In the world of startups, each new venture represents a dream, a passion, and a solution to a problem. However, these bright ideas often encounter their first major hurdle even before they take off – the daunting financial challenges that come with launching a business. These challenges range from operational expenses and product development to marketing efforts, and much more.

Securing a business loan isn’t just about overcoming these challenges; it’s about laying down a solid foundation for the venture. Having a financial backup can accelerate growth, allow for scaling, and importantly, provide a safety net during the unpredictable initial phases of a startup. Without this crucial financial boost, many innovative ideas might never see the light of day. Thus, understanding how to access startup business loans, especially when you’re starting without money, becomes paramount.

This guide delves into strategies and insights that can lead to startup success, even in the absence of initial capital.

Elevate, expand, and thrive using our ecommerce intelligence platform. Dive into actionable insights now!

Understanding the basics of business financing

When embarking on an entrepreneurial journey, understanding the intricacies of business financing can mean the difference between a thriving enterprise and one that struggles to keep its doors open. Financing is the fuel that propels startups forward, allowing them to transform innovative concepts into tangible products and services. Here’s a deeper look into the essential elements of business financing.

Definition and types of startup business loans

Startup business loans are special types of loans tailored to meet the needs of startups and new businesses. Unlike traditional loans that might require an established business history or collateral, startup loans are designed to support ventures that might not have extensive assets or a long track record.

Term loans for a startup

Overview: Term loans are the most straightforward form of borrowing. Here, lenders provide startups with a lump sum amount. In return, the business agrees to pay back the principal along with interest over a designated period.

Benefits: For startups with a clear projection of their revenue streams and expenses, term loans offer predictability. Regular fixed payments allow for more straightforward budgeting and financial planning.

Ideal for: Startups looking to finance a particular project or expansion phase, where the ROI (Return On Investment) is relatively predictable.

Equipment financing for a startup

Overview: Equipment financing is tailored for startups that need to invest in machinery, technology, or other tools crucial for their operations. The equipment itself serves as collateral, offering lenders a safety net.

Benefits: This loan type often comes with competitive interest rates, given the reduced risk for lenders. Plus, startups can immediately deploy the equipment to generate revenue, essentially allowing the machinery to pay for itself over time.

Ideal for: Businesses in manufacturing, IT, or any sector where specific equipment can significantly enhance operational efficiency and revenue generation.

Lines of credit for a startup

Overview: Unlike the lump-sum structure of term loans, lines of credit offer startups the flexibility to access funds as and when they need them, up to a pre-defined limit.

Benefits: It’s the financial cushion every startup dreams of. Entrepreneurs only pay interest on the amount they draw, making it a cost-effective solution for uncertain cash flow scenarios.

Ideal for: Startups with fluctuating capital needs, such as those in seasonal industries or businesses that encounter sporadic growth spurts.

Microloans for a startup

Overview: Microloans, as the name suggests, are smaller in amount than typical loans. Often facilitated by non-traditional lenders or non-profits, these are designed for specific, short-term needs.

Benefits: Beyond just financial assistance, microloan providers often offer mentorship, training, and resources, turning the loan experience into a holistic growth opportunity.

Ideal for: Entrepreneurs who are at the nascent stages of their venture, or those who require a small amount of capital to bridge a temporary financial gap or finance a specific small-scale project.

Bottom line

The world of startup business loans is varied and vast, ensuring that there’s likely a financial solution tailored for every unique startup challenge. As with any financial decision, due diligence, research, and a keen understanding of one’s business needs are crucial to selecting the most suitable loan type.

The role of credit in financing your startup business

In the realm of business financing, credit stands as a silent gatekeeper, influencing opportunities and outcomes for entrepreneurs. Before diving deeper, let’s understand why credit is pivotal and how it intertwines with the success of startups and established businesses alike.

Personal credit: A founder’s financial fingerprint

For many lenders, a startup’s potential isn’t just seen in its business model or market niche—it’s reflected in the financial habits of its founder. Especially for newly launched ventures, where there’s little to no business history to assess, the personal credit score of the founder or business owner becomes a significant evaluation metric. It serves as a measure of the individual’s trustworthiness, financial responsibility, and past management of debts and obligations. For an entrepreneur, this underscores the need to maintain a clean personal financial record, as those early financing opportunities might hinge on their personal creditworthiness.

Business credit: The evolving financial identity of a startup

Just as individuals have credit profiles, so do businesses. As a startup matures and engages in its own set of financial transactions, it begins to carve out a distinct credit profile. This business credit score, separate from the owner’s personal score, becomes a testament to the company’s reliability in meeting its financial commitments. A robust business credit score can be a game-changer. Not only does it present the venture as a reliable entity, but it also opens doors to superior financing options tailored for businesses, often accompanied by more favorable terms and conditions.

Revenue-based financing vs. traditional business loans

In business financing, two prominent options emerge: revenue-based financing and traditional business loans. Each offers its own advantages and challenges.

Understanding revenue-based financing (RBF): Aligning with business rhythms

Revenue-based Financing (RBF) represents a dynamic approach to funding, tailored especially for the unpredictable journey of startups. Unlike conventional loans where fixed repayments are the norm, RBF takes a more adaptable route.

Businesses that opt for this model secure a loan, but instead of a rigid monthly repayment, they commit to returning a percentage of their future revenues. This percentage-based approach inherently links the repayment to the company’s performance, ensuring that during booming months, the business pays back more, and during slower months, less. Such flexibility is a boon for startups, particularly those with cyclical or fluctuating revenues, as it ensures that repayments don’t become a choking point during leaner periods.

Traditional business loans: The bedrock of business financing

Traditional business loans are typically characterized by their fixed terms as well as defined repayment schedules and often necessitate some form of collateral. Whether the interest rate is fixed or variable, businesses have a clear roadmap of their financial obligation over the loan’s tenure.

This predictability is both its strength and its potential limitation. While it offers businesses a clear path and the stability of knowing their monthly obligations, it might not provide the cushioning effect during revenue dips, which startups, especially in their nascent stages, might experience.

RBF vs traditional business loans: Navigating the choice for a startup

Choosing between RBF and traditional loans often boils down to a company’s risk appetite, growth predictions, and revenue stability. RBF, with its inherent flexibility, might seem attractive, but businesses need to factor in that if they experience a surge in revenues, the total repayment could significantly exceed what might have been repaid through a traditional loan.

On the flip side, traditional business loans, with their structured repayment plans, can be reassuring but may also exert undue pressure during lean patches. Startups, therefore, need to gauge their projected cash flows, growth trajectory, and risk tolerance to make an informed decision.

Revenue predictions and why they’re crucial for startups

For startups, venturing into the business world can often feel like setting sail in unpredictable waters. Revenue predictions serve as the compass for these journeys, offering insights into potential financial landscapes and guiding startups toward sustainable growth and stability. Understanding their significance is paramount for any budding entrepreneur aiming for success.

Strategic forecasting

When founders harness the power of strategic forecasting, they position their startups for proactive, rather than reactive, decision-making. A clear estimate of incoming revenue allows for meticulous budgeting. Resources can be channeled into areas with the highest anticipated returns, ensuring that every dollar spent is an investment in the company’s growth. This could mean ramping up R&D efforts to spearhead innovation, intensifying marketing campaigns to capture a larger market share, or even exploring potential areas for expansion.

Moreover, by grounding decisions in data-driven revenue predictions, startups can minimize risks. They can anticipate potential cash flow crunches, strategize around seasonal ebbs and flows, and make informed decisions about hiring or scaling operations.

Securing investments

Investors, especially those seasoned like venture capitalists or angel investors, are always on the lookout for signs of robust financial health and strategic foresight. This is where the power of accurate revenue predictions comes into play.

By showcasing a firm grasp of revenue predictions, startups signal a deep understanding of their market landscape. It suggests that the business isn’t just operating on passion or intuition alone; it’s grounded in data and informed analytics. Such an approach paints a picture of a startup that’s not only aware of its current standing but is also keenly attuned to potential future trajectories. This kind of foresight is invaluable, indicating a startup’s preparedness to pivot or adapt based on market changes.

A commitment to financial prudence, as demonstrated by solid revenue forecasting, conveys a level of maturity and professionalism. It reassures investors that the startup is not only visionary but also pragmatic – that it values sustainability alongside innovation. For an investor, this translates to reduced risks. A startup that understands its revenue streams, can anticipate challenges, and strategizes its growth accordingly is often considered a safer investment bet.

When startups bolster their pitches with accurate revenue forecasts, they essentially bridge the trust gap, offering investors a clear lens into their operational strategy and long-term viability. In a sea of promising startups, it’s this blend of innovation, foresight, and financial acumen that can set a venture apart, making it a magnet for investment opportunities.

Strategies for startups to secure a business loan with no money

Starting a business without substantial capital in hand might seem daunting, but it’s far from impossible. The financial landscape offers several avenues to secure funds, even if an entrepreneur begins with empty pockets. Here, we’ll unpack some of the key strategies entrepreneurs can employ to obtain that all-important funds.

“For a comprehensive overview of business loans and how they can benefit startups, explore our in-depth guide on Square loans and PayPal Business Loans. It provides valuable insights into PayPal’s financing solutions.

SBA (Small Business Administration) loan

The Small Business Administration, or SBA, stands as a beacon for small business aspirations in the U.S. Although this governmental agency doesn’t lend money directly to entrepreneurs, it plays a crucial role by guaranteeing loans. This backing significantly reduces the associated risks for private money lenders, making them more inclined to offer loans.

The benefits of SBA loans are manifold. Firstly, they generally come with extended repayment durations, ensuring businesses aren’t strained with hefty monthly payments. Secondly, the interest rates associated with SBA loans are often lower than those of conventional loans. Furthermore, the prerequisite down payments are usually modest, providing an accessible route for those with limited capital.

To tap into these benefits, prospective borrowers should initiate their journey by consulting the official SBA website. Here, one can acquaint oneself with the diverse loan offerings, the stipulated eligibility criteria, and the standardized application procedures. Additionally, local SBA offices can provide personalized guidance tailored to individual business requirements.

ACH loans

In the financial jargon, ACH stands for Automated Clearing House. ACH loans are an emergent form of short-term financing where the repayments are automated, occurring daily or weekly directly from the borrower’s bank account.

The appeal of ACH loans lies in their speed. These financing solutions often promise swift approvals and fund disbursals. Additionally, loan eligibility is determined by a company’s daily bank transactions. Thus, they serve as an ideal fit for businesses with consistent daily revenues but might be asset-light.

However, every coin has two sides. ACH loans, while being expedient, typically come with a higher interest tag. As such, businesses need to conduct a meticulous cost-benefit analysis. It’s imperative to ensure that the frequent deductions don’t impede the company’s financial health.

Revenue-Based Financing (RBF)

RBF is an agreement between the startup and the lender where the company borrows a certain sum and commits to paying it back as a percentage of its future revenues. This setup offers a distinct advantage: repayments are intrinsically tied to the company’s performance. During periods of booming sales, repayments increase, while during leaner times, the repayments decrease proportionally. This inherent flexibility can ease the cash flow burdens startups frequently face, ensuring that repayments never become insurmountably hefty in challenging times.

Yet, it’s this very flexibility that also presents a possible drawback. If a startup’s revenues grow exponentially, the total repayment under RBF can far exceed what might have been repaid under a more traditional fixed-term loan. In essence, the cost of capital might be higher in the long run.

However, the appeal of RBF often lies in its accessibility. For startups with convincing sales forecasts and a clear pathway to revenue generation, RBF provides an avenue to access capital without diluting ownership, as would be the case with equity financing. It thus bridges the financing gap, allowing startups to fund their growth ambitions based on the strength of their business model and market potential, rather than just their current assets.

Equity financing

At its core, equity financing involves startups offering up a stake in their company’s ownership as a trade-off for receiving much-needed capital. Venture capitalists and angel investors are frequently the key players in this arena, willing to inject significant sums into promising ventures in return for an equity share.

Several compelling motivations draw startups towards this type of funding. Foremost among these is the ability to secure sizable financial backing without the immediate pressure of repayments that traditional loans entail. But the appeal doesn’t stop at money alone. Investors, especially those with a rich industry background, often bring a wealth of additional assets to a startup. Their vast networks, experience, and industry insights can be invaluable. Their association with a startup can also act as a badge of credibility, making further rounds of funding easier and attracting potential partners or clients.

However, like all choices, equity financing comes with its set of trade-offs. The most evident is the dilution of ownership. As entrepreneurs offer up equity, they’re parting with a slice of their company, which might later translate to reduced control over major decisions. Additionally, the very nature of investor involvement can sometimes pivot the company’s primary objectives. Instead of focusing on long-term, organic growth, there could be a push towards rapidly scaling and achieving quick returns to satiate investor expectations.

Crowdfunding

Crowdfunding has firmly established itself as a viable financial lifeline for startups, especially those operating on a shoestring budget. This funding avenue is diverse, with various types including reward-based platforms like Kickstarter, where backers receive products or perks in return for their pledge; equity-based platforms like SeedInvest, transforming backers into shareholders; peer-to-peer lending platforms like Prosper; and donation-based platforms like GoFundMe for projects with a philanthropic angle.

One of the standout advantages of crowdfunding, beyond funding itself, is its capacity to validate business ideas. A successful campaign speaks volumes about market demand, providing startups with invaluable feedback and often attracting potential investors’ eyes. Furthermore, these campaigns foster a strong sense of community, turning early supporters into brand ambassadors who champion and promote the startup’s offerings.

However, while cost-effective compared to traditional fundraising, crowdfunding is not without challenges. A campaign’s success hinges on its presentation, clear messaging, and continuous backer engagement. Furthermore, startups must deliver on their promises to maintain their reputation. Despite these challenges, with thorough planning and a compelling narrative, crowdfunding can be a transformative tool for cash-strapped startups, offering not just funds but also a dedicated community of supporters.

Grants and competitions

Grants and competitions stand out as two non-traditional yet highly effective methods for startups to secure much-needed capital without accruing debt or relinquishing equity. Both avenues come with their distinct advantages and caveats.

Grants

Grants are sums of money provided to businesses or individuals for a specific purpose, and unlike loans, they typically don’t need to be repaid. These are frequently provided by government agencies, non-profit organizations, and corporations. The allure of grants is undeniable: free capital. However, securing a grant isn’t as simple as just asking. Grants are often targeted toward specific industries, innovations, or demographics. For instance, there are grants dedicated to green technologies, women or minority-led startups, and specific research areas. Applying for them involves meeting stringent criteria, showcasing the feasibility and potential of the business idea, and often requires rigorous documentation and reporting. While the process may be laborious, the benefits go beyond just monetary. Being awarded a prestigious grant can also provide a startup with credibility and open doors to other funding opportunities.

Competitions

In recent years, the startup ecosystem has seen a surge in competitions and pitch events. Universities, corporations, and even cities or countries host these events to stimulate innovation and attract talent. Competing in these events requires startups to refine their business ideas, polish their pitches, and often showcase prototypes or actual results. Winners usually walk away with cash prizes, and occasionally, offers of investment. Beyond the obvious monetary gain, such competitions also provide startups with a platform to gain visibility, network with industry experts, and receive feedback. Even startups that don’t win can benefit from the exposure and the feedback they receive.

Asset-Based Lending

While asset-based lending (ABL) typically requires collateral, it doesn’t necessarily have to be in the form of money. At its essence, ABL allows businesses to leverage the inherent value of their tangible assets to obtain much-needed funding. Instead of cash flow or credit scores dominating the lending decision, the emphasis here is on assets like inventory, equipment, and accounts receivable.

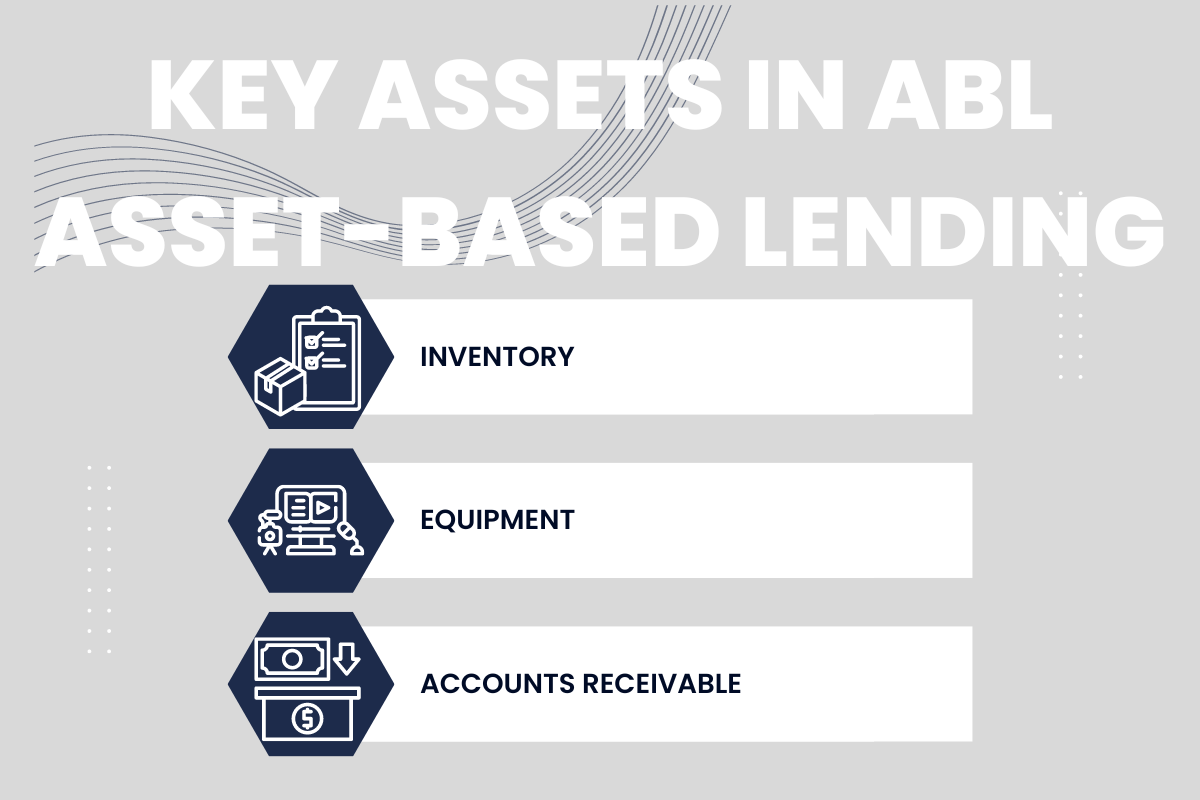

Key assets in ABL:

- Inventory: Every unsold item symbolizes potential capital. Recognizing this, asset-based lenders often approve loans using inventory as collateral. Nevertheless, due to depreciation risks, the loan’s value remains a fraction of the total inventory.

- Equipment: Essential operational assets, from machinery to vehicles, can be powerful collateral. Their loan value depends on the asset’s worth and its rate of depreciation.

- Accounts Receivable: Expected payments showcased in outstanding invoices can be compelling for lenders. If a startup has a record of timely client payments, its receivables are viewed as reliable assets.

However, ABL isn’t without its challenges. The credit offered typically falls short of the full asset value, cushioning the lender against potential losses. And if a default occurs, asset liquidation can be a tricky affair.

Still, for startups with tangible assets but perhaps inconsistent revenues or shaky credit, ABL can be an efficient way to navigate immediate financial needs, setting the stage for sustained growth and innovation.

How to make a compelling business plan for your startup loan?

At the very heart of any compelling business loan application lies a well-crafted business plan. Think of it as more than just a document; it’s the strategic and operational compass for your venture. This plan does more than just detail daily operations—it outlines your ambition, painting a clear picture of the pathway you’ve charted for your business to navigate challenges and seize opportunities.

Going beyond the basics

A mere summary won’t do. Your business plan should be comprehensive, encompassing more than just the rudimentary details of your business. It’s crucial to dive deep into a thorough market analysis, articulate descriptions of the products or services you offer, elucidate the organizational hierarchy, and provide meticulous financial forecasts. It’s also your platform to shine a spotlight on the unique facets of your business. Whether it’s a distinctive selling point, a proprietary method, or a niche in the market you’ve discovered, this is your moment to highlight what makes your venture stand out.

A plan crafted with the lender in mind

Understanding your audience is key. When drafting a business plan, it’s vital to remember that lenders come with their own set of priorities and apprehensions. Instead of merely presenting information, proactively address any foreseeable risks associated with your business. But don’t stop there—showcase your strategies to counteract these challenges. When you can offer concrete solutions to potential obstacles, it not only underscores your business acumen but also highlights your proactive approach, reassuring lenders of your commitment and foresight.

Business loan for a startup with no money: Closing thoughts

Navigating the financial landscape as a startup requires a blend of diligence, foresight, and adaptability. In a world abundant with choices, finding the perfect business loan isn’t just about the immediate injection of funds—it’s about carving out a sustainable financial pathway that supports growth, fosters innovation, and withstands challenges.

While the journey to secure the right financing may seem daunting, with the right resources, research, and mindset, entrepreneurs can turn financial decisions into strategic steps toward lasting success. As you embark on this crucial aspect of your entrepreneurial journey, remember that every choice you make lays a brick in the foundation of your venture’s future. Choose wisely, and the road ahead will not only be smoother but also more rewarding.

.png)