periods for which you are authorizing disclosure. | Provides more comprehensive authorization compared to Form 8821, allowing the representative to actively engage with the IRS on your tax matters. |

| Form name | IRS Form 8821 | IRS Form 2848 |

While both forms involve granting authority to a representative, Form 8821 is more focused on allowing access to tax information, whereas Form 2848 grants broader authority for representation and decision-making. The choice between the two forms depends on the specific tasks you want your representative to perform on your behalf.

Want to take a look at articles on similar tax topics? Form 944: Payroll Tax Reporting for Small Businesses With the 944 Form

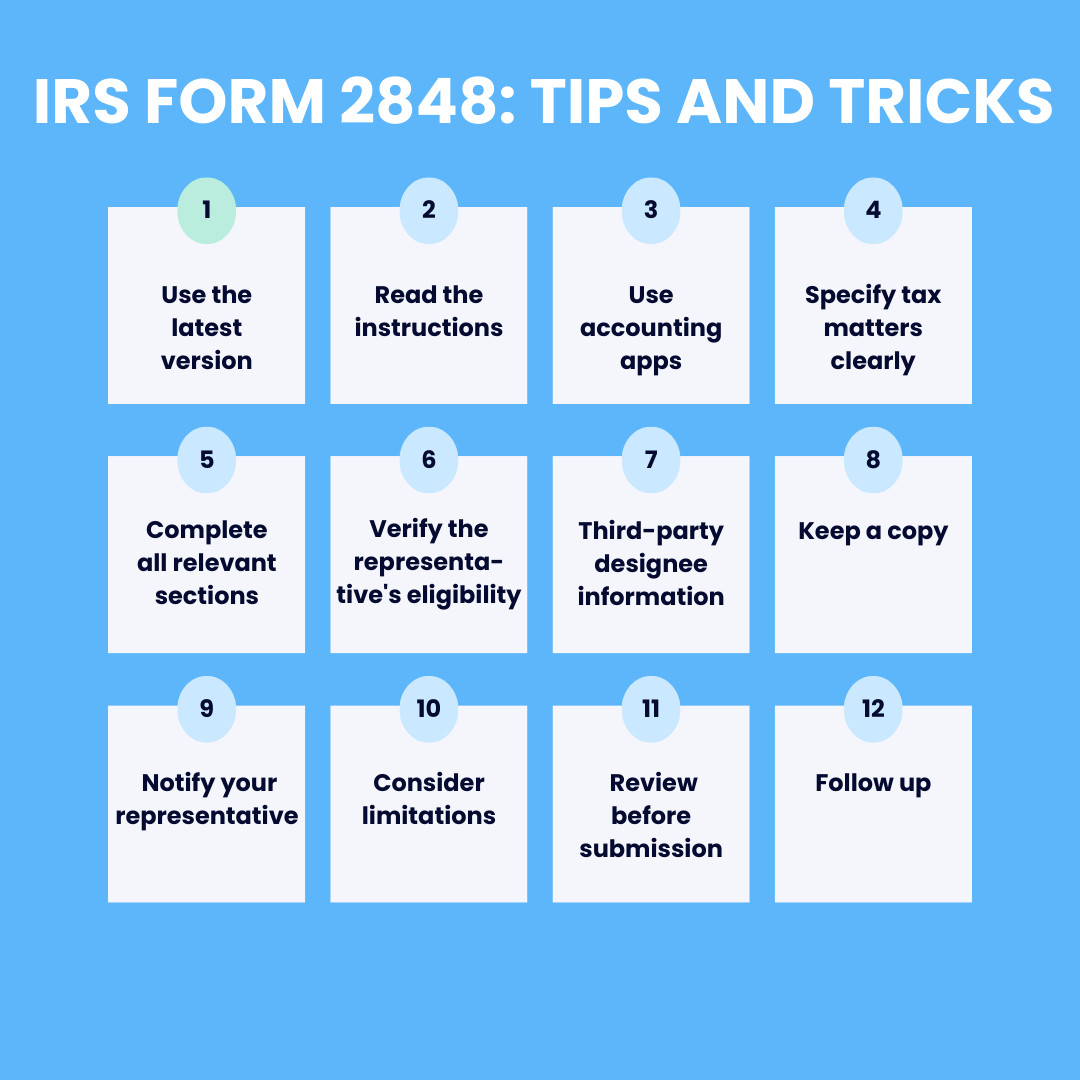

IRS Form 2848: Tips and tricks

When completing IRS Form 2848, here are some tips and tricks to keep in mind:

1. Use the latest version

Always use the most recent version of the form, which can be found on the IRS website. This ensures that you are using the current instructions and meeting any new requirements.

2. Read the instructions

Thoroughly read the instructions provided with the form. The instructions guide you through each section and provide important information about:

- eligibility,

- filing,

- and additional requirements.

3. Use accounting apps for Form 2848

For those who prefer to embrace the digital age, consider using accounting apps to enhance your financial tracking for IRS Form 2848. Real-time financial reporting tools can significantly streamline the process of managing business transactions.

Simplify your accounting tasks with Synder

Synder, in particular, offers a user-friendly interface that seamlessly syncs data, providing a hassle-free experience for business owners. Whether it’s income reporting, expense tracking, or overall financial management, Synder ensures accuracy and efficiency. Notably, Synder goes beyond basic accounting by incorporating tax recording features.

By integrating such tools into your financial workflow, you not only reduce the risk of errors but also improve the overall efficiency of your record-keeping.

Take advantage of the opportunity to optimize your business processes and explore the features of Synder with a free trial. To gain more insights and tips, consider participating in the informative Weekly Public Demo offered by Synder. Elevate your financial management with Synder – where simplicity meets effective financial operations.

4. Specify tax matters clearly

Clearly indicate:

- the specific tax matters,

- tax form numbers,

- and tax periods for which you are authorizing representation.

Be precise to avoid any confusion.

5. Complete all relevant sections

Fill out all necessary sections of the form, including both Part I and Part II. Incomplete forms may delay processing.

6. Verify the representative’s eligibility

Ensure that the individual you are appointing as your representative is eligible to practice before the IRS. Check the eligibility criteria outlined in the instructions.

7. Third-party designee information

If you choose to designate a third-party designee, provide accurate information. This person can discuss the authorization with the IRS and should have a unique identifier.

8. Keep a copy

Make a copy of the completed form for your records before submitting it to the IRS. This copy is important for reference and may be needed in the future.

9. Notify your representative

If you appoint a representative, inform them about the authorization. This helps in coordinating actions and avoiding misunderstandings.

10. Consider limitations

If you want to limit the authority of the representative to specific matters, clearly state those limitations in the form.

11. Review before submission

Review the completed form carefully for accuracy and completeness before submitting it to the IRS. Mistakes can lead to delays or issues with the authorization.

12. Follow up

After submission, follow up with the IRS to ensure that the form has been processed and that the representative is officially authorized.

Note: It’s always a good idea to consult with a tax professional if you have questions or concerns about completing Form 2848.

Check out related content: W9 vs 1099: Comparing IRS Forms 1099 vs W9

IRS Form 2848: Key takeaways

- Form 2848 grants permission for individuals or organizations to act on behalf of a taxpayer in dealings with the IRS.

- Authorized representatives include attorneys, CPAs, and enrolled agents.

- Signing this form and authorizing representation doesn’t absolve the taxpayer of any tax liabilities.

- Signing the form does not grant authority to do everything when it comes to your taxes on your behalf.

Conclusion

In conclusion, IRS Form 2848, the ‘Power of Attorney and Declaration of Representative,’ is a vital tool for taxpayers appointing representatives to act on their behalf before the IRS. This form grants broad authority, including accessing tax information and representing the taxpayer in IRS interactions.

The filing process is quite straightforward and involves:

- obtaining the form,

- carefully completing it,

- and submitting it to the IRS.

Key parties are the taxpayer and the representative, with eligibility criteria for representatives outlined by the IRS. Obtaining a CAF number is crucial for the representative.

To enhance efficiency, individuals may consider using accounting apps like Synder. Overall, Form 2848 empowers taxpayers in managing complex tax matters with qualified representation, ensuring effective communication with the IRS. Understanding the form’s nuances is essential for effective tax management.

Share your experience

Have you ever navigated the process of filing IRS Form 2848, the Power of Attorney and Declaration of Representative? We’re interested in hearing about your personal experience and any insights you can provide. Whether you found it to be a seamless process or encountered challenges, your feedback can be invaluable to others who may be undertaking the same task. Please take a moment to share your thoughts, tips, or any noteworthy aspects of your experience in the comments below. Your input could be immensely beneficial for those navigating the intricacies of IRS Form 2848.

FAQs

1. How to submit Form 2848 online?

In order to submit your form online, take the following actions:

- Login with your credentials and multi-factor authentication.

- Answer form-related questions and upload the signed Form 8821 or Form 2848 (one at a time).

- Avoid duplicate submissions if already sent by fax or mail.

- For additional forms, choose ‘Submit another form’ and answer authorization questions.

- If unable to use Secure Access, submit forms via fax or mail.

- After submission, you’ll receive a confirmation email.

2. What is the alternative to Form 2848?

The alternative to IRS Form 2848 is IRS Form 8821. While Form 2848 grants broader authority for representation before the IRS, Form 8821 provides a more limited authorization, allowing a third party to access specific tax information without representation. Choose the form based on the level of authority needed for your specific situation.

3. How to revoke a power of attorney

To revoke a power of attorney granted using Form 2848:

- Complete Form 2848: Fill out Part I (Sections 1-4) and Part II, Section 3.

- Sign and Date: Sign and date Part II, Section 4.

- Submit to IRS: Mail the form to the IRS.

- Notify Representative: Inform your representative in writing.

- Confirm with IRS: Follow up with the IRS to ensure processing.

Note: Consult IRS instructions or a tax professional for the latest details.

4. Why is the signature on IRS Form 2848 important?

The signature on Form 2848 authorizes a representative to act on the taxpayer’s behalf. It signals the taxpayer’s approval for the representative to handle their tax matters, including accessing information and communicating with the IRS. Without a valid signature, the authorization is incomplete. Both the taxpayer and representative should ensure the signature meets IRS requirements to avoid complications.

5. Can IRS Form 2848 be used to designate a representative for handling audits?

Yes, absolutely. Form 2848 is a powerful tool for taxpayers facing IRS audits. By completing this form, you can designate a representative to be the primary contact person, responding to audit inquiries, managing communication and providing necessary documentation, and representing your interests before the IRS.

Learn more about how to avoid getting tax audited by the IRS.

Running an international business? Learn the ins & outs of QB multicurrency in this article: QuickBooks Multiсurrency: What Multiсurrency Is & How to Manage Multiple Currencies in QuickBooks.