PayPal handles a staggering share of online commerce, and it shows up on almost every ecommerce P&L for a reason. In 2025 alone, PayPal users completed 25.355 billion transactions, totalling a record $1.79 trillion in payment volume across roughly 36 million merchant accounts. Whichever way you slice it, that’s a lot of payouts getting into bank accounts, and a lot of bookkeeping that needs to go right.

The catch is that PayPal was built to move money, not to keep books. This guide is for ecommerce sellers, owners, and the controllers and accountants – anyone looking at a PayPal balance, a QuickBooks register, and a Shopify report and wondering why none of the three agree.

We’ll cover what PayPal is from a bookkeeping perspective, the report you should be pulling every month, how transactions land in your books, the gotchas distorting revenue, and how to choose between manual entry, native bank feeds, and automation tools.

TL;DR

- PayPal doesn’t do your accounting: It provides reports, but you still need tools like QuickBooks Online or Xero to properly record revenue, fees, transfers, and balances.

- PayPal is more complex than typical processors: It holds balances, mixes funding sources, and introduces timing, FX, and refund differences that standard bank feeds often miss.

- Clean setup makes everything work: Treat PayPal as its own bank account, track fees separately, use clearing accounts when needed, and reconcile using the Balance Affecting report.

- Automation depends on volume: Manual entry works for very small volumes, native feeds for simple setups, and automation tools for multi-channel and/or high-volume businesses.

- Good PayPal accounting drives better decisions: Accurate data enables channel profitability analysis, real cash visibility, and smoother audits, funding, or exits.

What is PayPal accounting?

For most ecommerce sellers, PayPal accounting covers four overlapping jobs:

- Recording sales received via PayPal as revenue

- Breaking out PayPal’s processing fees as an expense

- Treating transfers between PayPal and the operating bank account as transfers, not income

- Reconciling the PayPal balance against what the books say it should be at the month-end

A common starting question is whether PayPal does any of this for you, and the short answer is no. PayPal generates transaction reports, payout summaries, and tax-time documents like the 1099-K, but it doesn’t keep your books.

These reports are inputs to the bookkeeping process, not a substitute for it. To track revenue, expenses, and cash position properly, you still need an accounting system – QuickBooks Online, Xero, NetSuite, Sage Intacct, etc. – with PayPal connected to it.

Learn how to sync PayPal transactions in QuickBooks Online.

Why is PayPal harder to bookkeep than a regular merchant account?

Most payment processors take card payments, deduct a fee, and deposit the net to your bank a day or two later. PayPal is structurally different. It carries a running balance like a checking account, deducts its fee before depositing the net somewhere else like a payment processor, pays vendors directly from that balance like a credit card, and processes income from multiple sales channels (your website, Shopify, eBay, Amazon, invoicing) like a gateway, often all in the same week.

Each of these behaviours needs different bookkeeping treatment, and PayPal’s standard transaction list shows them in a way that flattens the differences.

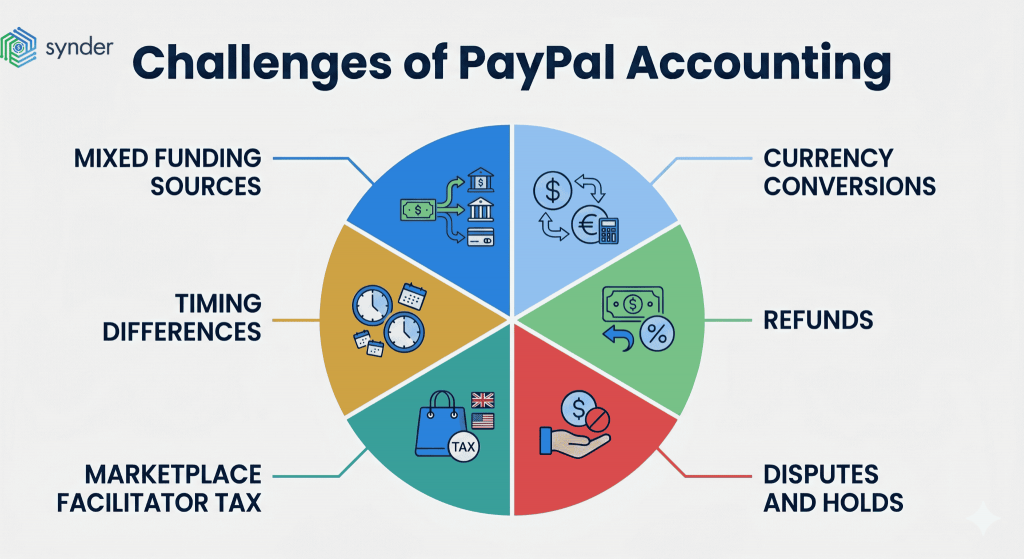

Here’s what confuses sellers:

- Mixed funding sources. A single payment from PayPal can pull from your PayPal balance, a linked credit card, or a linked bank account, and sometimes a mix of all three on one transaction. The accounting impact is completely different in each case, but PayPal’s transaction list shows them all the same way.

- Currency conversions that don’t cross the bank feed. If a US seller takes a payment in EUR, PayPal converts internally, and the conversion event never appears as a deposit in any bank account. It only shows up inside PayPal, which means QuickBooks bank feeds miss it entirely, and your books end up off by the FX gain or loss.

- Refunds that don’t reverse cleanly. A partial refund might span two months, affect the PayPal balance differently from the original sale, and then re-emerge in a future payout net of the original fee. Matching that back to the original invoice manually is slow.

- Disputes and holds. PayPal can freeze funds for days or weeks during a dispute, then release or claw them back. Those movements affect your real cash position but rarely look like normal expenses or revenue.

- Marketplace facilitator tax. In some US states, PayPal collects and remits sales tax on your behalf for marketplace sales. The tax shows up in your PayPal data, but it’s not your liability, and recording it as your own payable will overstate what you owe.

- Timing differences. A customer pays on Tuesday, PayPal holds the funds until Wednesday, you transfer to your bank on Thursday, and the bank clears it on Friday. Four different dates, one transaction, depending on which side you’re looking from.

Expert lens

Most guidance says to treat PayPal as a bank account, and operationally, that works. But for understanding edge cases, experienced ecommerce accountants use a different mental model: PayPal acts more like an escrow agent. Once you view PayPal as money owed to you, not as cash already in your account, the accounting becomes clearer. Held funds are receivables, not expenses, and chargebacks reverse prior inflows, not new losses. This is what clearing accounts reflect: PayPal owes you money, pays it out, and any remaining balance signals something that needs attention.

Settings inside PayPal that improve your books

It’s usually assumed that PayPal is configured the way it’s shipped out of the box. However, it isn’t, and a handful of PayPal-side settings make the bookkeeping side cleaner without requiring any changes to your accounting software. Practitioners running PayPal-heavy clients tend to enforce these as a matter of policy at onboarding:

- Default funding source set to a linked bank or credit card, not the PayPal balance. When PayPal pulls vendor payments from the balance, the books require manual transfer entries to track where the money went. Setting a bank or card as the default means every outbound payment shows up as a normal bank or credit card charge in the accounting feed, with no extra reconciliation step.

- Auto-transfer the PayPal balance to your operating bank daily. Cash held in PayPal earns no interest and is exposed to account-restriction risk if a transaction triggers a review. Daily auto-sweep also keeps the PayPal balance close to zero, which speeds up month-end reconciliation by reducing timing-related variance.

- Separate PayPal accounts for income and expenses where possible. Some bookkeepers require ecommerce clients to maintain one PayPal account for incoming customer payments and a separate one for outgoing vendor payments. The arrangement doubles the number of accounts to reconcile but eliminates the most common categorization error – a customer payment immediately consumed by a vendor charge, leaving the bookkeeper to untangle income, expense, and netting after the fact.

- Enable two-factor authentication and limit API access. Although this is a security setting rather than a strictly bookkeeping one, practitioners flag it because compromised PayPal accounts create some of the worst reporting cleanups – unauthorized transactions interleaved with legitimate ones are extraordinarily hard to reconcile after the fact.

- Confirm your PayPal account is a business account, not personal. Personal accounts come with stripped-down reporting (the Balance Affecting export is harder to access), no API access for most automation tools, and limited dispute protections. Many sellers start on personal accounts and never upgrade.

None of these are universal, and the right configuration depends on the business. But across the SMBs and ecommerce accounting communities that actively discuss this on LinkedIn and in CPA practice forums, the same five settings come up almost every time someone asks how to make PayPal less painful.

Related read: How to Create a PayPal Business Account.

PayPal report that makes reconciliation work

Most sellers default to the standard PayPal statement. It looks like a bank statement, so it feels right. The problem is that the standard statement doesn’t carry a running balance after each transaction, which means there’s no way to verify your accounting balance against PayPal’s actual balance at any point in time. You can see what came in and what went out, but you can’t see what the balance was on a given date.

The report that solves this is the Activity Download with the transaction type set to “Balance Affecting”, exported as CSV. It’s available inside any business PayPal account under Activity → All Reports → Activity Download. For personal accounts being used for business (still common among smaller sellers), it’s located a couple of clicks deeper, under Activity → Statements → See more reports → Activity Download.

The Balance Affecting filter strips out everything that didn’t move your PayPal balance, leaving you with the events that should appear in your books. Each row shows:

- The gross amount

- The PayPal fee

- The net amount

- The running balance after that transaction

It also separates currency conversions and refunds as their own line items, which the standard bank feed often skips.

Once you have the CSV, hide the columns you don’t need (PayPal exports a lot of metadata), so the gross, fee, net, balance, and transaction-type columns line up next to each other. Sort by type to find every refund and currency conversion in the period, because those are the entries most likely to be missing from your accounting software.

This single report is what experienced bookkeepers reach for when reconciling PayPal in QuickBooks Online or Xero, and it’s the report most clients should be sending their accountant at month-end alongside the standard statement.

Setting up PayPal correctly in your accounting software

The setup pattern is the same across most accounting systems – QuickBooks Online, Xero, NetSuite, Sage Intacct, and Puzzle. The labels and screens differ, but the underlying chart-of-accounts moves are identical. Here’s the sequence to follow at the start of any engagement, with QuickBooks Online and Xero shown as examples.

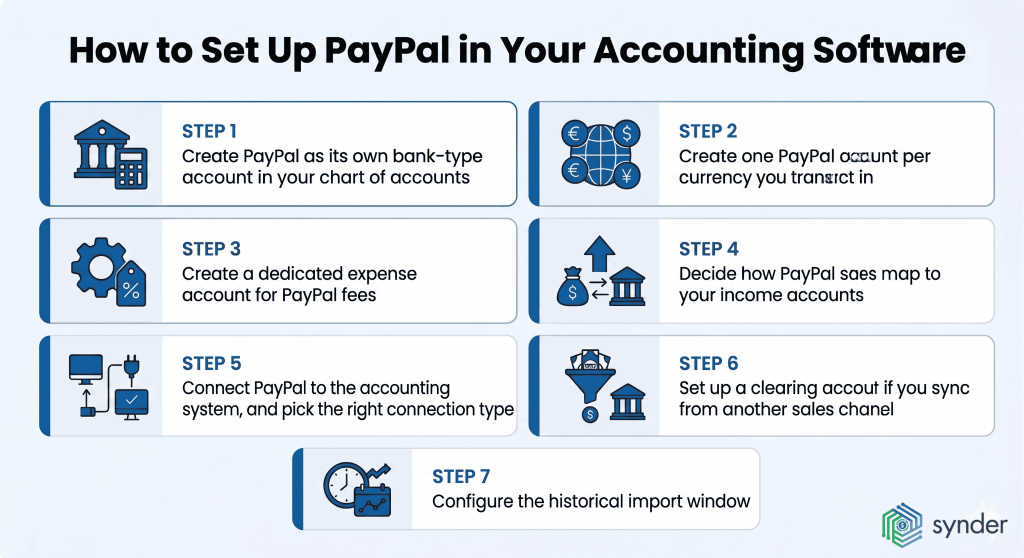

Step 1: Create PayPal as its own bank-type account in your chart of accounts

Go into your accounting software and add a new bank account called “PayPal – Operating” (or similar) with the correct base currency. Don’t categorize it as “other current asset,” as a payment method, or fold it into your operating bank. It needs to be a bank-type account, so it gets its own register, its own reconciliation screen, and its own opening balance. In QuickBooks Online, for example, this is located under Accounting → Chart of Accounts → New → Bank. In Xero, Accounting → Chart of Accounts → Add Bank Account.

Step 2: Create one PayPal account per currency you transact in

If you take payments in multiple currencies and PayPal holds separate balances per currency, each one needs its own bank account in your books – PayPal – USD, PayPal – EUR, PayPal – GBP. They don’t share a register because the FX rate moves between them, and combining them produces unreconcilable balances. Multi-currency must be enabled in the accounting software first.

Step 3: Create a dedicated expense account for PayPal fees

Add an expense account called “PayPal Fees” (or “Merchant Fees” / “Payment Processing Fees” if you want to consolidate across processors) for recording the fee side of every PayPal transaction. Without a dedicated fee account, fees either get lost in cost of revenue or, worse, are never recorded at all because the bank feed only shows the net deposit.

Step 4: Decide how PayPal sales map to your income accounts

You have two choices:

- Map PayPal sales to your general sales/revenue account and use platform tags, classes, or tracking categories to separate PayPal from other channels in reporting (the approach most accountants prefer).

- Create a separate “PayPal Sales” income account or sub-account for cleaner P&L visibility at the cost of more rows in your chart of accounts.

Step 5: Connect PayPal to the accounting system, and pick the right connection type

Most accounting systems offer at least two ways to connect PayPal. In QuickBooks Online, you can choose between the legacy “PayPal Bank” feed and the “Connect to PayPal” app – the latter posts richer transaction details and breaks out the gross sale and the fee automatically as separate lines. In Xero, the equivalent is the direct PayPal feed paired with a clearing account. NetSuite, Sage Intacct, and other ERPs typically rely on third-party connectors. Whichever path you choose, confirm the connection brings gross sales to revenue and PayPal fees to expense as separate entries, not a single net line.

Step 6: Set up a clearing account if you sync from another sales channel

If PayPal is paired with Shopify, Amazon, eBay, or another channel that already feeds sales into your accounting system, you need a clearing account to prevent double-counting. The Shopify side creates the receivable in the clearing account; the PayPal side settles it. Without this, the same sale gets recorded once from Shopify and again from PayPal, inflating revenue.

Step 7: Configure the historical import window

When you first connect PayPal, both QuickBooks Online and Xero let you backdate the import – QuickBooks’s native connector goes back up to 18 months, and Xero’s varies by feed provider. NetSuite and Sage Intacct integrations vary by connector, so check before relying on a specific cutoff. If you’re cleaning up books for a prior year, set the start date carefully. Once you’re out of range, you’re back to manual CSV import for any earlier period.

When you get these seven steps right, the rest of the workflow – recording transactions, reconciling, handling fees and refunds – becomes mechanical.

Read about reconciling PayPal transactions in Xero.

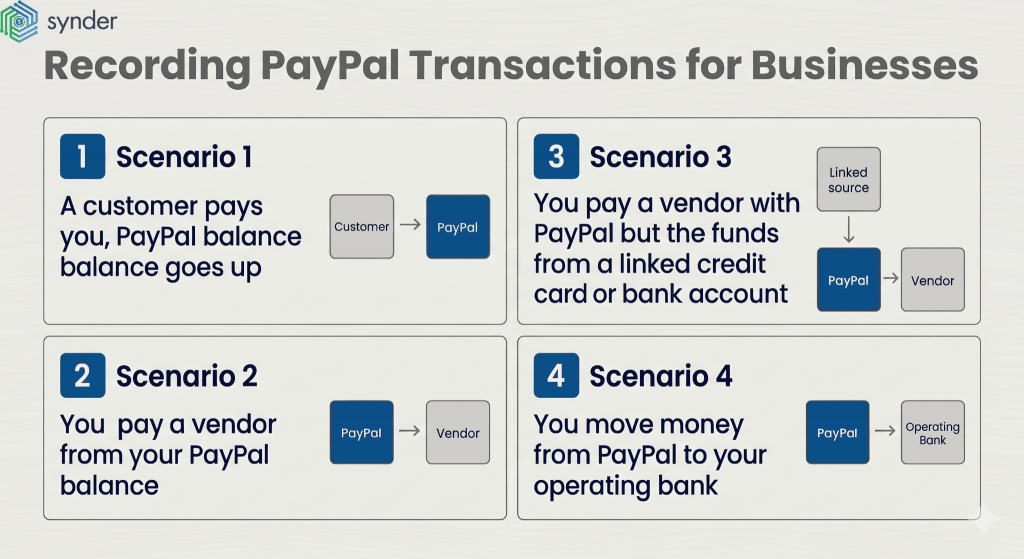

Recording PayPal transactions: the four scenarios that cover 95% of activity

Most of the bookkeeping pain on PayPal comes from a handful of scenarios that look similar in the bank feed but require different treatment. Working through them one at a time makes the whole workflow clearer.

Scenario 1: A customer pays you, PayPal balance goes up

This is the easy one. The customer pays $100, PayPal takes its $3.98 fee (the standard 3.49% + $0.49 rate for US online checkout), $96.02 lands in your PayPal balance.

In QuickBooks, the Connect to PayPal feed will post a sales receipt for the gross $100 to revenue, and a separate expense for $3.98 to PayPal Fees. The net $96.02 lands in your PayPal bank account. You click “Add,” and it’s done.

In Xero, you match the $100 sales invoice (if you generated one) against the $96.02 PayPal deposit and the $3.98 fee in the same reconciliation step.

Scenario 2: You pay a vendor from your PayPal balance

It goes against your PayPal balance, and no other account is involved. Categorize it as you would any expense, like Office Supplies, Software, Contractors, whatever applies, and add it. The clue that this scenario is in play: there’s no related credit-card or bank funding line in the same transaction.

Scenario 3: You pay a vendor with PayPal, but the funds come from a linked credit card or bank account

This is the one that creates duplicate transactions if you handle it from the wrong side. PayPal pulls $300 from your linked credit card, then pays the vendor. You’ll see two related lines: one in your credit card register showing the charge, and one in PayPal showing the payment. They’re the same money moving through PayPal as a pass-through.

The cleanest workflow, and the one that gives the most consistent matching results in QuickBooks Online, is to start from the credit-card side:

- Find the credit card transaction.

- Click “Transfer” (not “Add”), and transfer it to your PayPal bank account.

- Go to the PayPal side, where QuickBooks will already be showing a found match for the transfer.

- Click “Match.”

- Categorize the actual expense (Software, Subscriptions, etc.) as you normally would.

Doing the transfer in the opposite direction – initiating from the PayPal side first – is technically possible, but the matching is less reliable, and you’ll spend more time chasing duplicates.

Scenario 4: You move money from PayPal to your operating bank account

This is a transfer between two accounts you own, not income. Record it as a “Transfer” in QuickBooks (or “Transfer to another account” in Xero) from PayPal to Checking. Both bank feeds wil show the transaction, and you match on the receiving side. Forgetting this and categorizing the deposit as Sales is the single most common source of inflated revenue on PayPal-heavy books.

| The pattern across all four: ask yourself where the money actually came from and where it went. If both legs of the movement are accounts you own, it’s a transfer. If one leg is a customer or vendor, it’s a sale or expense. PayPal is just the conduit. |

Manual entry vs native bank feeds vs automation tools

There are three main ways to get PayPal data into your accounting system. The right one depends almost entirely on your transaction volume, your channel mix, and how much time you’re willing to spend at month-end.

Manual CSV entry. Pull the Balance Affecting report each month, categorize each line, post journals or transactions in batches. Works fine for under 30 PayPal transactions a month. Beyond that, the time cost outpaces the cost of any tool.

Native bank feeds. Free, automatic, and built into QuickBooks Online (Connect to PayPal app) and Xero (direct PayPal feed). They handle the basics – gross to revenue, fee to expense, transfers – for straightforward single-currency activity. Their main weakness is the same set of edge cases identified earlier: multicurrency, refunds across periods, disputes, marketplace facilitator tax, and double-counting when another channel is also feeding into the same accounting file. Suitable for low-volume single-channel sellers.

Automation tools. Third-party apps that connect PayPal to your accounting system and post entries on your behalf, working through a clearing account so PayPal payouts can be matched cleanly to bank deposits. They generally use one of two approaches – sometimes both, configurable per integration:

- Individual transactions. Each PayPal transaction lands in your books as its own entry, with full detail – customer, product, line items, tax, fees, refunds. Useful when you want order-level visibility in the accounting system, when you’re tracking inventory and COGS at the SKU level, or when you need open invoices to close automatically as customer payments come in.

- Consolidated journal entries per chosen period or payout. A day’s, week’s, month’s, or payout’s worth of PayPal activity is posted as a single journal entry per platform, broken out by sales, fees, refunds, taxes, and adjustments. Useful at higher volumes, in multi-channel setups where order-level detail already lives in another system (Shopify, Amazon), and for accounting teams that prefer a clean general ledger over thousands of individual entries.

As an example, Synder connects PayPal to QuickBooks Online, Xero, NetSuite, Sage Intacct, or Puzzle and supports both approaches above, configurable per integration. On the PayPal side specifically, it imports sales, processing fees, refunds, payouts, multicurrency conversions, dispute holds and reversals, and marketplace facilitator tax – the categories that native bank feeds typically miss – and posts them through a clearing account so the PayPal payout matches the bank deposit at month-end.

Beyond PayPal, Synder connects to 30+ other sales and payment platforms, such as Shopify, Amazon, Stripe, Square, and eBay, among them, which matters for multi-channel sellers who’d otherwise need a separate tool per channel.

Real-world case study

An ecommerce meal prep enterprise running 30+ locations across New York, with QuickBooks Online connected to Shopify and PayPal, cut daily reconciliation from 3–4 hours of manual work down to 30–45 minutes, saving 70+ hours every month and processing 100,000+ transactions automatically.

Before, growth came with a cost. Each day ended with hours of manual reconciliation, limited visibility into performance by store or county, and fees from Shopify and PayPal scattered across different workflows. It worked, but only with constant effort.

After, the process became structured and automatic. Transactions synced in real time, fees were categorized as they happened, and reporting across channels came together in one place, turning what used to be a daily task into a quick, predictable routine.

Key takeaways

For ecommerce businesses

- High transaction volume turns reconciliation into a time problem fast, so automation isn’t optional at scale.

- Clean PayPal setup (separate account, proper fee tracking) directly impacts margin visibility.

- Multi-channel reporting only works when data from Shopify, PayPal, and accounting is structured consistently.

- Time saved on reconciliation can be redirected to growth, not cleanup.

For accounting firms and bookkeepers

- Manual reconciliation doesn’t scale across high-volume ecommerce clients, and process design matters more than effort.

- Standardizing PayPal and Shopify workflows across clients reduces month-end variability and errors.

- Automated categorization and reconciliation improve both accuracy and client turnaround time.

- Better data structure enables advisory services (location-level, channel-level insights), not just bookkeeping.

If you want to see how this works against your own PayPal data, you can book a demo with Synder Team.

Choosing the right PayPal accounting method

The right setup depends less on the tool and more on how your business operates. Transaction volume, number of sales channels, and reporting needs all shape what will actually work day to day. The comparison below breaks down where each approach fits.

| Method | Best for | Handles multicurrency | Handles refunds/disputes | Time at month-end |

| Manual CSV import | <30 transactions/month | Manual journals required | Manual journals required | High |

| Native QBO/Xero PayPal feed | Single-channel, <500 transactions/month | Limited | Limited | Medium |

| Automation tool like Synder – individual transactions | Order-level detail, inventory tracking, lower volumes | Yes (varies by tool) | Yes (varies by tool) | Low |

| Automation tool like Synder – consolidated journal entries | Multi-channel, 500+ transactions/month | Yes | Yes | Lowest |

Why PayPal accounting matters beyond tax compliance

PayPal bookkeeping is often framed as a tax compliance task, but for ecommerce businesses, it’s much more than that. Clean PayPal reconciliation is what makes your financial reporting usable. If the data is messy, every downstream metric gets distorted, and decisions suffer.

There are three areas where this shows up most:

- Channel profitability: Most ecommerce businesses run multiple processors (PayPal, Stripe, Shopify Payments). To understand which channel actually makes money, you need clean separation of gross sales, fees, and refunds by channel. If PayPal activity is blended into a single revenue line and fees are buried, profitability analysis becomes guesswork. Once cleaned up, many businesses discover that channels they assumed were strong performers are barely breaking even, or the opposite.

- Cash flow visibility: PayPal can hold funds for up to 21 days, and longer in cases of disputes or account reviews. If the held amounts aren’t tracked separately, your books can overstate available cash. That gap directly affects operational decisions: inventory purchases, payroll timing, and ad spend. Treating held and pending funds as distinct balances gives a much more accurate view of what’s actually available to use.

- Funding and due diligence: When raising capital, applying for credit, or preparing for a sale, PayPal data gets reconciled against your books and 1099-K filings. Inconsistencies that didn’t matter day to day suddenly become critical. Cleaning up historical PayPal data under time pressure is costly and often uncovers deeper issues, such as missing transactions, misclassified fees, or FX differences, that can delay deals or impact valuation.

Overall, PayPal accounting determines whether your financials are reliable enough to run, scale, and eventually exit the business.

Conclusions on PayPal bookkeeping and accounting

PayPal feels more complex than other processors because it is doing three jobs at once. It acts like an account, a payment processor, and a vendor wallet, while most accounting setups expect those to be separate. Once you structure it properly, set it up as its own bank account, track fees separately, record transfers correctly, and reconcile against the right reports, everything becomes much clearer. Even areas like multi-currency, disputes, marketplace tax, or cross-period refunds can be handled in a structured way with the right setup.

The real decision is how much automation you need. Manual entry works for very low volumes, native feeds fit simple single channel setups, and automation tools make sense once you are running multi-channel at scale. None of these options is wrong. The issues usually come from using the wrong setup for your volume, which is what leads sellers to look for a better approach in the first place.

FAQ

How long should I keep PayPal records for tax purposes?

In the US, the IRS recommends keeping records that support items on a tax return for at least three years from the date you filed, and seven years if you wrote off bad debt or worthless securities. For PayPal, that means archiving the Balance Affecting CSV exports, payout statements, and 1099-K forms for each tax year. PayPal itself stores activity history for several years, but exporting at year-end gives you a stable, auditable copy in case you ever need to reconstruct a period.

Do PayPal and QuickBooks work together?

Yes, through two main routes. QuickBooks Online has a native “Connect to PayPal” app that brings transactions in as sales receipts and breaks out fees automatically, suitable for low-to-mid volume. For higher volumes, multichannel sellers, or businesses needing multicurrency and dispute handling, third-party tools like Synder that sync PayPal to QuickBooks via a clearing account give cleaner reconciliation. QuickBooks Desktop also supports PayPal via CSV import or third-party integrations, though the workflow is more manual.

How do I reconcile PayPal in QuickBooks Online each month?

Pull the Balance Affecting CSV from PayPal for the period, confirm that your PayPal bank account in QuickBooks has matching transactions for every line, identify any missing entries (currency conversions and refunds are the most common gaps), post adjusting journals as needed, then run the standard QuickBooks Online reconciliation against the ending balance. If your gross sales in QuickBooks match PayPal’s gross volume and your fee expense matches PayPal’s fee total, the reconciliation should land at zero.

How are PayPal fees recorded in accounting software?

It should be an expense account, which is separate from revenue. You need to record the gross sale amount to revenue, record the PayPal fee as a separate expense (commonly named PayPal Fees, Merchant Fees, or Payment Processing Fees), and the net amount lands in your PayPal bank account. Recording only the net to revenue understates your top line and hides a legitimate deductible expense, both of which create problems at tax time.

Can PayPal multi-currency be reconciled cleanly in Xero or QuickBooks?

Yes, but you’ll need either multi-currency enabled in your accounting software like QuickBooks Online or Xero, with a separate PayPal account for each currency, or an automation tool that handles conversions and posts FX differences correctly. Without it, multi-currency PayPal activity can slowly fall out of balance as small conversion differences add up over time.

What are the alternatives to PayPal for ecommerce sellers?

The main options are Stripe (lower flat fees, strong international support), Square (simpler setup with integrated POS), Shopify Payments (lowest fees inside the Shopify ecosystem), and Amazon Pay (highest buyer trust on marketplace channels). Most established sellers run PayPal alongside one of them, and don’t replace it.