Bad debt is a common financial challenge faced by businesses of all sizes. Essentially, bad debt occurs when a receivable amount, typically from a customer or client, becomes uncollectible. This situation usually arises when the debtor is unable to fulfill their payment obligations due to financial insolvency or other reasons.

The management of bad debts is, therefore, a crucial aspect of financial administration for businesses. This is where tools like QuickBooks Online and QuickBooks Desktop come into play. QuickBooks, a popular accounting software, offers efficient solutions for tracking and managing financial transactions, including the handling of bad debts. It provides businesses with the necessary features to not only record and monitor receivables but also to effectively write off bad debts when deemed uncollectible. This ensures that financial records remain accurate and reflective of the company’s true financial position.

In the upcoming sections, we will delve into the specifics of how QuickBooks Online and Desktop can be utilized to manage and write off bad debts, ensuring that your business maintains healthy financial practices and accurate accounting records.

Ready to streamline your financial management and supercharge your accounting process? Discover the power of Synder – the one-stop solution for seamless integration of your sales and accounting data.

Understanding bad debt

In accounting, bad debt is a loss that a business incurs when it becomes apparent that the receivables from a customer cannot be collected. These receivables could be in the form of outstanding invoices or loan payments that are due to the business. Bad debt is recognized under the accrual accounting method, where revenues are recorded at the time of a sale, not necessarily when the cash is received. Therefore, when it’s clear that these revenues will not be received, they must be accounted for as bad debts.

Impact of bad debt on financial statements

The presence of bad debt has a direct and significant impact on a company’s financial statements:

- Income Statement: Bad debts are recorded as an expense, which reduces the net income of the business. This is because the anticipated revenue from the sales or services provided will not be realized.

- Balance Sheet: On the Balance Sheet, bad debts lead to a reduction in the Accounts Receivable balance, as they represent amounts that are no longer expected to be collected. Consequently, this affects the overall asset value of the company.

- Cash Flow Statement: While bad debts do not directly affect the cash flow (since the cash was never received), they impact the overall financial health portrayed by the Cash Flow Statement, reflecting the company’s efficiency in managing and collecting receivables.

Read on to find out how to write off bad debt in QuickBooks Online and QuickBooks Desktop.

How to write off bad debt in QuickBooks Online

Here is a straightforward guide to help you efficiently manage uncollectible receivables and write off bad debt in QuickBooksOnline.

Reviewing aging receivables

- Navigating to reports: Begin in QuickBooks by heading to the ‘Reports’ area.

- Accessing the Receivables Report: Search for and open the ‘Accounts Receivable Aging Detail Report’. This report is crucial for analyzing outstanding receivables.

- Identifying non-collectible receivables: Scrutinize the report to determine which receivables are unlikely to be collected and should be classified as bad debt.

Establishing a Bad Debts Expense Account

- Accessing the Chart of Accounts: Move to ‘Settings’ and select the ‘Chart of Accounts’ option.

- Creating an account: Opt for ‘New’ at the top right corner to start creating a new account.

- Choosing account specifications: In the account type section, pick ‘Expenses’. Then, for detail type, choose ‘Bad Debts’.

- Account naming: Label this new account as ‘Bad Debts’.

- Saving the account: Finalize by saving your changes with the ‘Save and Close’ option.

Setting up a bad debt item

- Products & Services section: Within ‘Settings’, proceed to the ‘Products & Services’ tab.

- Creating a placeholder item: Click ‘New’, then choose the ‘Non-inventory’ option. This step is for creating an item to represent the bad debt in your accounts.

- Naming the item: Designate this non-inventory item as ‘Bad Debts’.

- Linking to the Bad Debts Account: Connect this item to the previously established ‘Bad Debts’ account via the ‘Income Account’ dropdown.

- Completing the setup: Conclude this step by selecting ‘Save and Close’.

Generating a credit memo for the bad debt

- Starting the memo: Choose ‘+ New’ and then select ‘Credit Memo’ to initiate the process.

- Customer selection: From the ‘Customer’ dropdown list, pick the customer linked to the bad debt.

- Filling in the credit memo: In the ‘Product/Service’ area, select ‘Bad Debts’ and input the amount you’re writing off. Include a note stating ‘Bad Debt’ in the statement message box.

- Completing the memo: End this step by clicking ‘Save and Close’.

Applying the Credit Memo

- Initiating payment reception: Select ‘+ New’ and navigate to ‘Receive Payment’ under the ‘Customers’ section.

- Customer allocation: Choose the relevant customer from the dropdown menu.

- Invoice adjustment: In the ‘Outstanding Transactions’ area, mark the invoice you want to write off. Then, in the ‘Credits’ section, attach the previously created credit memo.

- Finalizing the application: Conclude by clicking ‘Save and Close’, which will reflect the bad debt in the Profit and Loss report under ‘Bad Debts’.

Generating a bad debt report

- Return to the Chart of Accounts: Head back to ‘Settings’ and select ‘Chart of Accounts’.

- Report generation: In the bad debts account row, click ‘Run report’ to view all tagged receivables as bad debt.

Additional recommendations

In the ‘Customers’ section under ‘Sales’, you can mark entities with bad debts. Edit their names to include a marker like ‘Bad Debt’ or ‘No Credit’. For maintaining accuracy, consider enlisting a QuickBooks Online and Desktop – certified bookkeeper to routinely categorize transactions and reconcile bank statements.

How to write off bad debts in QuickBooks Desktop

Writing off bad debt in QuickBooks Desktop is a process that helps keep your accounts receivable in QuickBooks and net income figures accurate. Here’s a detailed explanation of how to write off bad debt in QuickBooks Desktop.

Establish an expense account for monitoring bad debt

- Navigate to the Chart of Accounts: Start by going to the ‘Lists’ menu in QuickBooks Desktop. From there, select ‘Chart of Accounts’.

- Create a new account: In the Chart of Accounts, go to the ‘Account’ menu and choose ‘New’.

- Set up the account: Select ‘Expense’ as the account type and then click ‘Continue’.

- Name the account: Name this new expense account something indicative of its purpose, like ‘Bad Debt’.

- Save the account: Complete this step by selecting ‘Save and Close’. This account will be used to track bad debt losses.

Settling the uncollectible invoices

- AccessRreceive Payments: Go to the ‘Customers’ menu and choose ‘Receive Payments’. This is where you will manage the process of closing out the unpaid invoice.

- Select customer: In the ‘Received from’ field, enter the name of the customer who has the uncollectible invoice.

- Enter payment amount: Set the ‘Payment amount’ to $0.00, as you are not actually receiving any payment.

- Apply discounts and credits: Select ‘Discounts and credits’. This is where you’ll write off the unpaid amount.

- Write off the amount: In the ‘Amount of Discount’ field, input the amount you want to write off. This is the amount you’ve deemed uncollectible.

- Select the bad debt account: For the ‘Discount Account’, choose the bad debt expense account you created in the first step. This links the write-off to the correct account.

- Finalize the transaction: Click ‘Done’, then ‘Save and Close’. This action will officially write off the unpaid invoice amount and record it as bad debt.

Additional tip

You can monitor customer balances by using the ‘Accounts Receivable Aging Detail report’ to stay informed about your customers’ open balances. This can help you identify which invoices are at risk of becoming bad debts.

FAQ: Writing off bad debt in QuickBooks

Q1: What is bad debt in QuickBooks?

In QuickBooks, bad debt refers to money owed to your business that is considered uncollectible. This typically involves outstanding invoices that you’ve determined won’t be paid by the customer.

Q2: How do I write off bad debts in QuickBooks Online?

To write off bad debt in the online version of QuickBooks:

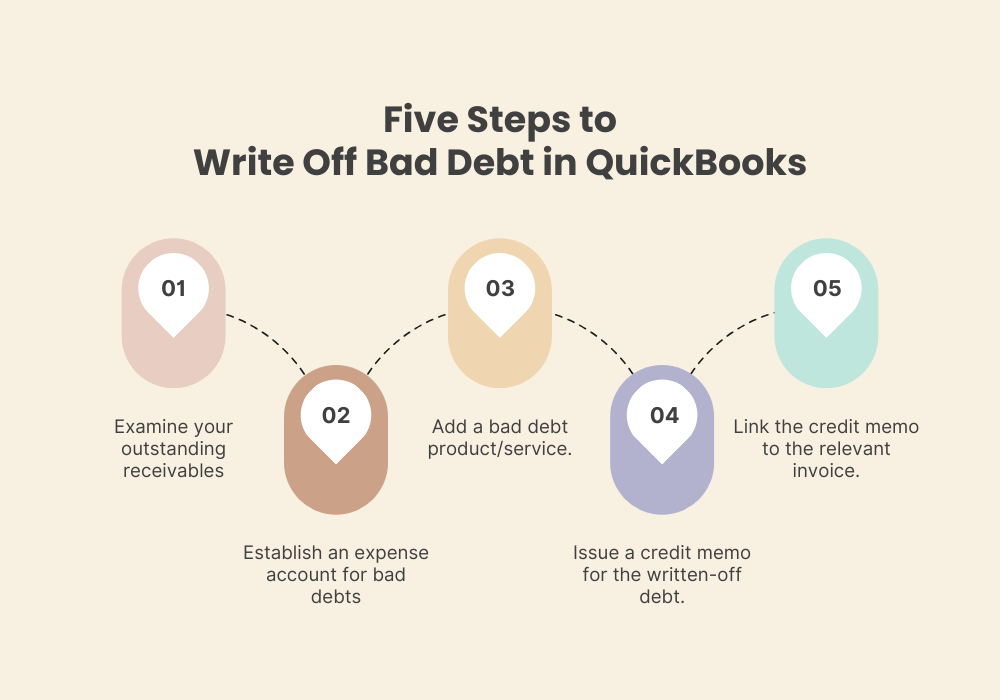

- Examine your outstanding receivables (aging accounts receivable automation);

- Establish an expense account for bad debts;

- Add a bad debt product/service;

- Issue a credit memo for the written-off debt;

- Link the credit memo to the relevant invoice;

- Consider generating a report on bad debts.

Q3: What are the steps to write off bad debt in QuickBooks Desktop?

In the desktop version of QuickBooks, the process involves:

- Adding an expense account specifically to track bad debt.

- Closing out the unpaid invoices by applying a discount (representing the bad debt) to them, and linking this discount to the bad debt expense account.

Q4: Why is it important to write off bad debt in QuickBooks?

Writing off bad debt in QuickBooks (or any other accounting software) is essential for maintaining accurate financial records. It ensures that your income statements and balance sheets accurately reflect your business’s financial status, aids in cash flow management, and ensures compliance with accounting standards.

Q5: Can I recover a bad debt after writing it off in QuickBooks?

If a customer pays after you’ve written off their debt, you can record the payment in QuickBooks. The process would involve reversing the write-off and recording the income as usual.

Q6: Is it necessary to consult a professional before writing off bad debt?

While QuickBooks makes it relatively straightforward to write off bad debt, consulting an accounting professional is advisable, especially for significant amounts. This ensures that all accounting and tax implications are properly addressed.

Q7: How does writing off bad debt affect my business’s taxes?

Writing off bad debt can have tax implications. Generally, bad debts can be deducted, reducing your taxable income. However, tax laws vary, so it’s important to consult with a tax professional for specific advice.

Q8: How often should I review my accounts receivable for potential bad debts?

Reviewing your Accounts Receivable in QuickBooks at least monthly is recommended to identify potential bad debts early. This helps take timely action to either collect the debt or write it off.

Q9: Can I prevent bad debts in my business?

While it’s difficult to completely prevent bad debts, you can reduce the risk by performing credit checks on new clients (if applicable), setting clear payment terms, and sending timely reminders for payments.

Q10: Does QuickBooks offer tools to help with bad debt management?

Yes, QuickBooks offers various tools and reports, like the Accounts Receivable Aging Detail report, that can help in identifying and managing bad debts effectively.

Navigating bad debt write-off in QuickBooks Online and Desktop: Closing thoughts

Writing off bad debt in both QuickBooks Online and QuickBooks Desktop is an essential process for maintaining the accuracy of your financial records. It ensures that your accounts receivable and net income reflect the true financial position of your business. The process differs slightly between the QuickBooks versions but serves the same critical purpose.

Staying vigilant about potential bad debts—by regularly reviewing accounts receivable in QuickBooks and understanding the signs of bad debt—can aid in early intervention and possibly prevent certain debts from becoming uncollectible. However, when prevention is not possible, QuickBooks provides a robust system to manage these financial realities.

Ultimately, the ability to efficiently write off bad debts in QuickBooks ensures that businesses can continue to focus on growth and profitability, secure in the knowledge that their accounting system accurately reflects their financial status.

Want to learn more about QuickBooks? Find out how to create an invoice in QuickBooks and how to reconcile accounts in QuickBooks with our comprehensive guides.