Backup withholding is a critical tax mechanism designed to ensure the collection of taxes on certain types of income. Understanding its functioning is essential for both payers, such as businesses and financial institutions, and payees, including contractors and investors. It ensures compliance with tax laws and helps maintain accurate financial records.

This article delves into the intricate world of backup withholding, exploring its triggers, how it’s applied, and the crucial role it plays in ensuring accurate tax collection. Our guide aims to demystify the nuances of backup withholding and provide practical insights for staying compliant with IRS regulations.

This article has been prepared for informational purposes only. It’s not intended to provide any tax advice. It’s always best to consult with a tax professional to ensure that taxes are properly calculated and reported.

Streamline your business finances with precision! Discover how Synder’s advanced accounting solutions can transform your financial management. Experience hassle-free, accurate accounting tailored to your business needs. Sign up for a free trial to unlock the power of efficient bookkeeping with Synder today!

What is backup withholding?

Backup withholding is a tax measure that involves the withholding of tax from certain types of income when specific conditions are not met. When regular withholding is not applicable, backup withholding serves as a safeguard for the IRS to capture taxes directly from payments such as interest, dividends, and non-employee compensation.

Unlike regular tax withholding, which is a standard procedure, backup withholding is more circumstantial and triggered under particular situations such as when an individual fails to provide a valid Taxpayer Identification Number (TIN) or in cases of underreported income. It is typically executed at a designated percentage rate, which is crucial for both payers and payees to be aware of.

Responsibilities of payers

The responsibility of implementing backup withholding falls primarily on the payer. This includes businesses, financial institutions, and other entities that make payments of income types subject to this type of withholding. These payers are required to withhold a certain percentage of the payment and remit it directly to the IRS.

Their responsibilities also extend to collecting and verifying the payee’s TIN, and ensuring that they are complying with IRS guidelines. Failure to do so can result in penalties and other consequences. Therefore, payers must be fully aware of their obligations under the backup withholding rules and maintain accurate records to demonstrate compliance.

The role of the Internal Revenue Service (IRS) in backup withholding

Central to the administration and enforcement of backup withholding is the Internal Revenue Service (IRS). The IRS is responsible for issuing the guidelines and regulations that govern backup withholding. This includes determining the income types subject to withholding, setting the applicable rates, and outlining the conditions under which backup withholding should be implemented.

The IRS also plays a critical role in educating both payers and payees about their obligations under the law, providing resources to help them understand when and how backup withholding applies, and enforcing compliance through penalties and audits.

Importance in tax compliance

In the broader context of tax compliance, backup withholding serves as a critical tool for ensuring that taxes are efficiently collected from sources of income that might otherwise go underreported. Capturing tax revenue directly at the source helps maintain the integrity of the tax system, especially in cases where traditional withholding is not applicable. Non-compliance can lead to a range of consequences including penalties and interest charges, making it essential for individuals and businesses to stay informed and compliant to avoid such repercussions.

If you want to find out how long the IRS can hold your refund for review or what day of the week the IRS deposit refunds are, read our guides.

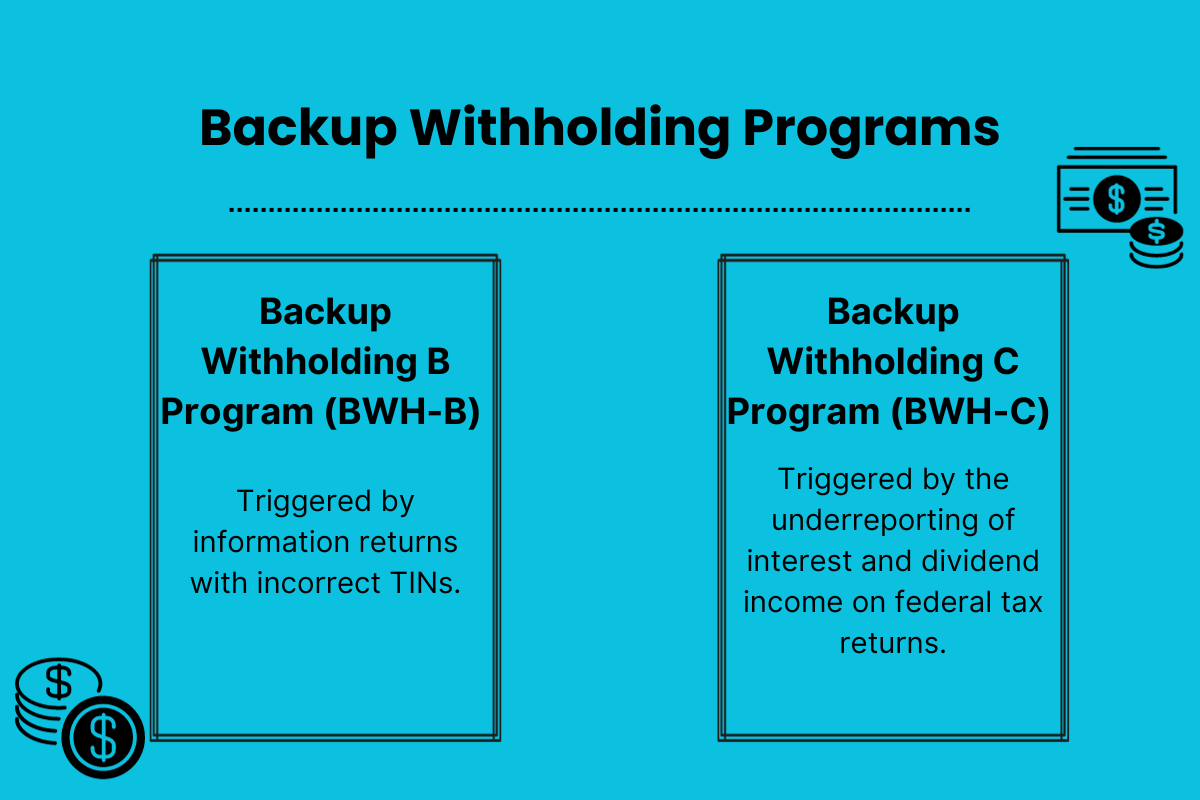

Backup withholding programs

There are two major categories that backup withholding can be divided into: the Backup Withholding B Program (BWH-B) and the Backup Withholding C Program (BWH-C). Let’s look at their differences.

Under the BWH-B Program, BWH may be required if you haven’t provided a correct taxpayer identification number (TIN) to the payer for inclusion on necessary information returns. Your TIN could be your social security number (SSN), employer identification number (EIN), or individual taxpayer identification number (ITIN).

The BWH-C category applies if you have not accurately reported interest and dividend income on your federal tax return or have not confirmed that you are not subject to BWH due to the underreporting of such income.

What are the situations where entities or individuals can be subject to withholding (corresponding form included)

Let’s now look at a comprehensive list of situations that typically trigger backup withholding:

- Failure to provide a TIN: When a taxpayer does not furnish a correct Taxpayer Identification Number to the payer.

- Incorrect TIN: If the IRS informs the payer that the TIN provided by the taxpayer is incorrect.

- Underreported interest or dividend income: When the IRS notifies the payer that the taxpayer underreported interest or dividend income on their tax return.

- Previously subject to penalties: If the taxpayer has previously been penalized for not paying enough tax through withholding or estimated tax payments.

- Government payments reporting: Certain types of government payments might be subject to backup withholding and are detailed on Form 1099-G.

- Patronage dividends: Backup withholding is relevant for patronage dividends where more than half of the payment is monetary, as shown on Form 1099-PATR.

- Rental, profit, royalty, and other income: Payments including rents, profits, royalties, and various other incomes are subject to backup withholding and reported using Form 1099-MISC.

- Independent contractor income reporting: For independent contractors, backup withholding might apply to their commissions, fees, or other payments, which are reported on Form 1099-NEC.

- Transactions through brokers and barter exchanges: These transactions are subject to backup withholding and are reported using Form 1099-B.

- Credit card and third-party network transactions: Transactions processed via payment cards or third-party networks are reported for backup withholding on Form 1099-K.

- Original Issue Discount (OID) considerations: Backup withholding on OID is limited to the cash amount paid and is reported on Form 1099-OID.

- Non-regular gambling withholding on winnings: Winnings from gambling, not covered by standard gambling withholding, are subject to backup withholding and reported on Form W-2G.

Understanding backup withholding in different contexts: Business, personal, and contractor transactions

Backup withholding can apply to a broad range of entities and individuals, primarily focusing on those who receive certain types of income. This includes freelancers, independent contractors, investors receiving dividends or interest, and even some businesses in specific instances.

The key factor determining whether backup withholding applies is the nature of the income and the compliance status of the recipient.

Business and corporate entities

For businesses and corporate entities, backup withholding becomes a significant aspect of financial transactions and account management. These entities must be vigilant when dealing with payments that could be subject to backup withholding, such as payments to contractors or dividends and interest to investors.

For every transaction, the business must ensure the payee’s TIN is accurately collected and reported. Failure to do so can lead to backup withholding requirements, affecting the business’s cash flow and compliance status.

Personal account implications

Individuals also need to be aware of backup withholding, especially if they have multiple income streams or investments, or if they operate as independent contractors. Backup withholding can impact personal accounts by reducing the amount of income initially received. For instance, interest from bank accounts or dividends from investments could be subject to withholding if the IRS has no record of the individual’s correct TIN. It’s vital for individuals to monitor their personal accounts and financial statements to ensure any withheld amounts are duly noted and accounted for in their tax returns.

Contractor considerations in backup withholding

Independent contractors, who often receive payments for services rendered, must particularly be aware of backup withholding. It is imperative for contractors to provide accurate TIN information to their clients to avoid unnecessary withholding.

Additionally, contractors should maintain detailed records of all transactions in their business accounts, including any instances of backup withholding, to facilitate accurate tax reporting and to ensure they receive credit for any taxes already withheld from their payments.

Exceptions and exclusions from withholding

To understand how withholding works, it’s important to be aware of the specific exceptions and exclusions.

Organizations exempt from withholding

Tax-exempt entities, such as nonprofit organizations, are generally exempt from backup withholding. Since these organizations usually don’t have tax liabilities in the same way for-profit entities do, the IRS excludes them from this requirement.

Government bodies, including federal, state, and local government agencies, are not subject to backup withholding. This exemption applies as these entities are responsible for collecting and remitting their own taxes.

Many corporations are exempt from backup withholding. The IRS recognizes that these entities already undergo rigorous tax reporting and withholding processes, reducing the need for additional backup withholding measures. However, it is important to verify whether a specific corporation falls under this exemption, as not all corporate structures may qualify.

Types of payments excluded from withholding

Payments outlined by the IRS that are exempt from backup withholding encompass a variety of financial transactions. These include real estate transactions, situations involving foreclosures and abandonments, and canceled debts.

Additionally, distributions from Archer Medical Savings Accounts (MSAs) and payments related to long-term care benefits are not subject to backup withholding. The same exemption applies to distributions from any retirement account, distributions from an employee stock ownership plan, and cash purchases of fish.

Furthermore, unemployment compensation, state or local income tax refunds, as well as earnings from qualified tuition programs, are also excluded from backup withholding requirements.

Additional exclusions on payments

Certain payments that are already subject to other forms of withholding are also excluded from backup withholding. This is to avoid double withholding on the same income.

Payments made to non-resident aliens (foreign entities) in most circumstances are not subject to backup withholding but may be subject to other types of withholding requirements.

It’s always recommended for both payers and payees to consult with a tax professional or refer to the latest IRS guidelines to understand the specific circumstances of their situation. This ensures compliance with current tax laws and regulations.

How it works: Backup Withholding Program (BWH-B)

The “B” Backup Withholding Program (BWH-B) operates under specific tax regulations and involves a process by which payers (like financial institutions, businesses, or individuals) must begin backup withholding on certain payments. Here’s a breakdown of how BWH-B works as outlined by the IRS.

Trigger for BWH-B

The BWH-B program is activated when a payer files information returns (such as Form 1099 or W-2G) with incorrect Taxpayer Identification Numbers (TINs). The incorrect TINs could be either missing, obviously incorrect (not 9 digits or containing non-numeric characters), or not matching the IRS’s records.

IRS notice to payers

The IRS issues a CP2100 or CP2100A Notice to payers who have filed returns with these errors. The difference between CP2100 and CP2100A Notices is based on the number of error returns filed: CP2100 is for 50 or more errors, while CP2100A is for fewer than 50.

These notices inform the payer that they may need to start backup withholding if it hasn’t been initiated already.

Responsibilities of the payer

Upon receiving the notice, payers should begin backup withholding immediately if they are making reportable payments to a payee who hasn’t provided their TIN, provided an incorrect TIN, or if the TIN doesn’t match IRS records.

Payers are required to make up to three solicitations for the correct TIN (initial, first annual, second annual) to avoid penalties.

Payee’s role in BWH-B

Payees become subject to BWH-B if they do not provide their TIN in the required manner or if the IRS informs the payer that the provided TIN is incorrect. Payees do not receive advance notice from the IRS before backup withholding starts. They must furnish their TIN in writing and certify its accuracy under penalties of perjury, often using Form W-9.

Stopping backup withholding

To stop backup withholding, the payee must provide the payer with the correct TIN.

Payer’s verification through TIN matching

Payers of income reported on specific Forms 1099 may use the IRS TIN Matching program to verify TINs before filing to prevent errors.

How it works: Backup Withholding Program (BWH-C)

The “C” Backup Withholding Program (BWH-C) functions under specific guidelines and involves the following process.

Trigger for BWH-C

BWH-C is initiated when a taxpayer (payee) fails to accurately report or fully report interest and dividend income on their federal income tax return. This can include failing to file a tax return that includes all interest and dividend income received, or not certifying, under penalties of perjury, that they are not subject to backup withholding for accounts opened after 1983.

IRS notices to the taxpayer

Before initiating backup withholding, the IRS sends at least four notices over a minimum period of 120 days, requesting the taxpayer to correct the unreported or underreported interest and dividend income. If no correction is made after these notices, the IRS then sends a final notice informing the taxpayer that they are subject to backup withholding.

Role of payers

Once the IRS determines that a taxpayer is subject to BWH-C, it notifies the payers (such as banks and corporations) to begin backup withholding. Payers are required to deduct 24% from future interest and dividend payments made to the affected taxpayer. Backup withholding applies to interest and dividend accounts or instruments if the payer is notified that the payee is subject to BWH-C.

Stopping backup withholding

To cease backup withholding under BWH-C, the taxpayer must file any missing tax returns and correctly report all interest and dividend income. Alternatively, they can amend previously filed tax returns to accurately report this income. Once the IRS is satisfied with the corrections, it will notify the payers to stop backup withholding.

Payer’s action on receiving a “C” notice

Upon receiving a “C” notice, payers must start backup withholding at the current rate of 24%. They continue this withholding until the IRS informs them that the taxpayer is no longer liable for backup withholding.

Implications for taxpayers

Understanding the financial impact of backup withholding is essential for taxpayers, as it affects both their income and tax returns. Let’s delve into how this withholding influences immediate cash flow and potential refunds, and explore the process of reconciling these amounts during tax filing.

Impact on income and refunds

Backup withholding has direct implications for taxpayers’ income and potential tax refunds. For payees, the immediate effect is a reduction in the amount of income received since a portion is withheld and sent to the IRS. This might affect their cash flow, especially if they were not anticipating this withholding.

However, it’s important to note that this is not an additional tax, but rather a method of ensuring that the appropriate taxes are paid. During the tax filing process, the amount withheld can be credited against the total tax liability. If the withheld amount exceeds the tax liability, it may result in a tax refund for the taxpayer.

Reconciling withheld amounts

For taxpayers who have had income withheld under backup withholding rules, reconciliation is an important process during tax filing. The withheld amount is reported on their tax return and is applied against their total tax liability. To accurately reconcile, taxpayers need to ensure they have all necessary documents, typically the 1099 form, which shows the amount of income paid and the amount withheld. It is crucial for taxpayers to retain these documents as they provide the proof of withholding that is necessary to claim credit on their tax returns.

Learn more about IRS compliance. Find out about audit red flags and how to avoid getting tax audited by the IRS.

Conclusion

Backup withholding is a vital component of the U.S. tax system, serving as a precautionary measure to ensure tax compliance on various types of payments. Understanding the specific scenarios that trigger backup withholding, the obligations of both payers and payees, as well as the exemptions that apply, is crucial for accurate tax reporting and compliance.

By staying informed about these regulations and utilizing available resources for guidance, taxpayers can effectively navigate the complexities of backup withholding, thereby ensuring they meet their tax obligations while avoiding unnecessary penalties.

In view of the evolving tax laws and regulation changes, staying updated and consulting with tax professionals as needed remains an essential practice.

For more information, please visit IRS.gov where you can find a number of useful resources explaining backup withholding and other tax withholding matters.