- Stripe Reserve Transaction Types

- How Synder Syncs Stripe Balance Reserves

- Per Transaction Mode

- How This Appears in Accounting Software

- Summary Sync Mode

- Important Notes

- FAQ

This guide explains how Stripe balance reserve transactions sync to your accounting software through Synder.

Use this guide if:

- You see reserve-related transactions in Stripe and want to understand how they sync to accounting.

- Your Stripe balance temporarily decreases or increases due to reserve holds or releases.

- You want to confirm that Synder recorded these transactions correctly.

Stripe may temporarily hold a portion of your balance for risk management or payout configuration. When this occurs, Stripe creates reserve hold and reserve release transactions in the balance history. Synder fetches and synchronizes all reserve transaction types.

Stripe Reserve Transaction Types

Stripe uses several transaction types to represent temporary balance holds and releases. The exact transaction name depends on the reserve type.

Reserve Transactions (Stripe Connect Reserves)

Used by Stripe Connect platforms when a connected account has a negative balance.

Funds are temporarily moved into a reserve until the connected account balance recovers.

Refer to this article in Stripe for more details.

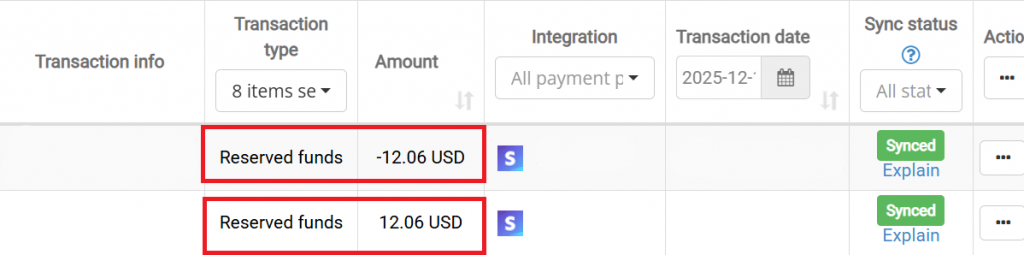

Reserved funds

Stripe may hold funds if your account is assessed as having elevated risk (for example higher dispute rates).

Funds are released after the configured holding period if no liabilities occur.

Payout minimum balance hold/release

If you configure a minimum balance for payouts, Stripe retains part of your balance. When the minimum balance setting is reduced or removed, Stripe creates a payout minimum balance release transaction.

Payment network reserve hold/release

Payment networks such as Visa or Mastercard may temporarily reserve funds to cover potential disputes.

Issuing authorization hold/release

These transactions apply to Stripe Issuing cards. When a card purchase is authorized, Stripe temporarily holds the amount until the transaction is captured or released.

Synder also supports Stripe Issuing transactions, including captured card payments.

For more details on how exactly reserves work and why they are necessary, visit this article from Stripe Help Center.

How Synder Syncs Stripe Balance Reserves

Synder synchronization behavior depends on the selected sync mode.

Per Transaction Mode

In Per Transaction mode, Synder automatically creates an asset account named Balance Reserve in your accounting records. This account can be changed in the settings, if needed.

Synder records transactions based on the reserve movement direction:

- Reserve hold (negative transaction) – Funds move from your clearing account → Balance Reserve account

- Reserve release (positive transaction) – Funds move from Balance Reserve account → clearing account.

This structure reflects that the funds remain owned by the business but are temporarily restricted.

Transaction types created in Synder correspond to the specific reserve transaction names used in Stripe.

Example transaction in Synder:

How This Appears in Accounting Software

The created entity depends on the accounting platform.

- QuickBooks Online – Transfer (From and To accounts vary based on whether the transaction is positive or negative).

- QuickBooks Desktop – Transfer (From and To accounts vary based on whether the transaction is positive or negative).

- Xero – Invoice + payment ( for releases) or Credit note + refund (for holds).

Summary Sync Mode

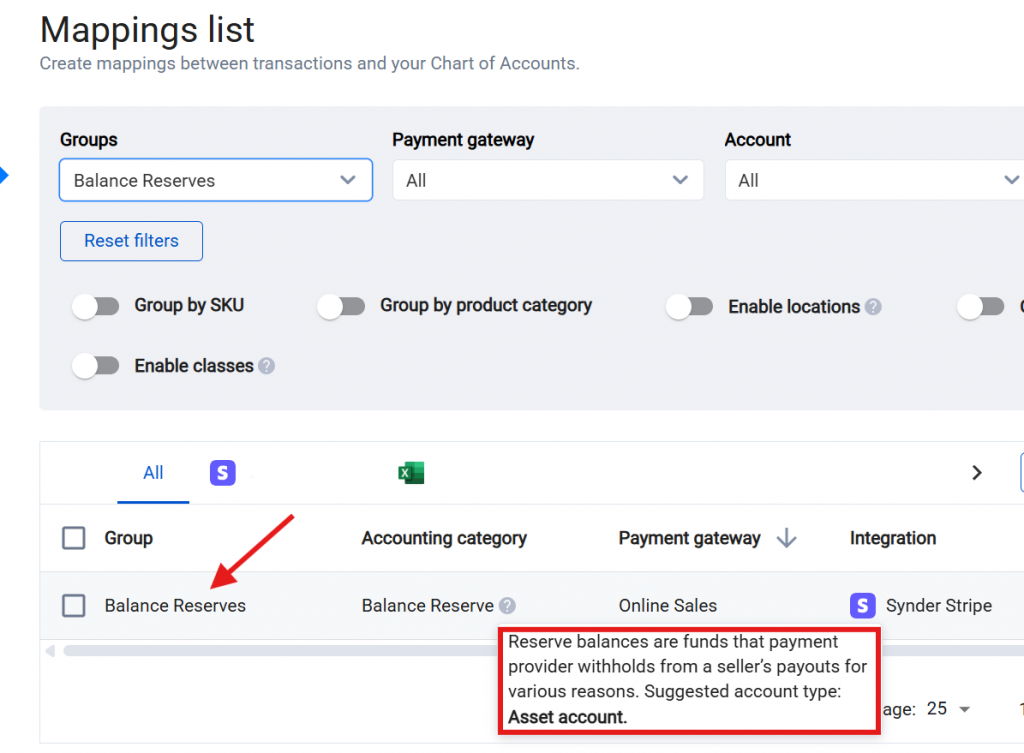

In Summary Sync mode, when Synder detects a reserve transaction, a new mapping line appears in the Mappings list.

Assign the appropriate Balance Reserve account to this mapping line or allow Synder to create a new asset account.

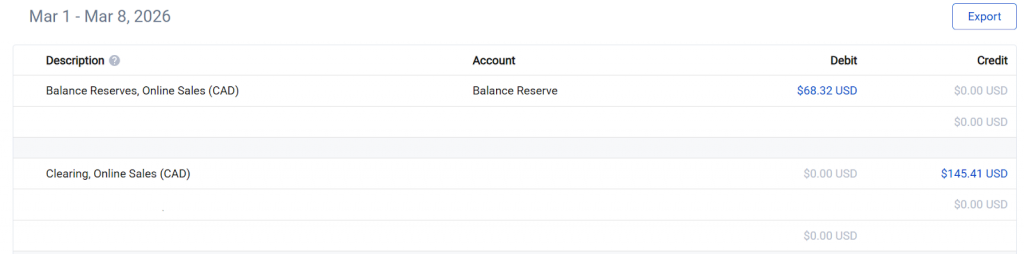

In Summary Sync mode, reserve movements are recorded inside the summary journal entry:

- Reserve hold

Debit Balance Reserve (Asset)

Credit Clearing account - Reserve release

Debit Clearing account

Credit Balance Reserve (Asset)

Important Notes

- Balance reserves are not expenses. They represent temporary holds on funds.

The recommended account type for balance reserves is Asset.

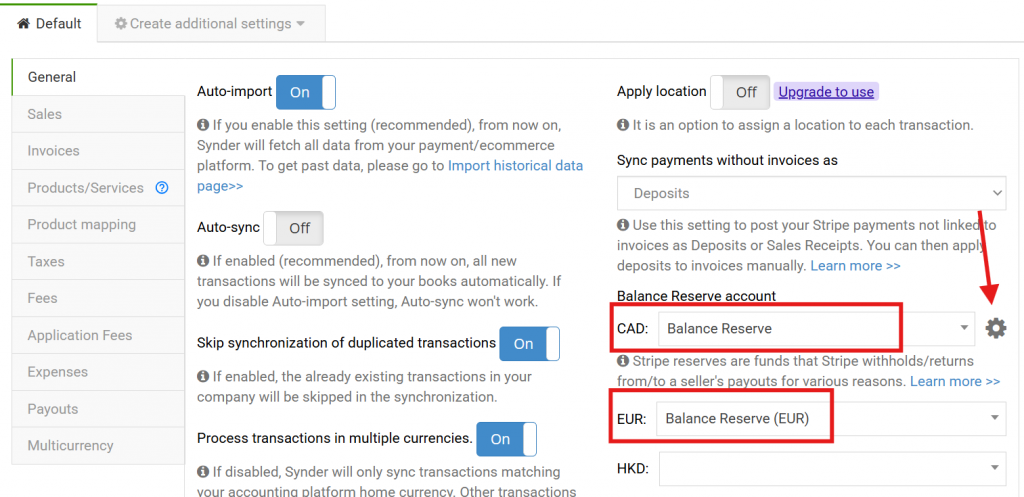

- By default, Synder creates a single Balance Reserve account and synchronizes all reserve transactions to it.

For a multicurrency setup, if clearing accounts with multiple currencies are used, synchronization may fail because the From and To accounts must use the same currency.

To ensure accurate tracking:

- Create a separate reserve account for each currency (for example, Balance Reserve CAD, Balance Reserve EUR, Balance Reserve GBP).

- Assign the appropriate account in Synder settings.

FAQ

- Why did my Stripe balance decrease but no expense appeared?

Reserve holds are not expenses.

They only move funds into a temporary reserve account. Synder records the movement from Clearing account to Balance Reserve account.

- Why do I have the Balance Reserve account created automatically in my accounting platform?

This account tracks funds temporarily held by Stripe so your accounting balances remain accurate.

You can change the account in Synder settings if needed. - Why does the transaction amount look negative or positive?

Stripe represents reserve movements using positive and negative balance transactions. Synder uses this direction to determine how the accounting entry should be created.- Negative amount – Funds moved into reserve

- Positive amount – Funds released from reserve

Reach out to Synder Team via online support chat or email with any questions you have – we are always happy to help you!