When running a business, managing your accounts receivable isn’t just important—it’s a game-changer. Some might think, “Do I need this?” (Spoiler: Yes, you do.) Why? Because healthy cash flow and stable income don’t happen by accident—they’re the result of smart receivables management.

Get it right, and you’ll secure timely payments, maintain high liquidity, and build strong customer relationships—all without disputes or payment-related headaches. So how can you achieve this? Drawing from our deep expertise at Synder, we’ve put together best practices and strategies to help you stay ahead. Let’s dive in.

Contents

What is accounts receivable (AR)?

Simply put, accounts receivable (AR) is the money your customers owe you for products or services they’ve already received. Think of it as cash on its way to your business—it’s listed as an asset on your balance sheet because it’s the money you’re set to collect soon.

Looking for more details? When you let customers pay later, their unpaid bills become your accounts receivable. They usually have a set deadline, like 30 or 60 days, to settle up. Managing AR well is key to keeping your cash flow healthy and your operations running smoothly.

Important note: AR is money coming to you, while accounts payable (AP) is money you owe others. For example, if you buy office supplies from a vendor and agree to pay in 30 days, that unpaid bill is part of your accounts payable.

Dive deeper into the Difference between Accounts Receivable and Payable.

What is accounting receivable management?

Accounts receivable management is how a business makes sure customers pay on time for products or services bought on credit. The key parts of this process include:

- Billing and invoicing: Sending accurate invoices quickly.

- Payment processing: Handling payments and matching them to accounts.

- Client communication: Keeping in touch with customers about payments.

- Internal coordination: Ensuring all teams work together smoothly.

- Credit and collections: Setting credit terms and following up on late payments.

What are the challenges of AR?

The more you have to keep track of, the more challenges can arise. To tackle them effectively, you need to recognize them first, right? Let’s dive into the biggest challenges businesses face and how they can throw a wrench in your operations.

- Weak credit policies: Without strong credit policies in place, you could end up extending credit to unreliable customers—setting yourself up for unpaid debts and revenue loss.

- High Days Sales Outstanding (DSO): High Days Sales Outstanding (DSO) means payments take way too long to roll in, seriously damaging your ability to grow or react to financial surprises.

- Invoice errors: One wrong number or missing detail on an invoice can spark disputes, delay payments, and tarnish your professional image.

- Disorganized records: Without clear, organized records, tracking who owes what becomes a guessing game, increasing the risk of unpaid invoices slipping through.

- Communication gaps: If you’re not crystal clear with customers about payment terms or overdue balances, confusion and delays will follow.

- Manual processes: Relying on outdated, manual processes slows you down and leads to costly mistakes. It’s like trying to run a marathon in flip-flops.

Best practices for accounts receivable management

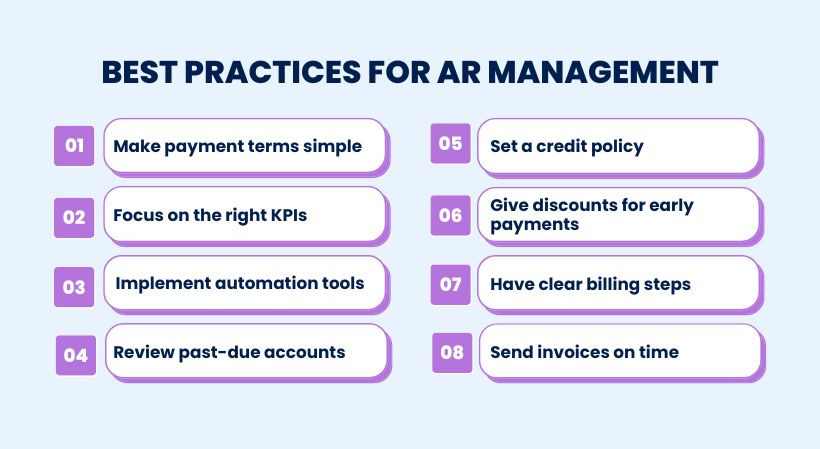

Now that you’re familiar with the major AR challenges, it’s time to learn how to avoid them, right? We’ve gathered 8 best practices for managing your accounts receivables. Let’s break them down one by one.

1. Make payment terms simple

Keep your payment terms crystal clear to avoid any confusion and get paid on time. Here’s how to simplify the process:

- Set clear expectations: Spell out exactly when and how payments should be made. For example, “Net 30” means payment is due within 30 days of the invoice.

- Keep it consistent: Include your payment terms on every document—purchase orders, contracts, and invoices—so there’s no room for doubt.

- Be upfront: Talk about payment terms early on with customers to make sure everyone is on the same page.

When your payment terms are simple, you save time, avoid misunderstandings, and ensure smoother cash flow.

2. Focus on the right KPIs

Even the best policies and processes won’t help if no one follows them. And let’s face it, compliance alone isn’t enough—poorly managed operations can silently eat away at your profits before you even notice.

The fix? Keep tabs on key accounts receivable KPIs. These metrics give you a clear view of what’s working, what’s not, and where to act fast to improve. Here are the ones you should track:

- Accounts Receivable Turnover (ART): This ratio measures how often your company collects its average accounts receivable during a specific period. A higher ART indicates efficient collections and shorter payment cycles.

- Average Days Delinquent (ADD): ADD calculates the average number of days payments are overdue beyond the agreed terms, highlighting delays in the collection process.

- Collections Effectiveness Index (CEI): CEI assesses the percentage of total accounts receivable collected within a set timeframe, reflecting the efficiency of your collections efforts.

- Days Sales Outstanding (DSO): DSO determines the average number of days between issuing an invoice and receiving payment, indicating the efficiency of your credit and collections process.

Capturing these metrics is only the first step. Regularly compile them into reports to gain a comprehensive, historical view of your accounts receivable performance. This practice enables you to identify operational bottlenecks and implement targeted improvements, ultimately enhancing cash flow and reducing the risk of bad debts.

Here are all the necessary formulas, you’ll need:

| AR KPIs | Formula |

| Accounts Receivable Turnover (ART) | Net Credit Sales / Average Accounts Receivable |

| Average Days Delinquent (ADD) | Days Sales Outstanding – Best Possible Days Sales Outstanding |

| Collections Effectiveness Index (CEI) | (Beginning A/R + Monthly Credit Sales – Total Ending A/R) × 100 / (Beginning A/R + Monthly Credit Sales – Current Ending A/R) |

| Days Sales Outstanding (DSO) | (Accounts Receivable / Total Credit Sales) × Number of Days |

3. Use automation tools like Synder for AR tasks

Picture this: you’re running a subscription-based SaaS business and need to connect Stripe with QuickBooks to keep your accounts receivable in check. Handle it manually, and here’s what you’re signing up for:

Best-case scenario? A few errors and countless hours lost on mind-numbing data entry.

Worst-case? Total chaos—messed-up books and a massive headache. Sounds like a lose-lose, doesn’t it?

Here’s the good news: automation can save you. And that’s exactly where Synder steals the spotlight.

With Synder RevRec, you can leave these problems behind. Synder RevRec seamlessly pulls subscription data from payment platforms like Stripe into QuickBooks Online, turning it into a centralized hub for managing your subscriptions. This automation eliminates manual tracking, even as your subscription numbers grow. And that’s not all—in case of Stripe QuickBooks Online integration, Synder offers even more benefits:

- Automatic Stripe subscription tracking: Synder can automatically create recognition schedules based on Stripe data and track changes like refunds, cancellations, upgrades, or multiple products.

- GAAP-compliant revenue recognition: Software recognizes revenue when obligations are fulfilled, not when cash is received, ensuring compliance.

- Invoices with extended terms: You can manage Net 30, Net 60, and other extended terms to start recognizing revenue even before payment is received.

- Detailed subscription insights: You’ll receive access to automated schedules and accurate reports showing deferred and recognized revenue each month.

- Multicurrency support: Synder simplifies reporting by managing schedules in your home currency using Stripe’s conversion rates to avoid discrepancies.

- Discount recognition: With Synder, you can easily track and recognize discounts across billing periods with flexible processing options.

Has Synder caught your eye? Join our Weekly Public Demo to see Synder’s full capabilities in action, or use a 15-day free trial to test Synder yourself.

4. Regularly review past-due accounts

Don’t let late payments catch you off guard. Schedule regular reviews, like monthly meetings, to keep your AR team and execs in the loop. Staying proactive ensures everyone’s on the same page and ready to tackle overdue accounts before they become a problem.

Why it’s important

- Keep cash flow steady: Collecting overdue payments ensures you have enough funds for daily operations and growth.

- Spot payment risks: Regular checks help identify customers who often pay late so you can address the issue early.

- Build better relationships: Dealing with overdue accounts quickly improves communication and resolves disputes faster.

How to review past-due accounts

- Use aging reports: Group overdue invoices by how late they are to prioritize collections.

- Automate monitoring: Use tools to track and send reminders for overdue payments automatically.

- Talk to customers: Regularly reach out to resolve payment issues and maintain positive relationships.

- Adjust credit policies: Update credit terms based on payment behavior to avoid future delays.

5. Set a credit policy

Deciding whether to offer credit? Set clear policies upfront to stay in control. With the right rules in place, you can avoid overextending credit while making it easy for you to decide when a client qualifies. As a result: no guesswork and no headaches. Here’s how to set one up the smart way:

1. Set clear credit standards

- Check creditworthiness: Use credit scores, payment histories, or financial reports to decide who gets credit.

- Define credit limits: Assign sensible limits based on each customer’s reliability and your risk tolerance.

2. Nail down payment terms

- Keep it simple: Specify when payments are due, like Net 30 or Net 60.

3. Create a collection strategy

- Stay on top of it: Follow up on overdue payments regularly—don’t let them slip through the cracks.

- Have a plan for late payments: Add late fees or escalate to collections if needed.

4. Communicate the policy

- Train your team: Make sure everyone knows how to enforce the policy consistently.

- Be transparent with customers: Clearly explain terms upfront to avoid surprises.

5. Keep it fresh

- Review regularly: Check if your policy is working and tweak it as needed.

- Adapt to change: Stay updated on industry trends and adjust your policy to stay competitive.

A great credit policy isn’t just about avoiding bad debts—it’s about building trust, speeding up payments, and keeping your finances strong.

6. Give discounts for early payments

If you want to get paid faster, you can offer customers a discount for early payments. Add terms like 2/10 net 30 to your invoices—this means they get a 2% discount if they pay within 10 days, or they pay the full amount in 30 days.

Not every customer will take the deal, but many will, giving you quicker cash flow and fewer overdue invoices. After all, it’s a win-win: they save money, and you get paid sooner. Just make sure the discount terms are clear on your invoices to avoid confusion.

7. Have clear billing steps

To keep your billing process running smoothly, set clear rules and stick to them with no exceptions. Consistency is the secret to avoiding costly errors and chaotic books. If you wing it every time, you’ll be left with a mess of mistakes, disorganized records, and cash flow headaches by the year’s end. Here’s how to enhance your billing operations:

- Set clear billing cycles: Define consistent billing periods and invoicing dates to establish a predictable payment schedule.

- Detail your invoices: Include essential information such as purchase order numbers, billing and shipping addresses, itemized descriptions, quantities, prices, applicable taxes, and payment terms.

- Maintain organized records: Keep comprehensive records of all invoices and payments to ensure accuracy and facilitate audits.

- Regularly assess AR processes: Periodically evaluate your AR procedures to identify and rectify inefficiencies.

- Implement effective collections procedures: Develop a systematic approach for handling overdue payments, including timely reminders and escalation protocols.

- Document client-specific details:

- Billing сontacts: Maintain up-to-date contact information for each client.

- Unique billing requirements: Note any special billing instructions or preferences per client.

- Payment histories and notes: Track payment behaviors and any relevant notes to inform future interactions.

8. Send invoices on time

Sending invoices promptly is a cornerstone of effective accounts receivable (AR) management, directly influencing cash flow and financial stability. Here’s why timely invoicing is crucial and how to implement it effectively:

- Enhances cash flow: Prompt invoicing initiates the payment process sooner, leading to quicker receipt of funds and improved liquidity.

- Reduces payment delays: Clear and timely invoices minimize confusion and disputes, encouraging clients to pay within the agreed terms.

- Improves financial planning: Consistent invoicing provides better predictability of income, aiding in accurate budgeting and financial forecasting.

How to ensure timely invoicing?

- Automate the invoicing process: Utilize electronic billing systems to generate and send invoices automatically, reducing manual errors and ensuring consistency.

- Set clear payment terms: Define and communicate payment deadlines, accepted payment methods, and any penalties for late payments upfront to set clear expectations.

- Monitor accounts receivable metrics: Track key performance indicators like Days Sales Outstanding (DSO) to assess the efficiency of your invoicing and collection processes.

- Maintain accurate records: Keep detailed records of all transactions to facilitate timely invoicing and quick resolution of any disputes.

By implementing these practices, businesses can streamline their AR management, reduce the incidence of late payments, and maintain a healthier cash flow.

Conclusion

Accounting isn’t a walk in the park, and accounts receivable? That’s the backbone of your cash flow. Manage it poorly, and you’re in for a world of headaches—who wants that? Exactly, no one.

That’s why practices like past-due accounts review and clear payment policies can save you time and sanity. And for the ultimate game-changer, accounting automation tools like Synder have your back, optimizing the heavy lifting and speeding up the whole process.