Square has risen to prominence as a comprehensive payment solution, offering a range of tools for businesses, including point-of-sale systems, business loans, ecommerce tools, and more. Square’s primary offering is credit processing. It is critical to understand the Square credit card fee structure and how it might impact your business.

Credit card processing fees can significantly influence a business’s bottom line. Hence, it’s essential for business owners to grasp these costs and how to manage them best. This article aims to shed light on the Square credit card fee system, enabling you to make an informed decision about whether it’s the right fit for your business.

This article is meant to explore Square’s credit card fees in-depth, aiming to provide businesses with the information they need to make an informed financial decision. However, every business is unique, and it’s always a good idea to consult with a financial advisor or conduct your own research to ensure you’re choosing the best solution for your specific needs.

Overview of credit card fees in general

Credit card fees are a common expense in the business world, with merchants needing to pay these fees every time a customer chooses to pay with a credit card. While credit card fees might seem straightforward, there’s quite a bit of complexity beneath the surface that can impact your business’s overall profitability.

Credit card fees are charges paid by payment processors whenever a credit card transaction occurs. These fees are designed to cover various costs that the processors incur, such as the cost of processing the transaction, combating potential fraud, providing customer service, and more.

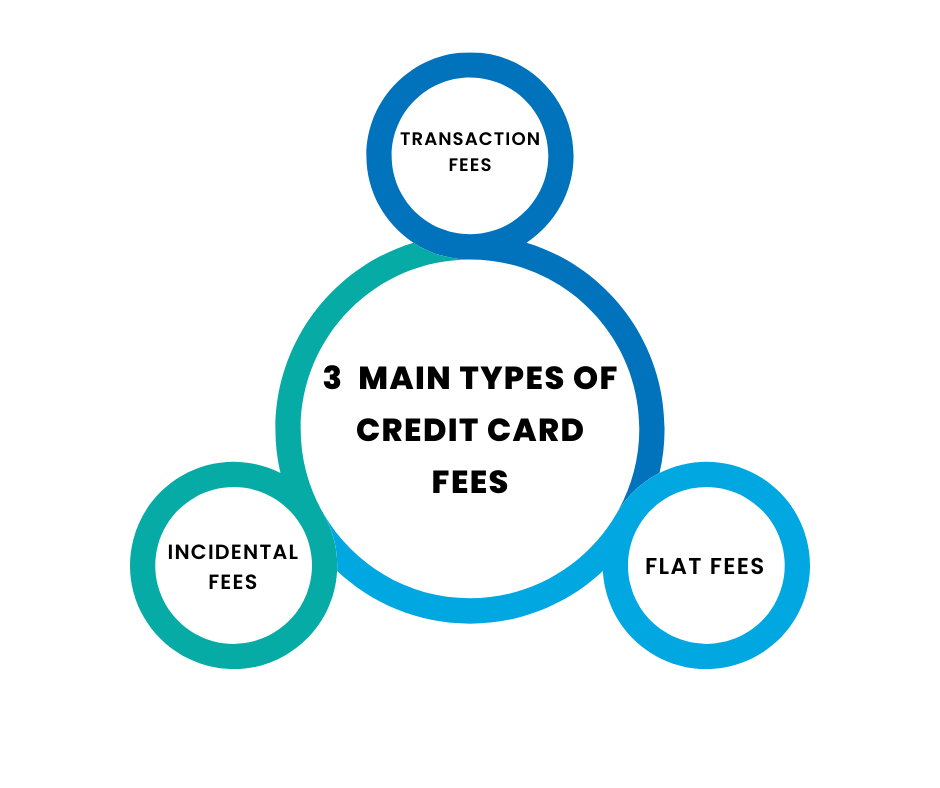

There are three main types of credit card fees:

- Transaction fees. These are the charges applied each time a credit card is used for a transaction. It typically involves a percentage of the transaction value and a fixed per-transaction fee.

- Flat fees. These fees are the fixed costs that you pay for the service of credit card processing. They include monthly fees, payment gateway fees, terminal fees, etc.

- Incidental fees. These fees are less predictable and can be triggered by specific events or actions, such as chargebacks, non-sufficient funds, or network access fees.

The impact of these fees on a business can be significant, particularly for small businesses with thin profit margins. Understanding these costs and how to mitigate them is essential for maintaining a healthy bottom line.

Transaction fees

Transaction fees are the costs incurred whenever a credit card transaction takes place. These fees are the most common type of credit card processing costs and are an essential factor for Square businesses to consider when selecting a payment processor.

Typically, transaction fees consist of two components: a percentage of the transaction total and a fixed fee. For instance, a processor might charge a rate of 2.6% + 10¢ for every credit card transaction. In this case, if a customer purchases $100 worth of goods, the business would pay $2.60 (2.6% of $100) plus an additional 10 cents, making the total fee $2.70.

Transaction fees are a way for payment processors and credit card networks to recoup the costs associated with facilitating the transaction. These costs include the risk of fraud, the technology to process the transaction securely, and the customer service provided by the payment processor.

Variations in transaction fees

Transaction fees can vary significantly depending on several factors:

- Card type. Premium credit cards, rewards cards, and international cards often have higher interchange fees, which can lead to higher overall transaction fees.

- Transaction method. In-person transactions where the card is physically present typically have lower transaction fees because they are less risky. In contrast, online transactions or transactions where the card is manually keyed in have higher fees.

- Business type and size. Different industries have different levels of risk, which can affect interchange fees. Furthermore, larger businesses with high transaction volumes can often negotiate lower processor markups.

- Payment processor. Different payment processors have different fee structures. Some use a flat-rate model (like Square), while others use a tiered or interchange-plus model, which can result in varying fees depending on the specific transaction.

Flat fees

Flat fees, also known as fixed fees, are a type of cost associated with credit card processing. Unlike transaction fees, which vary depending on the value of each transaction, flat fees are predictable, consistent costs that do not change from month to month. They cover various services and features provided by your payment processor.

Flat fees are predetermined, fixed costs that businesses pay to their payment processor. These fees can cover a wide range of services, including monthly account maintenance, payment gateway access, terminal rental, PCI compliance, and more.

For example, a payment processor might charge a flat monthly fee of $20 for access to their services. Regardless of the volume or value of transactions processed, this $20 fee remains the same every month.

Types of flat fees

There are several different types of flat fees that a payment processor might charge:

- Monthly account fee. This is a fee for simply having an account with the payment processor. It’s akin to a membership fee that gives you access to the processor’s services.

- Payment gateway fee. If your business operates online, you’ll likely need a payment gateway, which is a service that securely transmits transaction data from your website to the payment processor. Some processors charge a monthly fee for this service.

- Terminal lease or rental fee. If you lease or rent a card reader or point-of-sale system from the processor, you’ll typically pay a monthly fee for that hardware.

- PCI compliance fee. The Payment Card Industry Data Security Standard (PCI DSS) is a set of security standards designed to ensure that all businesses that accept, process, store or transmit credit card information maintain a secure environment. Some processors charge a fee for helping your business maintain these standards.

- Additional service fees. If your payment processor offers additional services, like advanced reporting or dedicated customer support, they may charge an extra monthly fee for these services.

Incidental fees

In the context of credit card processing, incidental fees refer to costs that are not regular or predictable but instead arise due to specific events or scenarios. Unlike transaction fees, which apply to every transaction, or flat fees, which are fixed monthly or annual charges, incidental fees only occur under particular circumstances.

Incidental fees are triggered by specific events or actions related to your merchant account or payment processing activities. They cover a range of situations, from technical issues to customer disputes, and their cost can vary significantly depending on the payment processor’s pricing structure.

Types of incidental fees

There are numerous types of incidental fees that a payment processor might charge, including:

- Chargeback fees. When a customer disputes a charge and initiates a chargeback, the payment processor may charge a fee to manage the dispute resolution process.

- Non-sufficient funds (NSF) fees. If a business doesn’t have enough funds in its bank account to cover the cost of its payment processing activities, the processor might charge an NSF fee.

- Retrieval fees. If a customer disputes a transaction, the card issuer may request more information about the transaction. The payment processor might charge a retrieval fee to cover the cost of gathering and submitting this information.

- Batch payment fees. Some payment processors charge a fee each time the business submits a batch of transactions for processing.

- ACH and wire transfer fees. If a business wants to transfer funds electronically from one bank account to another, there may be a fee associated with this service.

- Card network fees. Credit card networks (Visa, Mastercard, etc.) sometimes charge their own incidental fees for certain situations, like international transactions, which are passed onto businesses by the payment processor.

What goes into average credit card processing fees?

Credit card processing fees are the costs businesses must pay to enable their customers to use credit and debit cards for purchases. These costs are paid to multiple entities involved in the process of authorizing, processing, and settling card transactions. The fees are typically broken down into three main categories:

- Interchange fees: These fees are set by the card networks (like Visa, MasterCard, Discover, and American Express) and are paid to the card-issuing banks. The interchange fees compensate the issuing banks for the risk and handling costs involved in processing card transactions. These fees vary based on a variety of factors, including the type of card used (credit or debit, rewards or basic, etc.), the transaction method (in-person, online, etc.), and the type of business accepting the card.

- Assessment or network fees: These are fees that the card networks charge for each transaction that uses one of their cards. They are usually a small percentage of each transaction.

- Payment processor’s markup: This is the fee that your payment processor (like Square, PayPal, or a traditional merchant services provider) charges for their services. This is where payment processors make their profit. The markup varies widely among providers and can be a percentage of each transaction, a flat per transaction fee, a monthly fee, or some combination of these.

On average, for a standard in-person transaction, businesses can expect to pay between 1.5% and 3.5% of the transaction value in total processing fees. However, the actual cost can vary depending on a multitude of factors, including the specific interchange rate of the card used, the type and volume of transactions a business processes, and the pricing model of the payment processor.

Some processors use a tiered pricing model, where different types of transactions are charged different rates, while others, like Square, use a flat-rate pricing model, where the same rate is charged for all transactions. There are also interchange-plus models, where the processor charges the interchange fee plus a fixed markup, and subscription models, where businesses pay a monthly membership fee plus a fixed per-transaction fee.

When evaluating credit card processing costs, businesses should consider all these components and understand their own transaction patterns and volumes to determine which pricing model will be most cost-effective for them. It’s also important to consider any additional fees, like chargeback or monthly account fees, which can add to the total cost of processing card payments.

Introduction to Square credit card fees

In today’s digital era, businesses of all sizes and industries are leveraging technology to accept customer credit and debit payments. One company that revolutionized the world of card payment processing is Square. Known for its ease of use, simplicity, and transparent pricing, Square business account offers a variety of solutions for businesses to accept card payments, both in-store and online. Square’s credit fees are central to its service, which is critical for businesses to understand when evaluating their options.

Square has adopted a flat-rate fee structure, which means that it charges the same fee for every card transaction, regardless of the card type or whether it’s a swipe, chip, or keyed-in transaction. This simple, predictable pricing structure is one of the features that has helped Square stand out in the payment processing landscape.

As straightforward as Square’s fees might seem, it’s still crucial for businesses to fully understand these costs and how they might impact their bottom line. The way your business operates—its sales volume, average transaction value, and even the types of cards your customers use—can all influence the overall cost of using Square.

Understanding Square credit card fees

Square credit card fees are the charges that businesses incur for using Square’s payment processing services. These fees allow Square to facilitate credit and debit card transactions, providing businesses with the technology and support needed to securely and efficiently accept customer card payments.

Square’s fee structure is characterized by its simplicity and transparency. Rather than using a complicated pricing model with different fees for different types of cards and transactions, Square charges a flat rate for all card transactions. This means that businesses pay the same fee whether they’re accepting a Visa, MasterCard, Discover, or American Express card and whether the transaction involves a swiped card, a chip card, or a manually keyed-in card number.

The specific fees that Square charges are as follows:

- For card-present transactions. These are transactions where the customer’s credit or debit card is physically present and is swiped, dipped, or tapped on a Square reader. The fee for such transactions is 2.6% of the transaction value plus 10 cents.

- For online and keyed-in transactions. These are transactions where the customer’s card details are entered manually or through an online portal. The fee for these transactions is 3.5% of the transaction value plus 15 cents.

- For Square invoices. If you’re using Square’s online invoice service, the fee is 3.3% of the transaction value plus 30 cents.

It’s important to note that these fees are deducted from the transaction total before the remaining funds are transferred to the business’s bank account. So, if a customer makes a purchase of $100, the business will receive the $100 minus the applicable Square fee.

Check our guide to learn more about Square fees.

Strategies to mitigate the impact of Square credit card fees

While competitive and transparent, Square’s credit card processing fees still represent a cost to your business. Therefore, it’s in your interest to use strategies to help mitigate these fees’ impact. Here are some strategies to consider:

1. Increase your average transaction value

Since Square charges a flat fee per transaction, businesses can reduce the effective rate of fees by increasing the average value of their transactions. Consider bundling products or services together, upselling, or promoting higher-value items to increase your average transaction amount.

2. Encourage debit card or cash payments

Debit card transactions often come with lower processing fees than credit card transactions. If possible, encourage your customers to use debit cards instead of credit cards. Additionally, promoting cash payments can entirely eliminate processing fees for those transactions.

3. Implement a minimum card payment

To mitigate the impact of fees on small transactions, consider implementing a minimum amount for card payments. However, be aware that this could potentially alienate some customers, so it’s important to strike the right balance.

4. Use Square’s Point of Sale (POS) system

Square’s POS system not only offers a seamless payment experience but also provides valuable sales data. You can use this data to understand your sales patterns better and identify opportunities to optimize your operations and reduce the impact of credit card processing fees.

5. Efficient tax handling

Credit card processing fees are tax-deductible for businesses. Make sure to keep track of these expenses and include them in your business tax filings to reduce your overall tax burden.

6. Regular fee assessment

Regularly review your transaction history and the associated fees. If you notice a significant cost increase, it might be time to revisit your payment processes or consider a different payment processor.

FAQ about Square credit card fees

Understanding the nuances of Square’s credit card fees can be challenging, and there are many common questions that businesses often have. Here, we will answer some of these frequently asked questions:

Are there any monthly fees associated with Square?

Unlike some other payment processors, Square does not charge any monthly fees. You pay only for the transactions you process. However, certain features and services, such as Square for Retail, Square Appointments, or Square for Restaurants, do carry monthly subscription fees.

Does Square charge more for premium credit cards?

No, one of the advantages of Square’s pricing structure is that they charge the same rate for all cards, whether they’re standard, premium, rewards, corporate, or international cards. This is not always the case with other payment processors, which can charge higher fees for certain card types.

What happens if a customer disputes a charge?

If a customer disputes a charge and it results in a chargeback, you’ll be subject to a $25 fee from Square. However, Square offers a dispute management system and provides guidance to help you respond to chargebacks. If the dispute is resolved in your favor, the $25 fee will be refunded.

Conclusion

Square’s credit card fees are an important consideration for any business considering using Square for payment processing. Square’s transparent, flat-rate fee structure can be an attractive feature, especially for small businesses that appreciate predictability and simplicity. However, as with any cost of doing business, it’s crucial to understand these fees and how they might impact your bottom line.

Consider the specifics of your business, including your average transaction value, sales volume, and the nature of your sales, when assessing whether Square’s fee structure is the best fit for you. Ultimately, the best payment processing solution is the one that aligns most closely with your business’s needs and supports your goals for growth and profitability.