Revenue recognition sounds like a back-office concern until a misapplied contract costs you a restatement. According to a review by the Center for Audit Quality and Anti-Fraud Collaboration, which looked at more than 400 enforcement actions from the SEC and PCAOB, revenue recognition consistently came up as the top area of regulatory focus. In over 50 cases, executives were held personally liable for issues tied to revenue recognition. For companies that bill customers before delivering services, the gap between when cash arrives and when revenue is earned is a legal and investor-relations risk.

ASC 606, “Revenue from Contracts with Customers,” is the U.S. GAAP standard that governs this. Issued jointly by FASB and IASB, it replaced a fragmented set of industry-specific rules with a single five-step framework that applies to virtually any business operating under customer contracts. This article walks through how that framework works, where companies get tripped up, and how modern finance teams are handling compliance.

TL;DR

- ASC 606 replaced legacy rules with one model: The five-step framework applies across industries and requires recognizing revenue when control of goods or services transfers to the customer, not when cash is received.

- Performance obligations drive timing: Revenue recognition hinges on correctly identifying distinct deliverables in a contract, such as bundles, add-ons, and implementation services, each requiring separate analysis.

- Transaction price allocation is where errors cluster: Variable consideration, discounts, and standalone selling price estimates are judgment-intensive, and missteps here cause restatements.

- ASC 606 and IFRS 15 are nearly aligned, but not identical: For companies reporting under both U.S. GAAP and international standards, licensing treatment and certain transition elections differ.

- SaaS and subscription businesses face the highest complexity: Upgrades, cancellations, prorations, and multi-element invoices each create recognition events that compound quickly at scale.

What is ASC 606, and why does it exist?

Before 2014, U.S. revenue recognition guidance was fragmented. Software companies followed ASC 985-605. Construction firms used percentage-of-completion rules. SaaS businesses, which didn’t exist when most of those rules were written, tried to piece together applicable guidance from multiple sources. The result was inconsistency across financial statements that made meaningful comparison between companies difficult.

The FASB and IASB spent years developing a converged standard. The result, published as ASC 606 in the U.S. and IFRS 15 internationally, established a single principle: recognize revenue to reflect when you’ve actually delivered goods or services, in the amount you expect to receive for them. This idea is what everything else builds on.

Why is ASC 606 important?

What makes ASC 606 more demanding than its predecessors goes beyond the rules themselves and comes down to the level of judgment it requires. Unlike prescriptive standards that tell companies exactly how to handle specific transaction types, ASC 606 is principles-based. That flexibility creates room for interpretation, as well as for auditors to disagree with management’s conclusions.

The standard also expanded disclosure requirements significantly. Companies must now:

- Describe their performance obligations

- Explain the judgments used to determine transaction prices

- Disclose the amount of revenue expected from remaining contracts

For many private SaaS companies, this level of documentation was a new operational requirement.

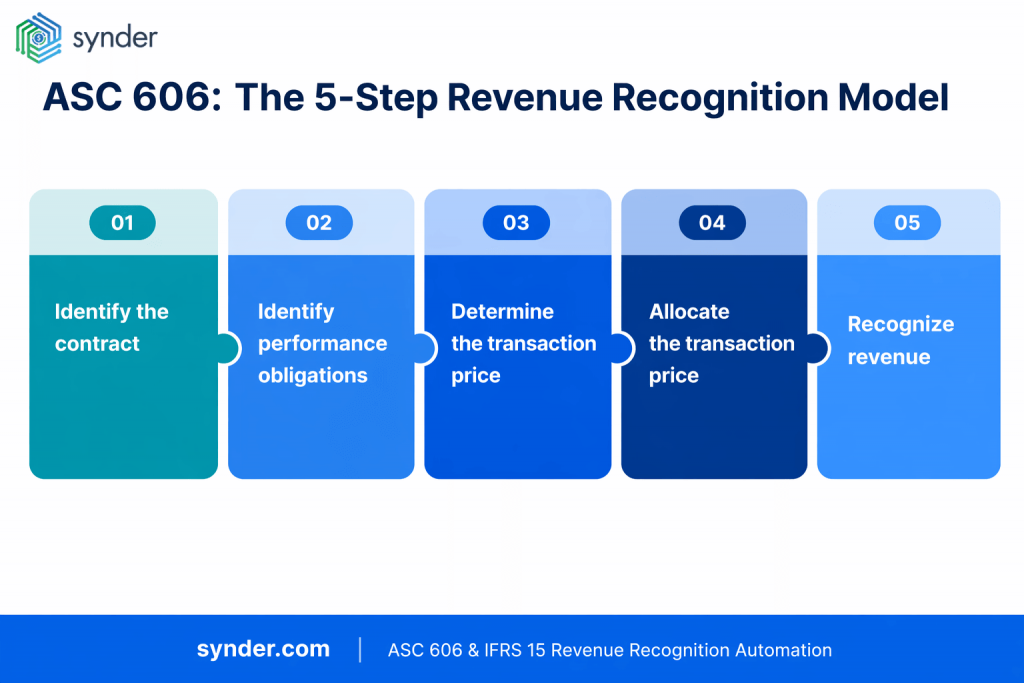

The ASC 606 five-step revenue recognition model

ASC 606 runs every contract through the same five-step sequence, and when you work through each step in order, the amount and timing of revenue fall into place.

Step 1: Identify the contract with the customer

The model begins before a single dollar of revenue can be recognized. Step 1 asks whether a valid contract exists, and the answer isn’t always obvious.

The five qualifying criteria

Under ASC 606, a contract qualifies when five criteria are met:

- The parties have approved the contract and are committed to their obligations.

- Each party’s rights regarding the promised goods or services are clearly identifiable.

- Payment terms are clearly defined.

- The contract has commercial substance.

- It is probable that the entity will collect the consideration it is entitled to.

That last criterion matters more than it might appear. If collectability is in doubt, revenue recognition can’t begin, regardless of what the contract says.

Variable-term and implied contracts

One scenario that often causes confusion for many companies is variable-term contracts. If a customer can terminate at any point without a meaningful penalty, ASC 606 treats the enforceable contract as covering only the period through which termination isn’t possible. A monthly subscription that can be cancelled next month is, economically, a series of one-month contracts, not a 12-month arrangement. That can feel counterintuitive for businesses that sign annual subscription agreements with monthly cancellation rights, but it aligns with how the standard defines what the entity is actually entitled to collect.

Oral and implied contracts also count. And a longstanding business relationship with predictable ordering patterns can count as a contract under ASC 606, even without a formal written agreement. That matters for retail and ecommerce businesses that rely on purchase orders instead of master agreements.

Step 2: Identify the performance obligations

Once a contract qualifies, the next question is what’s being promised. This is where revenue recognition for complex businesses becomes analytically demanding.

What makes an obligation “distinct”

A performance obligation is a promise to transfer a distinct good or service to the customer. “Distinct” has a specific meaning under ASC 606:

- The customer can benefit from the good or service on its own, or together with other readily available resources.

- The promise is clearly separate from other promises in the contract.

Both conditions need to be met. If a delivered item doesn’t really have value on its own without an accompanying service, then the two are usually treated as a single performance obligation, not separate ones.

The bundling problem for SaaS contracts

For SaaS companies, the performance obligation analysis rarely ends at “monthly subscription access.” Consider a SaaS contract that includes software access, implementation services, and dedicated customer success support. Are those three distinct performance obligations or one bundled arrangement?

The answer turns on whether a customer could realistically buy the implementation from a third party (they probably could) and whether the support is integrated into the software delivery or just a service layer on top (it might be either). That analysis has to happen contract by contract, and the conclusions need to be documented.

The disclosure obligation under ASC 606 requires companies to describe their performance obligations in sufficient detail that users of financial statements can understand the nature, amount, timing, and uncertainty of revenue and cash flows. That’s a high bar. For a company with ten different contract types, it translates to ten documented obligation analyses, reviewed and updated whenever pricing or product structure changes.

Step 3: Determine the transaction price

The next question is how much consideration the entity expects to receive. In a fixed-price contract, this is quite simple, but in most real-world SaaS and ecommerce arrangements, it isn’t.

Variable consideration and the constraint

Transaction price includes everything the entity expects to collect, but only what it’s entitled to. Variable consideration requires estimation, which means accounting for elements such as:

- refund rights

- volume discounts

- penalties

- bonuses

- usage-based fees

All of these need to be estimated at contract inception and updated each reporting period.

The standard requires using either the expected value method (probability-weighted average of possible outcomes) or the most likely amount method (the single most likely outcome), whichever better predicts the consideration to be received.

There’s a constraint: estimated variable consideration can only be included in the transaction price to the extent it’s highly probable a significant revenue reversal won’t occur when uncertainty is resolved. That’s a conservative threshold, which means companies can’t book optimistic revenue estimates just because a deal feels likely to close favorably. Audit firms scrutinize this constraint carefully because management has a natural incentive to recognize revenue sooner.

Noncash consideration and financing

Noncash consideration (equity, services, or other assets received in exchange for goods or services) gets measured at fair value. Consideration payable to a customer (rebates, co-op advertising, coupons) reduces the transaction price, not cost. That’s very important for retailers and ecommerce businesses that run trade promotion programs.

One underappreciated aspect of this step is the financing component. If there’s a meaningful gap between when the customer pays and when you deliver the service, and that gap creates a financing benefit for either side, you may need to adjust the transaction price to reflect the time value of money. There is a practical shortcut, though: if that gap is expected to be one year or less, no adjustment is required, which covers most subscription businesses on monthly billing, but annual prepayments are still worth a closer look.

Step 4: Allocate the transaction price

Once the total transaction price is determined, it must be spread across the performance obligations identified in Step 2. The allocation method under ASC 606 is based on relative standalone selling prices (SSPs) – the price at which each obligation would be sold separately.

Standalone selling price and estimation methods

Standalone selling price (SSP) is where multi-element contracts become particularly challenging. A SaaS contract might bundle annual access at $10,000 with implementation services valued at $3,000, but you cannot just assign those amounts directly. If a discount brings the total down to $11,000, it has to be spread across both elements based on their standalone selling prices, not pushed into just one.

That matters for your income statement, because implementation work finished in Q1 will carry part of that discount, even if you’d prefer to recognize more of it later.

Observable SSPs are the easiest to work with, since they reflect what you actually charge when selling the item on its own. When that data is not available, you need to estimate it using one of the accepted methods:

- adjusted market assessment

- expected cost plus margin

- residual approach, used only when pricing is highly variable or uncertain

Whichever method you use, it needs to be documented and applied consistently across reporting periods.

How discounts must be allocated

Discounts present a specific problem. Under ASC 606, they’re allocated proportionally across all performance obligations unless there’s clear evidence the discount relates to only some of them.

We work with a Boston-based ecommerce data syndication platform that discovered this when it needed to track discounts at the same granularity as revenue GL entries. Without the ability to identify exactly which performance obligations a discount applied to, the income statement presentation was misleading, as product totals and discount lines didn’t reconcile cleanly. Automated revenue recognition resolved this. It gave them the flexibility to report discounts at the same granularity as revenue GL entries, ensuring both product totals and discounts are reflected in their P&L.

Step 5: Recognize revenue when performance obligations are satisfied

This is the point when revenue actually gets recorded in the income statement, as it is recognized when, or as, a performance obligation is satisfied and control transfers.

Over time vs point in time

Control can transfer at a point in time or over time, and the distinction matters for when revenue hits the income statement. An obligation is satisfied over time if one of the following applies:

- The customer receives and consumes the benefits as you perform;

- Your work creates or enhances an asset the customer controls;

- Your work does not create an asset you can redirect elsewhere, and you have a right to payment for what has been completed so far.

Most SaaS subscriptions fall into the first category, since customers are using the service as they go, so revenue is recognized evenly over the subscription period.

Point-in-time recognition applies to everything else, like distinct licenses, physical goods once they are shipped, or services that are delivered as a completed milestone. If a customer buys a software license that isn’t continuously updated, the license itself may be a point-in-time obligation, even if ongoing support is recognized over time.

How does the 5-step process of ASC 606 impact the timing and amount of revenue recognized?

For subscription businesses, the biggest impact is how upfront payments are handled. If a customer pays $12,000 in January for an annual plan, you do not recognize it all at once. Instead, you recognize $1,000 each month as the service is delivered, while the remaining $11,000 sits as deferred revenue on the balance sheet until it is earned. This is required under ASC 606, so companies that used to recognize annual contracts upfront, or pull revenue forward to hit targets, had to adjust their numbers when they adopted the standard.

There is also an impact on how much revenue gets recognized. If variable consideration was previously recorded too optimistically, the ASC 606 constraint may reduce revenue in certain periods, while in other cases, companies that were overly conservative before may end up recognizing revenue earlier, especially for term licenses where control transfers at delivery.

ASC 606 vs. IFRS 15: Where the standards converge and diverge

The gap between ASC 606 and IFRS 15 is small by design. They were built together, and the core framework is the same. Still, if you report under both U.S. GAAP and IFRS, or plan to raise funds from international investors, a few differences are worth paying attention to.

| Dimension | ASC 606 (U.S. GAAP) | IFRS 15 (International) |

| Core five-step model | Identical | Identical |

| Software licensing | More nuanced ongoing activity analysis | Cleaner point-in-time vs. over-time split |

| Transition elections | Full or modified retrospective | Full retrospective, modified retrospective, or additional expedient |

| Practical expedients | Portfolio approach, shipping and handling, significant financing | Same, with one additional transition option |

| Effective date (public) | Annual periods after Dec 15, 2017 | Annual periods beginning on or after Jan 1, 2018 |

| Effective date (private) | Annual periods after Dec 15, 2018 | Annual periods beginning on or after Jan 1, 2018 |

| Disclosure requirements | Specific guidance on performance obligations, judgments, and remaining contract value; industry nuance via FASB TRG | Stronger emphasis on disclosure of judgments in certain areas; IASB TRG interpretations |

| Industry-specific guidance | FASB TRG interpretations + SEC staff guidance | IASB TRG interpretations |

| Consolidation adjustment | Required when subsidiaries use IFRS 15 | Required when parent applies U.S. GAAP |

| Practical tip: If your business is U.S.-only, you can table the IFRS 15 comparison for now, it won’t change how you recognize revenue day to day. But if you’re raising international capital, buying a foreign entity, or eyeing a dual-listed IPO, the differences become real fast. Get your auditors across the specific divergences before a buyer’s due diligence team finds them first. |

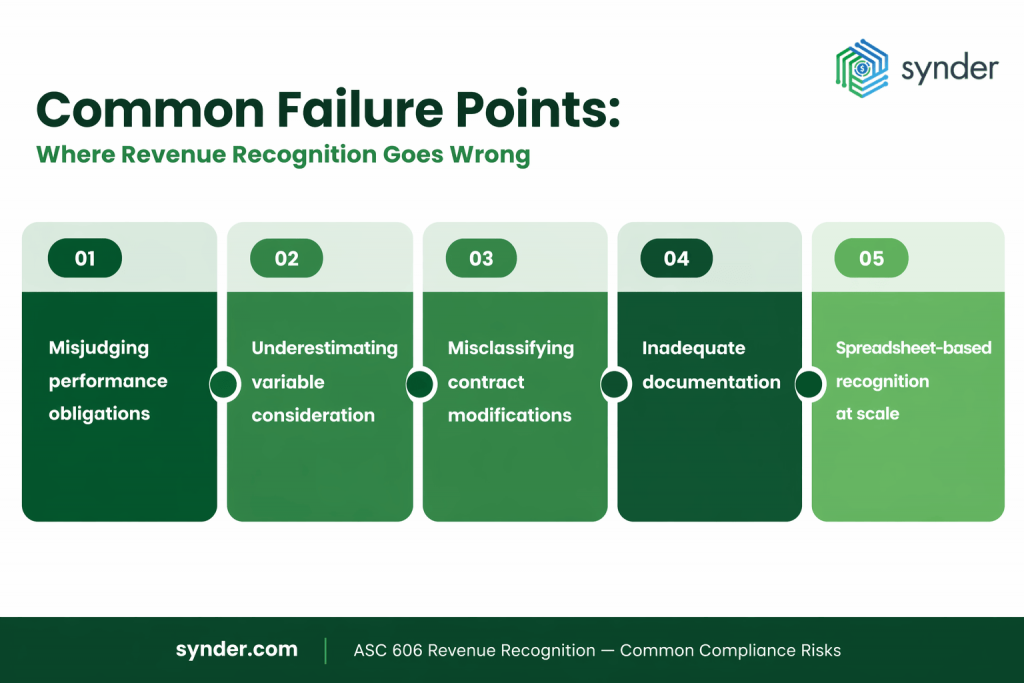

Common failure points: Where revenue recognition goes wrong

Understanding the five steps is necessary but not sufficient for compliance. The cases where companies get into trouble follow predictable patterns.

Misjudging distinct versus integrated performance obligations

Cohen & Company’s 2025 analysis of ASC 606 compliance challenges found that the performance obligation determination for implementation and professional services remains the top compliance issue for software and SaaS companies. The question – is this service distinct or integral to the software? – turns on customer dependency. As more companies move to the cloud, implementation services are increasingly tied to specific vendor platforms, which often means they’re treated as a single bundled obligation. That shift can significantly affect the timing of revenue recognition.

Underestimating variable consideration

Usage-based billing, volume discounts, and SLA credits all introduce uncertainty into the transaction price. It means you need to estimate them carefully. If you assume everything will be collected in full, or ignore past SLA credits, you’re likely overstating revenue, and that’s something auditors tend to question.

Treating contract modifications as new contracts when they’re not

A subscription upgrade is usually a contract modification. Under ASC 606, it is treated as a new contract only if the added services are distinct and priced at their standalone selling price. If there is a discount or the new services are closely tied to what already exists, it stays part of the original contract. Mixing up these treatments is a common reason subscription businesses end up restating revenue.

Inadequate documentation

Revenue recognition “has been, and will likely remain, a significant area of focus for auditors and regulators of public companies, given its importance to investors and its high susceptibility to fraud,” according to the Center for Audit Quality and Anti-Fraud Collaboration’s enforcement review. Documentation is what shows your decisions were reasonable. Without it, even a solid accounting position can be hard to stand behind.

Spreadsheet-based recognition at scale

For companies processing thousands of subscription invoices per month, manual spreadsheet-based recognition schedules introduce error through human data entry, formula errors, and version control failures. As a COO at an ecommerce data syndication platform put it:

I don’t see any other good options out there to do daily revenue recognition and prorations on subscriptions, while mixing combinations of advanced/arrears billing and one-time/recurring items. There’s just a lot of complexity in there and Synder generates thousands of GL entries for us to get us where we need to be.

Joe DiNardo, COO at Syndic8

How automation handles what manual processes can’t

The failure points above share a common thread: they’re ongoing judgment calls that have to be applied consistently, at volume, across every contract, every period. That’s exactly where manual processes break down and where revenue recognition automation earns its place.

Revenue recognition tools designed for ASC 606 compliance don’t just schedule straight-line amortization, but enforce the five-step logic programmatically. When recognition rules are configured once and applied to every invoice, the same treatment runs every time, regardless of volume, staff turnover, or month-end pressure. Subscription modifications trigger automatic schedule updates. Variable consideration feeds from source data rather than manual inputs. Every entry carries a traceable audit history without anyone having to reconstruct it after the fact.

What ASC 606 revenue recognition software can do

- Real ASC 606 logic: handles contract modifications, variable consideration, and complex performance obligations, not just straight-line schedules

- Direct integrations: connects to billing and accounting systems (like Stripe and QuickBooks), so data flows in automatically without manual uploads

- Full audit trail: captures contract terms, allocations, recognition timing, and journal entries for audit readiness

- Multi-element support: allocates revenue based on SSP across multiple performance obligations

- Handles contract changes properly: supports upgrades, downgrades, cancellations, and refunds with the correct accounting treatment

For example, Synder’s RevRec module connects natively to Stripe, so subscription data flows in directly, and any changes to active subscriptions are tracked in real time. For businesses on other billing platforms, RevRec supports data import via a structured Excel template, where uploaded invoices and refunds generate the same compliant schedules and journal entries.

In both cases, it automatically allocates revenue across billing periods in full compliance with ASC 606 and IFRS 15, and handles:

- multi-item invoices

- refunds and cancellations

- prorations and upgrades

- ongoing subscription changes in real time

Deferred revenue moves from the balance sheet to the income statement on schedule, and the full audit trail is generated automatically rather than assembled manually at close.

Before and after: how real companies automate revenue recognition

One of our clients, a digital pet health platform offering 24/7 veterinary telehealth services, was managing Stripe revenue recognition entirely in Excel. Annual subscription invoices had to be manually split across months, subscription modifications, such as cancellations, upgrades, refunds, required manual schedule updates, and matching invoices across Stripe and PayPal was a recurring source of errors. As a GAAP-compliant business with a growing subscriber base, the process was both time-consuming and fragile.

After implementing Synder RevRec, annual subscription invoices flow automatically into a deferred revenue account on the balance sheet, with equal monthly portions recognized to the P&L without manual intervention. Any modification in Stripe, be it refund, cancellation, upgrade, chargeback, is automatically detected, included in the recognition schedule, and posted to QuickBooks Online. Invoices from both Stripe and PayPal are synced, matched, and reconciled within the same system.

As a consumer company, it’s really important to be able to automate revenue recognition and set up the right integrations between Stripe and QuickBooks. This is definitely something we don’t want to do manually at scale. Being able to automate with Synder became a must.

Andrew Malek, Founder and CTO at Pawp

If you want to see how automated revenue recognition works for a subscription business, you can book a demo with Synder.

The ASC 606 transition methods and what they mean for your historical books

Companies that haven’t yet adopted ASC 606, or that are revisiting the transition decisions made at adoption, need to understand how the two permitted transition approaches affected historical financials, because auditors and investors will.

Full retrospective method

The full retrospective method means going back and restating prior periods as if ASC 606 had always been applied. That affects both the income statement, mainly revenue timing, and the balance sheet, including contract assets, liabilities, and deferred revenue.

The upside is clean comparability, since your year-over-year numbers are based on the same rules. The downside is the effort. For companies with complex, multi-element contracts, restating a few years of financials can take months.

Modified retrospective method

The modified retrospective method is simpler. Companies start applying ASC 606 from the adoption date and record a one-time adjustment to opening retained earnings, instead of restating prior periods. Earlier periods stay as they were, with disclosures explaining the differences. Most private companies went this route.

The tradeoff is comparability. For the first few years, your financials under ASC 606 won’t line up directly with earlier periods, which can matter for things like covenants, earnouts, and trend analysis.

Why a post-adoption review still matters

According to Precedence Research, the global SaaS market reached $408 billion in 2025, with around 95% of organizations now using SaaS in at least one business function.

At this point, most companies are well past the initial ASC 606 transition. But many haven’t taken a step back to review how things have evolved since then. New contracts, product launches, and pricing changes often introduce revenue recognition decisions that were never formally documented against the standard.

That’s why a periodic compliance check is worth it, especially ahead of a fundraising round or acquisition

Conclusion: ASC 606 revenue recognition in practice

ASC 606 isn’t new, but staying compliant – really compliant, not just what you documented at adoption – takes ongoing effort. The five-step model is a framework, but applying it to a business that keeps changing its contracts, pricing, and structure means relying on both good systems and sound judgment.

A common pattern is getting it right at the start, then gradually drifting as the business grows and deals get more complex. Revenue recognition is still an area regulators watch closely, where restatements are public, and where audit issues can slow down a funding round or acquisition. What makes the difference is having the processes in place to apply the standard consistently and to show how you did it.

For SaaS and subscription businesses, the real question is when to automate revenue recognition, not if. As volume grows, spreadsheets quickly become hard to manage. Putting the right systems in place early tends to make compliance feel controlled rather than overwhelming.

FAQ

What is the difference between revenue recognition ASC 606 and IFRS 15?

ASC 606 (U.S. GAAP) and IFRS 15 (international) share an identical five-step framework developed jointly by FASB and IASB. The main practical differences are in software licensing analysis, certain transition elections available only under IFRS 15, and minor disclosure emphasis variations. For most subscription and SaaS businesses, the two standards produce the same recognition outcomes. Companies operating across jurisdictions should document any differences and confirm treatment with their auditors.

Does ASC 606 apply to private companies?

Yes. ASC 606 applies to all U.S. entities that enter into contracts with customers to transfer goods or services, including private companies and nonprofits. Private companies received a later effective date (annual periods beginning after December 15, 2018, with some extensions to 2019), but there are no ongoing exemptions. Private companies preparing for a capital raise, audit, or acquisition should ensure their revenue recognition policies are fully documented and applied consistently.

What is the GAAP rule for revenue recognition?

Under ASC 606, the core GAAP rule is that revenue is recognized when (or as) a performance obligation is satisfied, meaning when control of the promised good or service transfers to the customer. The framework replaced older rules that focused on risk and rewards transfer with a control-based model, which is particularly relevant for long-term service contracts and software licensing arrangements.

What is the first step of revenue recognition under ASC 606?

Formally, it’s identifying the contract with the customer. But practically, the analytical work that drives most recognition decisions happens in Step 2 – identifying performance obligations. Getting this step right determines everything that follows: how revenue is allocated, when it’s recognized, and how much goes to the income statement versus deferred revenue on the balance sheet.

How does contract modification affect revenue recognition under ASC 606?

A contract modification is treated as a new contract when it adds distinct goods or services at their standalone selling price. If the added goods or services aren’t distinct, or aren’t priced at SSP, the modification adjusts the existing contract, requiring either a cumulative catch-up adjustment (when remaining goods are distinct) or a prospective blended rate adjustment (when remaining performance is a single bundle). For subscription businesses, every upgrade and downgrade is a modification event that requires this analysis.

What is deferred revenue under ASC 606?

Deferred revenue represents consideration received from a customer before the related performance obligation has been satisfied. Under ASC 606, it’s classified as a contract liability on the balance sheet. For annual subscriptions billed upfront, the full prepayment enters deferred revenue and is recognized ratably to the income statement as the service period elapses. Deferred revenue balances are a key disclosure item under ASC 606, and auditors scrutinize whether the timing of recognition from the deferred balance is consistent with actual performance.